Administering a global dollar

The Fed's new standing facilities

This week the Fed released the minutes of the July 2021 FOMC meeting. Much of the discussion, and much of the commentary, has focused on the Fed's plans for tapering its asset purchases over the coming months. But the July meeting also marked the approval of two new standing facilities. This event has received less coverage than the discussion of tapering, despite its perhaps longer-reaching consequences.

Repo facilities

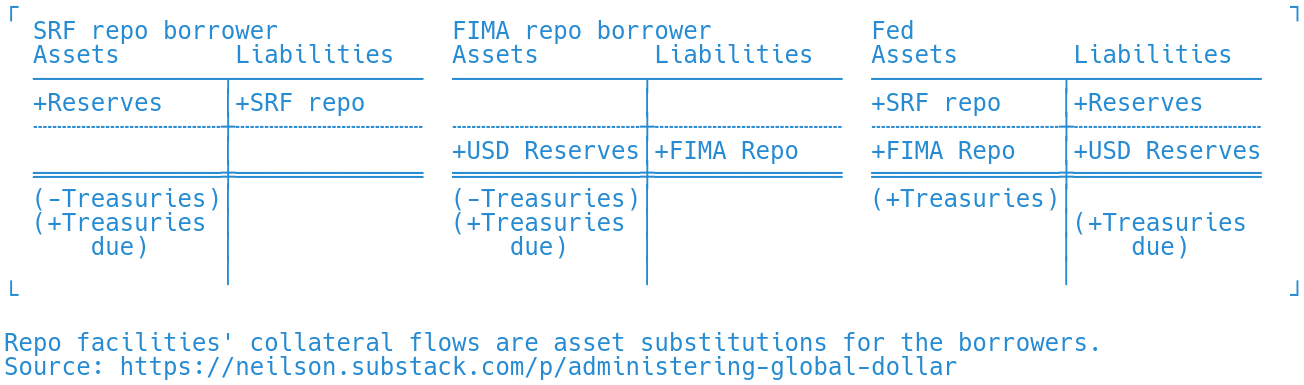

The two new facilities are both mechanisms for adding reserves to the financial system. Both operate through the repo market, extending a loan of reserves secured by acceptable collateral (Treasury debt, US agency debt, or US agency mortgage-backed securities). The two facilities face different sets of counterparties: the standing repo facility (SRF) for primary dealers and banks, the foreign and international monetary authorities (FIMA) repo facility for foreign central banks. Transactions in the two facilities have the same structure:

These representations show both the main funding flows, above the double line, and the collateral flows, below the double line and in parentheses. (NB collateral flows are not recorded as separate balance-sheet entries in the Fed's published accounts: mine are schematic balance sheets, for understanding.) For the flow of funding, both parties expand their balance sheets, swapping dollars today for dollars tomorrow. For the flow of collateral, the Fed expands its balance sheet, accepting collateral and promising to return it. The borrowers give up an asset, accepting in its place a different asset, the Fed's promise to return the collateral.

The minutes show that the FOMC is thinking of both the SRF and the FIMA repo facility as backstops. It is pricing them accordingly, currently at 25 bp, thus above other money market rates. They are meant to be uneconomical as a marginal source of funds when money markets are functioning: cheaper to borrow elsewhere. Under this design, both facilities would come into play only during a liquidity crisis.

Facilities for issuers of money

Compare the SRF and the FIMA repo facility to two existing facilities, the central bank swap lines and the Treasury General Account (TGA). The TGA is different from the others, but I think the comparison is helpful.

Start with the swap lines. These transactions are structured as FX swaps, which are loans of dollars secured by deposits of foreign currency. For a foreign central bank, they serve the same purpose as the FIMA repo facility above—they are a way to obtain dollars (the middle T account in both figures). The difference is in the collateral flows: with the FIMA repo facility, the Fed accepts US Treasury debt as security; with the FX swaps, the Fed accepts a reserve deposit of foreign currency at the borrowing central bank. This is crucial for a central bank, which can run out of Treasuries but can always issue more of its own liabilities.

This is the key difference between the swap lines and the FIMA repo facility, as Joseph Wang explains. They are directed at different sets of counterparties: the Fed is willing to accept deposits at only certain central banks, and these can access the FX swap lines. Everyone else has to hold Treasury collateral, which they can post at the FIMA repo facility.

I think it is helpful to group the FX swap lines together with the TGA, the US Treasury's deposit account at the Fed. The TGA is different, of course, because it is unsecured. But the reason that the TGA is unsecured is because Treasury liabilities are already the best collateral: there is nothing the Treasury could post, from the Fed's point of view, that would be better than its own debt securities. In this way, the TGA is like the FX swap lines: both are ways for issuers of good collateral to convert their debt into reserves at the Fed. Foreign central banks borrow against reserve deposits to obtain dollars; the US Treasury can issue debt securities directly to the Fed, in exchange for reserves.

A single global dollar system

This table puts it all together in a different way. The four facilities—SRF, FIMA repo, FX swap lines, and the TGA—are organized on two axes, one based on jurisdiction (vertically), the other based on whether the borrower can post its own liabilities as collateral (horizontally).

This structure says, I think, that the Fed sees itself as administering a single global dollar. It has separate channels for US counterparties, where it deals directly with government, banks and dealers, and international counterparties, where it deals only with central banks. Either domestically or internationally, some borrowers can post their own liabilities, while others have to buy collateral. The two channels are separate, but they are very much in parallel.

Thanks for reading

Soon Parted has been growing! The newsletter reached a milestone yesterday when my esteemed professor finally subscribed! Thank you everyone for reading, and especially for your responses, comments and questions.

Perry is in here. this is great news. Also I translated his lessons to turkish. https://www.paraanaliz.com/2021/piyasa/economics-of-money-and-banking-perry-g-mehrling-ders-2-g-11381/