I will not be the first to observe that those who know how to think about flows of funds through the monetary system are in a good position to think about flows of commodities through supply chains.

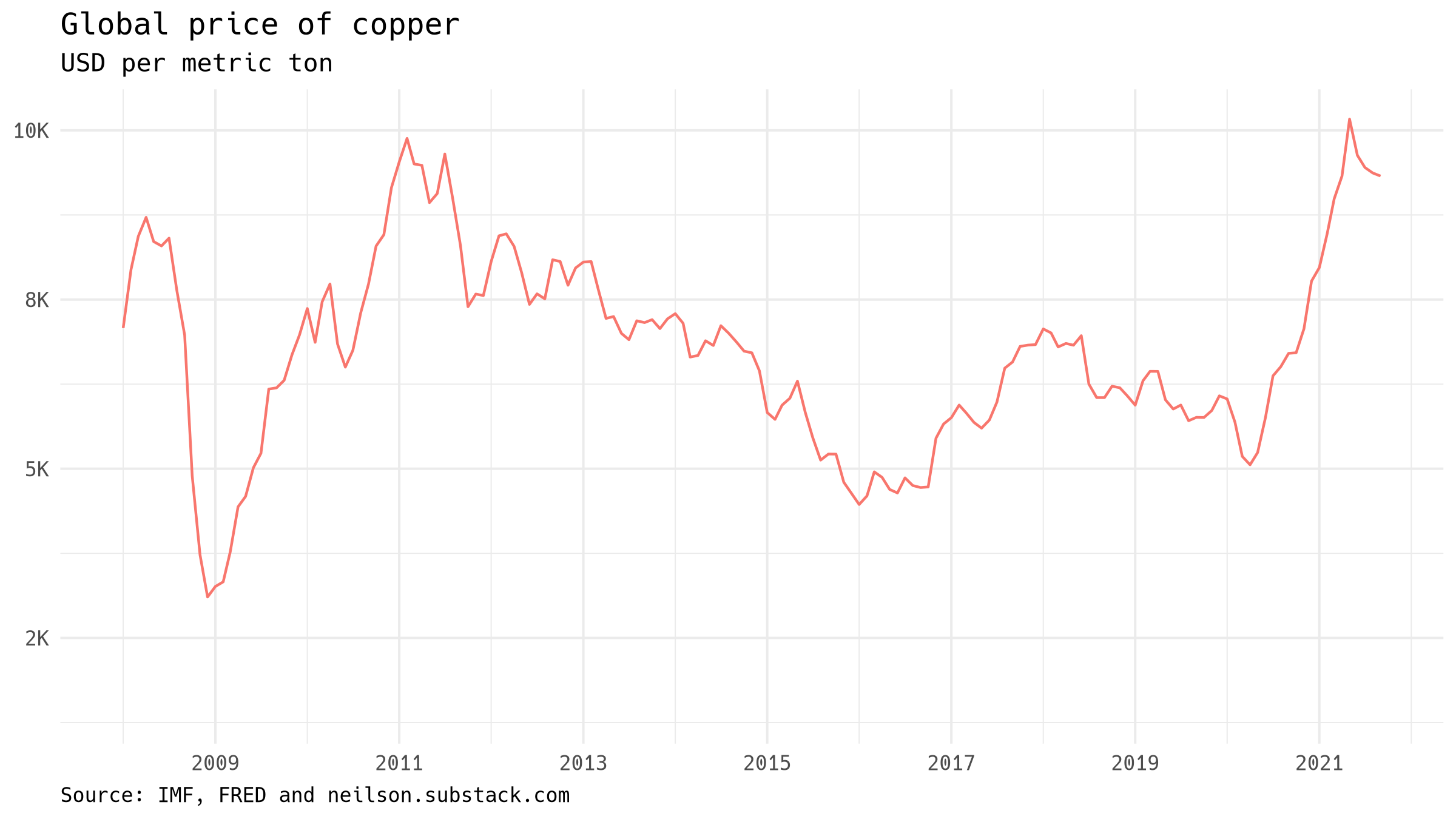

Copper, in particular, has become very expensive in recent weeks. The high price can be rationalized in a number of ways. High recent demand for the metal has much to do with its use in electronic components. Electric cars, in particular, use some 60 to 80kg of copper, perhaps five times as much as internal-combustion vehicles. Refining operations, on the supply side, have been impacted by the availability of energy. This graph, of monthly data, shows the red metal's rise in price since the beginning of the COVID-19 pandemic, though it does yet not show the recent spike even higher, above $10,000 per metric ton.

Conditions in the London Metal Exchange's copper risked becoming disorderly last week, and to restore calm, the LME engaged in what can be understood as a kind of monetary policy.

Copper warrants

The LME facilitates exchange by operating a centralized reserve of physical inventories of copper (and other metals) in its own global network of warehouses. Trading among LME members is conducted through the exchange of warrants, ownership rights to the physical inventory controlled by the exchange. Users of the metal can and do take physical delivery from these warehouses to their own facilities. Suppliers of the metal can and do make physical delivery from their own facilities to these warehouses. Centralization simplifies these logistics.

Centralization also facilitates trading by speculators that can't or don't want to take physical delivery. Because many speculative transactions offset one another, trading in warrants allows a relatively small inventory to support a relatively large volume of transactions. For example, normal settlement of a copper transaction that does not end in physical delivery looks very much like the settlement of a debt between two depositors at a bank:

Recent supply-chain stresses, however, have prompted buyers to take physical delivery, leaving the LME's inventories of copper quite low. These T accounts show commodities trading firm Trafigura, which, citing high customer demand, has markedly reduced its copper deposits with the LME:

The LME's interventions

The tight inventory makes it difficult for the LME to make a market, so last week the exchange made temporary adjustments to its clearing procedures. One of these was to allow holders of short contracts—thus sellers of copper—to delay delivery, at their own discretion. This amounts to lending metal to sellers, allowing them to defer the day on which they have to deliver. Such lending is recognizable as liquidity policy: the LME is leaning on one side of the market to ensure that trade does not break down completely. Note that the exchange is not the lender in these transactions: instead the LME compels buyers to lend.

Such lending can also happen without the exchange's insistence: another symptom of the tight inventory was a high market price for rolling over short positions using what is known as "tom-next" lending. To fix ideas, suppose that trading so far has led to one party holding a long cash position, set to be collected two days from now. Likewise another party is left with a short cash position, set to be delivered at the same date. The long, the buyer of metal, can lend tom-next to the short, by simultaneously selling for delivery tomorrow and buying in the same amount for delivery two days from now, on the cash date. Between the two settlement dates, this is in effect a loan of copper from the long to the short:

The lender receives the tom price for the sale, and pays the cash price for the purchase. Understood as a lending transaction, the difference between the two prices is effectively interest that the borrower pays to the lender, and is called "backwardation" if it is positive, i.e. if the tom price is above the cash price.

Writing for Reuters, Andy Home noted that the tom-next spread last week reached $175 per metric ton: as inventories shrank, shorts were finding it more difficult to meet their delivery commitments, and those who controlled the remaining inventory were charging a steep price for lending it overnight. The exchange responded by capping the backwardation at about $50 per metric ton, or $25 for big positions. Limiting backwardation caps the benefit to holding a dominant position.

Metals and money

The current focus on supply chains seems helpful, not only for explaining how production is continuing to respond to the stresses of the pandemic, but also for revealing something about how things had been working before. Monetary analysis can contribute to this by uncovering the clearing-and-settlement function of supply chains.

If supply chains are just payment chains in reverse, why not treat inflation as just another payments system problem and supply liquidity as needed? If prices go up, why not make sure everyone can pay them? (Isn't this how the Fed treated repo hyperinflation in September 2019, by printing money as needed?)

《Refining operations, on the supply side, have been impacted by the availability of energy.》

Is energy physicaĺly scarce, or are producers throttling supply for political or psychological reasons? Is inflation simply a power play?

When does recycling become economic? If the Fed gives consumers money to afford recycled copper, would that be better for the planet? What if engineers built with recycling in mind, designing engines such that recycling their metals is easy? Is lack of money the reason they don't do so already?