Crypto monetarism

Bitcoin is the monetization of energy consumption

This post has been updated. The second set of T accounts was expanded, and the accompanying discussion expanded.

Seen from our current vantage point of late 2021, cryptocurrencies—and Bitcoin in particular—sit at the intersection of a conversation about responding to climate change and a conversation about the future of money. It is widely understood that Bitcoin mining is an energy-intensive activity. But there is more: in fact we can understand Bitcoin as the monetization of energy consumption.

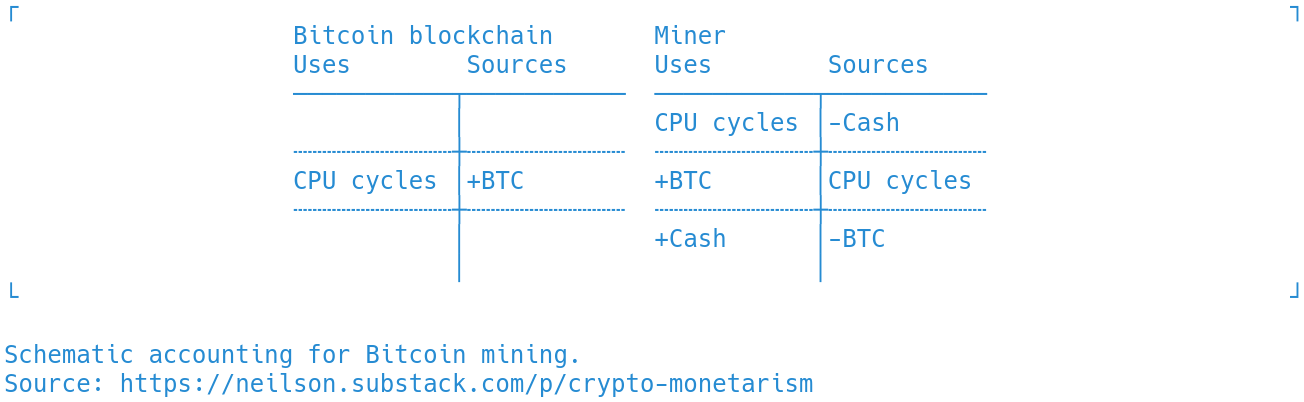

Accounting for Bitcoin mining

The Bitcoin algorithm is designed to allow a distributed network of computers to ratify all transactions, so as to reach perfect consensus as to the state of the ledger. For this to work, there must be many participants in the network, and so the algorithm creates an incentive for participation by compensating miners for their computational work.

Bitcoin mining is a financial process, so we should try to write down the accounting. The figure below, using sources and uses, shows one way to do so, schematically at least. A crypto miner (such as Bitfury, Hut 8 or Kryptovault), once it is up and running, spends cash to deploy computing power. In practice, this takes the form of facilities, maintenance and electricity for a bunch of computers. These computers provide CPU cycles (or GPU cycles, more likely) which the miner contributes to verifying the blockchain, receiving payment in return in the form of newly minted BTC, which can then be sold for cash.

This activity is profitable for the miner if the proceeds from selling the minted Bitcoin are greater than the cost of the CPU cycles that went into the mining process. Profits are maximized where input costs are lower, and when the money price of Bitcoin is higher. The game, then, is to connect cheap energy with efficient computers, and hope that the price of Bitcoin stays high.

Abstract scarcity

Underlying the design of the blockchain algorithm is the assumption that value derives from scarcity. This quaintly monetarist idea implements a misunderstanding of the gold standard in an algorithmic costume. Under the gold standard, the (incorrect) argument goes, paper money was backed by gold. Gold is scarce, and it is that scarcity that makes paper money valuable. Now, the argument (incorrectly) continues, we can do one better, because using math we can create an even more precisely defined scarcity, which can be the basis for valuable money. The Bitcoin algorithm guarantees this precise scarcity.

There are two problems. The first is that this is not a good understanding of the gold standard. In fact, under the gold standard, the issuance of paper money or deposits, notionally promises to pay gold, expanded and contracted according to the interacting interests of states, markets and business. Whatever one thinks about the system, the scarcity of gold was not the defining feature.

The second problem is to me the more interesting one. The Bitcoin algorithm implements scarcity using the difficulty of the computational work of verifying the Bitcoin blockchain itself. That algorithm is well defined, so what is scarce is really just the computing cycles needed to carry it out. For the most part, computing hardware is available, so in the end, the scarce resource is the energy needed to power it.

In other words, Bitcoin is the monetization of energy consumption.

Thought experiment: an alternative design

This perspective illuminates what, from a monetary point of view, appears as a big design flaw: Bitcoins are not proper financial claims. Unlike central bank money, government debt, commercial bank money, or even gold certificates, they are not anyone's obligation. The energy that goes into Bitcoin mining is not accumulated anywhere, and cannot be recovered—it is lost forever.

The same can be said of the energy that goes into mining gold. But Bitcoin has already given up gold’s physicality to become purely symbolic, like a financial instrument. This suggests an alternative design, which I offer as a thought experiment and nothing more. Rather than monetizing energy consumption, one could instead monetize the computing activity itself. A seller of cloud computing services, something like Amazon Web Services, might make a market in CPU cycles, buying miners' CPU cycles and selling them to those with computing needs. Miners could be compensated in tokens according to their contributions. Crucially, the tokens issued in this way would be redeemable for CPU cycles:

This is not much like Bitcoin, of course. It would leave blockchain software developers with spare labor capacity, and under such a system they would have to find something else to do. On the other hand, it does suggest how rethinking money could channel the intense computing resources currently devoted to crypto mining in a more useful direction.

Hmm.

I follow the argument that Bitcoin is the monetization of energy consumption. Whenever the price of Bitcoin is higher than the price of the total quantity of energy required to mine it, it's profitable for miners to put more energy into mining Bitcoin. So they will. This action arbitrages away the difference between the two prices until the quantity of energy put into the mining process rises (or falls) to match the price of the Bitcoin.

But the price of Bitcoin itself isn't determined by the mining process. Bitcoin is a speculative asset much like gold. People buy (and hold) it because they're hoping it will increase in value. Just like gold, the price of Bitcoin could go to zero, but it probably won't because so many people out there are committed to "buying the dip" and holding it as a long-term savings instrument.

As you point out, Bitcoin (just like gold) is not a proper financial claim. And the energy that goes into Bitcoin mining is just gone.

So far, I basically agree with everything you're saying.

But then we get into your thought experiment about monetizing computing activity and making a market in CPU cycles.

Are you just saying that:

1. In addition to (or instead of) using their own data centers, Amazon could farm out some of its computational load to the public, and pay them for it?

2. Amazon can pay for the CPU cycles by issuing its own tokens that are IOUs for CPU cycles?

3. Miners can sell those tokens to people who want to pay Amazon for cloud computing services?

If so, what's in it for Amazon? Why don't they just use dollars? Why is it useful to issue a new token when they can instead just pay the miners in dollars and continue to bill their clients in dollars?

Dear Mr. Neilson

I find it very difficulty to understand your point on the design flaw of Bitcoin compared to gold. How does the fact that coins are digital make Bitcoin a worse base layer money? How does the form (digital vs. physical) have anything to do with the monetary function?

Let me also mention that I believe you mischaracterize the function of mining. In concert with the programmatic difficulty adjustment, prove of work ensures that miners deploy costly resources (capex and opex) to attend a new block to the timechain. Since node operators determine the value of the coins released to the miner, he / she must behave according to the rules to not end in financial ruin. Energy is the resource chosen by the protocol because it can never be costless.

Bitcoin, to mention an ancillary point, is not only appreciated because of scarcity, but has many more attributes that make it a suitable base layer counterparty-free money: privacy, divisibility, ease of storage, ease of transfer, ease of verification and infinite scalability (via smart contracts like The Lightning Network). Many of those attributes are not present in gold.

The emergence of credit is a function of market demand. Credit is also possible (actually a reality, see exchanges and custody wallets) in the emerging Bitcoin monetary system. However, the public ledger plus make credit expansion more difficult to credibly establish and generally less mandatory given the ease of storage, transfer, verification and divisibility.

Thank you for your consideration.