CBDCs

Central Bank Deposit aCcounts

FOMC Chair Jerome Powell mentioned on March 18 that the Fed is, like many other central banks, exploring the issuance of a central-bank digital currency or CBDC. He cited this report on CBDCs from the BIS, which lays out central banks' thinking on the idea.

CBDCs, like paper money, are a way for the general public to hold liabilities of the central bank. Unlike paper money, they would be usable directly in an electronic payments system.

An illustration: under current arrangements, a typical payment from a deficit agent to a surplus agent involves the two agents' banks, who can complete the payment by exchanging reserves at the central bank:

The deficit agent initiates a payment to the surplus agent, and their banks settle the payment using their reserve accounts. As a result of the series of transactions, the balance sheet of the surplus agent's bank expands on both sides, while the balance sheet of the deficit agent's bank contracts; the balance sheet of the banking sector as a whole remains unchanged. The transaction affects the central bank's balance sheet only in that ownership of some of its liabilities changes hands.

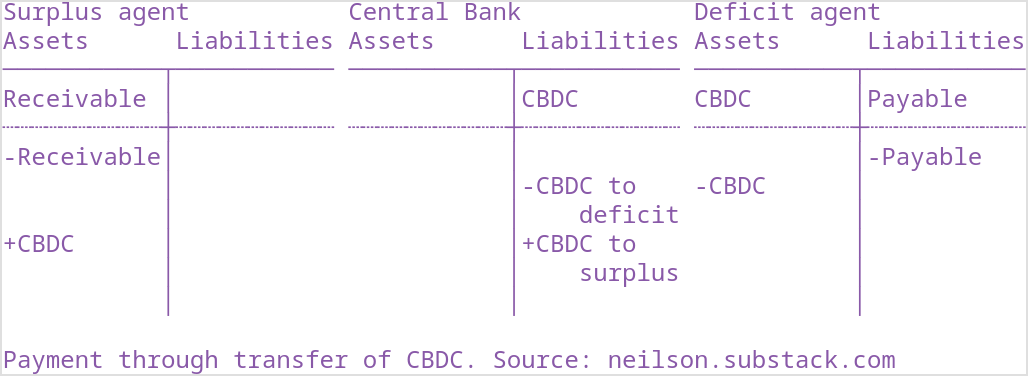

Under a CBDC arrangement, end users would have the ability to hold liabilities directly at the central bank. Now fewer balance sheets are needed to complete the same payment:

Authentication

The CBDC system is like an exchange of cash: end users can pay each other directly without going through commercial banks. It is also like the system that already exists for commercial banks: accounts at a common intermediary where payments can be completed directly.

Cash does not depend on the users' identities, but because it is physical it is inconvenient. Bitcoin is an electronic version of such token-based authentication. One path for CBDCs is to build a central-bank-operated digital token-based system, with the anonymity of cash, the immateriality of bitcoin, and the legitimacy of the central bank.

Deposit accounts use identity-based authentication. A central ledger keeps track of who has what.

Although both possibilities are entertained in the BIS study, it is a little hard to imagine central banks investing in the technology to support a token-based system, one that would enable anonymity at the core of the financial system. Objections around money laundering would be forceful.

It seems much more likely that actual CBDCs will be identity-based—in other words they will be deposit accounts. The People's Bank of China, which is not part of the BIS report, is already moving ahead with their own such system.

Implications for Financial Stability and Monetary Policy

As the example above shows, CBDCs reduce the public's reliance on banks for payment services. Disintermediating banks could be understood as either the goal of, or a financial stability risk arising from, the introduction of a CBDC. If central bank liabilities could be used for retail payments, deposits might migrate out of the private banking system.

This migration could happen over time as the system catches on, or all at once in a run from bank deposits. If the CBDC system is a reliable alternative to bank deposits, such diversity could be a source of resilience for the payments and financial systems more generally. If central banks are not able to reliably provide retail payments, or if they deprive banks of funding, it could be a source of instability.

CBDCs also open the possibility of conducting monetary policy directly with the public. By setting and adjusting an interest rate on CBDCs, the central bank could affect the public's desire to hold central bank money versus other kinds of money. One could even imagine the system playing a role in a sale of Treasuries, facilitating reflux out of the Fed's post-pandemic monetary overhang:

And so

There's a lot here: a new payments technology, bank disintermediation, monetary policy at the retail level. We'll be sorting out the details for some time to come.

A couple of things seem pretty clear already, however. First, we should separate CDBCs from crypto hype: central banks will move slowly and will try hard not to be disruptive. Second, "digital currency" is a misnomer. CBDCs are no more digital than deposits at a commercial bank have been for decades. Only in a token-based authentication system would they be much like currency. Much more likely is that they will end up being central bank deposit accounts.

I still think that's interesting, but there's nothing flashy about it.

Dear Nielson

2 additional resources

Central Bank Digital Currencies design principles and balance sheet implications.

Broadening narrow money monetary policy with a central bank digital currency

@veridelisi