Continuous payments

Fintechs are trying to build a world of continuous, interlocking payment streams

An important trend in retail credit has been the massive growth of "buy now, pay later" (BNPL) firms, especially Affirm, Afterpay, Klarna, Zip, and a service from incumbent PayPal. All provide instant credit at the point of retail sale.

In a way, these services are entirely generic retail trade credit. But it is worth observing that the BNPL firms consider themselves first and foremost to be not bankers lending money, but technology companies operating platforms. Viewing buy now, pay later as a technological intervention shows that it is connected to a broader effort, led by programmers, to create a world of continuous streams of payment. The idea shows up these days in several forms.

Retail trade credit via an API

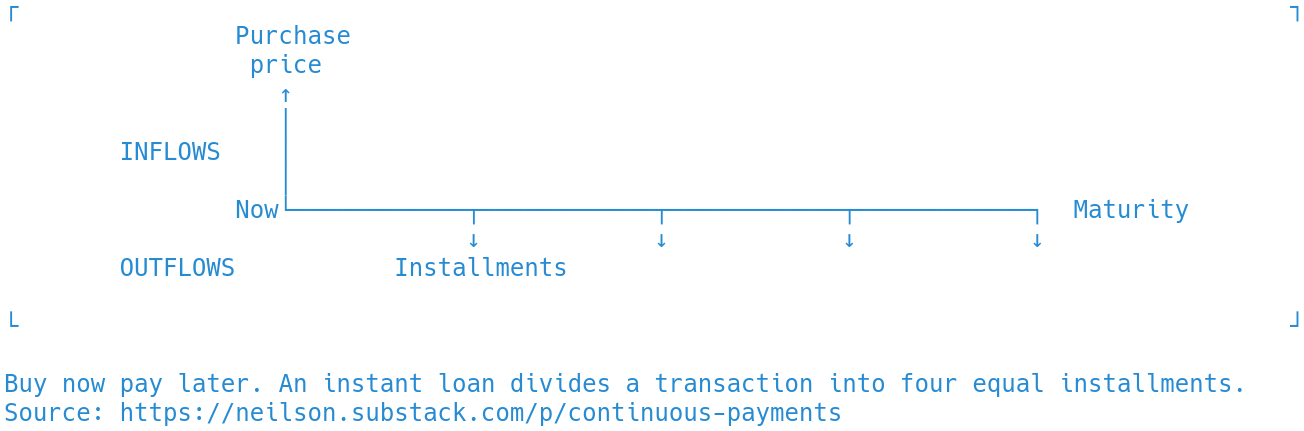

The basic BNPL transaction is, in financial terms, nothing more than a loan. The distinctive offering of today's BNPL firms is convenience: at the moment of purchase, with just a couple of clicks within the retailer's app or website, the buyer can borrow the entire purchase amount, as low as $10 or rising into the thousands of dollars. A typical transaction divides the purchase into four equal installments, and could be represented using cash flow diagrams like this:

I show the full purchase price as an initial cash inflow, though in practice this is paid directly to the retailer and never passes through the borrowers' hands. The retailer is out of the transaction after initial payment, and the loan is paid off automatically, in four payments two weeks apart in the most common arrangement. Lenders take varying approaches to interest. Typically the merchant pays a percentage to the lender, which makes the cost of borrowing invisible to the borrower. Some BNPL firms charge explicit interest and/or late fees to the borrowers.

To understand why the new BNPL firms are enjoying a boom, we have to think of them as technology companies, not just lenders. Their product offering is principally the software and platforms that make their lending smooth and almost invisible to the borrower. They are effectively selling their balance sheets as a service, connected directly and automatically to e-commerce merchants using application programming interfaces (APIs).

The lure of continuous payments

Seeing BNPL as a lending innovation driven by techology suggests a comparison to decentralized finance, where crypto technology has created a sandbox for many financial experiments. The comparison turns out to be informative.

One recent DeFi trend has been the idea of streaming payments. Zebec, for example, allows users to create automated second-by-second payments: the user establishes a total amount, start and end dates, and the protocol divides it into equal installments, one per second. Sablier, whose name is French for "hourglass," Superfluid, and MeanFi offer comparable services. These projects differ from each other in using different blockchains (Solana and Ethereum) and in how they manage the payments (with or without some kind of escrow).

With these examples in mind, it requires only modest additional imagination to see that the most generic continuous cash stream does not have an end date, but rather is a perpetuity or consol, which continues to pay—every second in this case—until the security is purchased and destroyed by its issuer. Expressed as a cash-flow diagram:

Because they are programmers, DeFi developers are excited about the composability of such streams, the possibility of chaining them together in series, so that the outputs of one stream become the inputs of the next. Every second, each such stream would take in flows of payments emerging from other streams, emitting its own payments in turn. Possibilities for synthetic financial instruments abound!

A world of continuous payment streams

I was prompted to think about this issue by my conversation with Izabella Kaminska earlier this month. Introducing her new project The Blindspot, Izabella described today's media arena as entirely structured around streams of recurring payments, to the point where it is a challenge to try to build a media business based on any other model. On quite different terrain, I had noticed that after participating in JPM's intraday repo experiment, a Goldman Sachs spokesperson was excited that they could quantify interest payments to the minute. The idea of continuous streams of payments really seems to have captured a lot of imaginations.

you omitted Lightning payments as money streaming. People pay podcasters on the minute via Apps like Breeze, Sphinx Chat or Foundain Podcast. Its called value4value (see https://podcastindex.org/podcast/value4value). Currently it uses BTCpayServer, in the future there will be static QR codes with all sorts of complex payment schemes in various currencies (see https://bootstrap.bolt12.org/examples).

I designed a payment system like this back in 2015. Instead of breaking the payment stream down into recurring discrete chunks that pay out every second (or closer), you can represent the payment in your database as a start time and a rate of flow. Then, at any given moment, you can calculate how much cash has flowed by subtracting the start time from the present time and multiplying by the flow rate.

The benefit is technological rather than financial. It allows you to represent perfectly continuous payment streams while saving storage space in your database.

I did this for the purpose of implementing a continuous basic income (UBI) payout. The basic income itself was like a perpetuity. But I also generalized the system to support payment streams with end times.

And, obviously, you have to figure out what to do when a promised continuous payment stream hits a time point at which it defaults.