Balance-sheet reasoning

Accounting for Soon Parted

I frequently make use of balance sheet representations in describing financial structures and events. These T accounts use the principles of accounting, but not the details of formal standards-based accounting, to convey financial relationships. This post tries to clarify the two principles of quadruple-entry accounting that form the basis of these balance sheets.

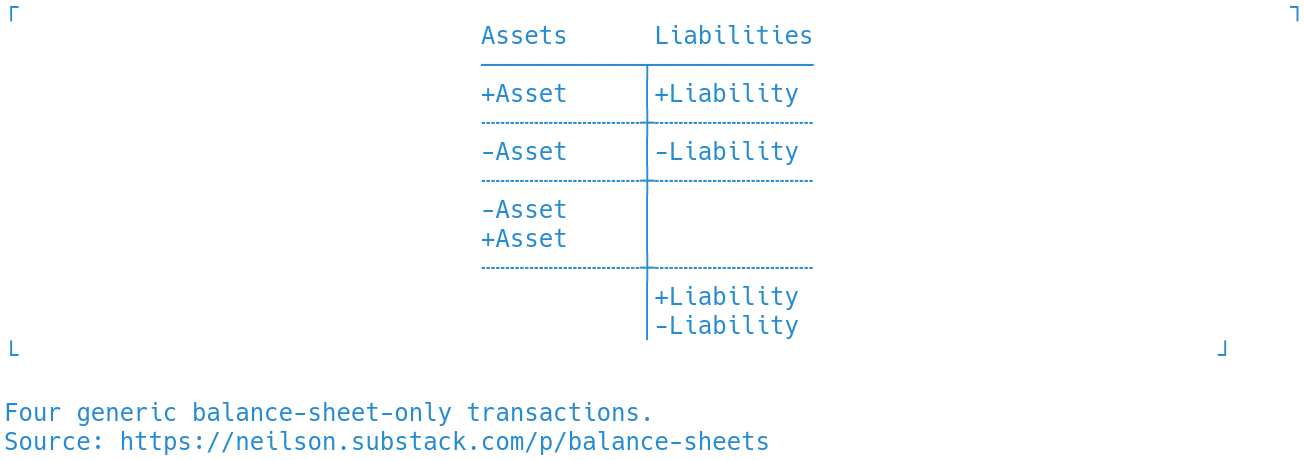

Double entry, one entity

The balance sheet of a single accounting entity—business, household, central bank—is governed by the double-entry principle familiar to anyone who has studied accounting. The values of the two sides must balance at each moment in time. This means also that any balance sheet transaction must itself balance. There is therefore only a limited set of prototypical transactions. This T account shows the four generic balance-sheet-only transactions:

Accountants will be quick to observe that there are other possibilities, those that are not confined to the balance sheet. For example, running down assets to pay an expense will have one entry on the balance sheet, and the other entry on the income statement. This is true, but my focus on monetary questions justifies narrowing the scope to transactions with balance-sheet entries on both sides.

Likewise, in practice, if one adds up actual assets and liabilities, they may turn out not to be equal. For this reason, one could introduce a balancing entry, called equity and written on the right-hand side, along with liabilities. If equity is positive, we think of it as the funds due from a corporate entity (a business) to its owners. But again, because banking transactions almost always use borrowed funds, assets and liabilities do balance, and so it is often not necessary to use an equity entry.

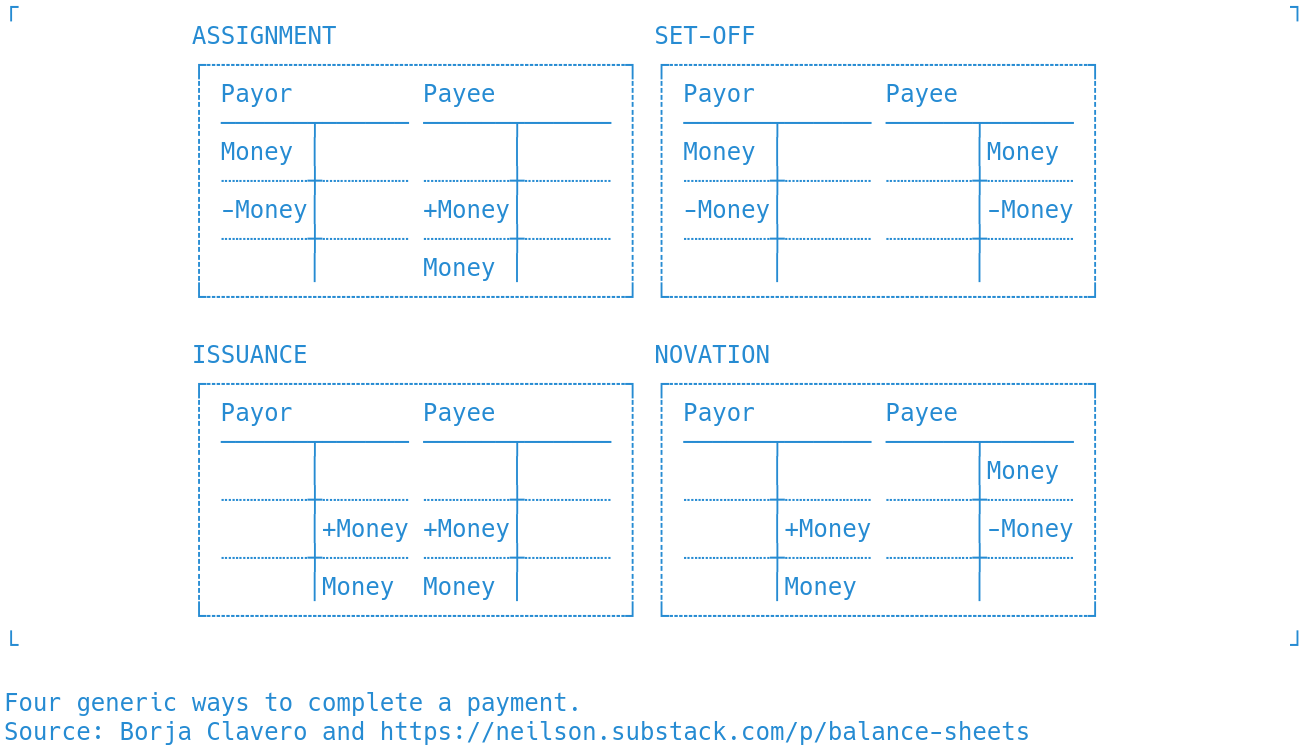

Double-entry, two entities

There is another double-entry principle as well. Because it only shows up when trying to record accounts consistently across multiple entities, it is somewhat less familiar than the first. Borja Clavero has spelled out this between-entity double-entry principle, by thinking about transactions in money-like instruments as means of payment. Because money can appear on either side of the balance sheet for either counterparty, there are four possible balance-sheet patterns for payment:

In the upper left, for example, payment is made by transfering, or assigning, an asset from one party to the other. In the lower left, the payor is an issuer of money, a central bank for example, who makes a payment by creating new liabilities.

Quadruple entry

There are thus two double-entry accounting principles: on the books of a single entity, every asset must be balanced by a liability; between entities, every asset must be someone else's liability and vice versa. If a set of accounts follows both of these principles at the same time, then it is quadruple-entry consistent. That means that it is a description of transactions that accounts for all movement of funds both within and between entities.

A generic financial transaction involves two simultaneous payments. For example, two counterparties might exchange two different forms of money. Each of the two payments will fall into one of the four categories above (assignment, set-off, issuance, novation), so there are sixteen possible ways that two payments between two entities can be completed. For example, payment in one direction could be made by assignment of asset A, while payment in the other direction could be completed by novation of liability B, which appears in the bottom-left corner of this figure:

Each box in the figure gives a minimal quadruple-entry-consistent balance-sheet transaction. They can be thought of as prototypical transaction types. I have tried to give reasonable names to each transaction type (though readers might suggest other names). The figure makes no differentiation between the two assets, and so it is symmetrical along the diagonal. If the two assets were different, for example if one were money and the other a non-money asset, the upper and lower diagonals would be distinct from each other.

Food for thought

These ideas from accounting do not make strong assumptions, nor do they offer strong predictions, about behavior. Being systematic about balance-sheet relationships probably makes arguments clearer, and it certainly aids in recognizing situations that repeat themselves in different guise.

I wonder, what would be a real world example of the two-entities double entry you called Novation? Here the Payor for granted promises to pay for the payee. That is the Payor would for granted increase his payables for the account of the Payee payables. Or is it just a building block for the quadruple entries that are real world deals?

《because banking transactions almost always use borrowed funds, assets and liabilities do balance, and so it is often not necessary to use an equity entry.》

Isn't it odd to abstract away the very reason firms exist from your analysis?

《between entities, every asset must be someone else's liability and vice versa.》

Does rehypothecation, where liabilities become assets, pose problems for this analysis?