E-krona

Sweden's CBDC pilot

A number of central banks are moving forward with implementation or pilots of central bank digital currencies. Like banknotes, CBDCs are meant to provide a way for end-users to transact using liabilities of the central bank. Like bank deposits, CBDCs are meant to be easily usable for electronic payments.

Within these bounds, there are still a range of technological, operational and financial choices on which CBDC designs can differ from one another. The Swedish Riksbank has piloted a design for its e-krona, which is the subject of this edition of Soon Parted.

E-kronor, like all CBDCs, would be issued by, and be liabilities of, the central bank itself. In the Riksbank’s project, money is issued in the form of tokens, unique data objects that could be held as assets by banks, in a database that the Riksbank’s project calls a vault, or by end-users, in a database called a wallet.

In the e-krona design, banks provide end-user-facing services, while the central bank issues and verifies tokens.

Initial issuance of e-kronor would be against banks’ reserve deposits in the Riksbank’s RIX settlement system.

One distinguishing feature of the e-krona pilot design is that it is based on single-use tokens, each representing a claim on the Riksbank for a specific amount. Each token can be used only once. Payment or transfer of e-kronor destroys the old token and creates one or more new ones. In this system, the Riksbank operates the servers that verify each token at the time it is used for payment and issue new tokens in the appropriate amount.

When a commercial bank distributes e-kronor to its customers, for example, it submits tokens from its vault to the Riksbank for verification, which destroys them, and issues new unused tokens to the end-user's wallet in the appropriate amount. Similar logic applies when the tokens are exchanged among users in payments.

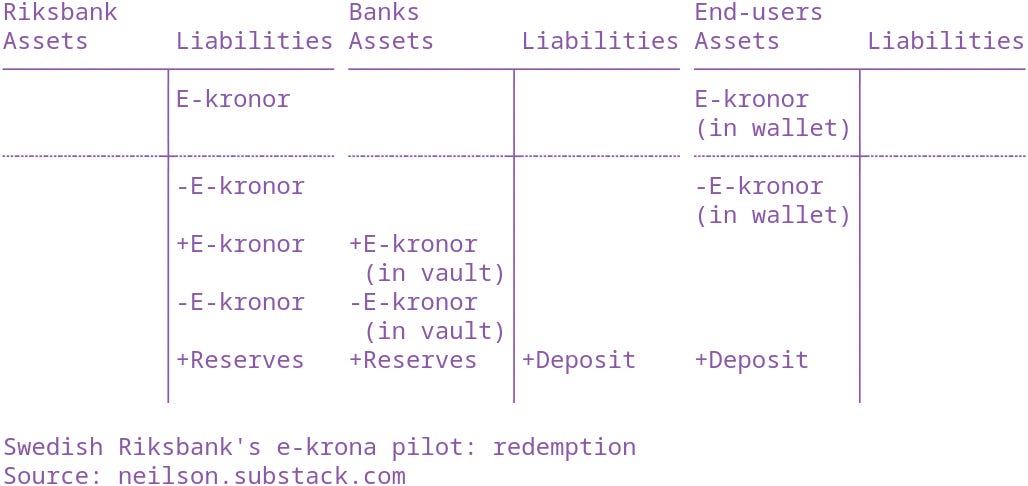

Redemption of e-kronor for deposits takes the same steps in reverse:

Note that if end-users shift from holding deposits to holding e-kronor, it reduces the deposit funding available to the banking system. This creates the potential for a generalized run on the banking system, in which a sudden shift from deposits to e-kronor would leave banks short of funding. More generally, the technological and operational choices made in CBDC design may have implications for financial stability. These concerns will shape CBDC implementation and policy, and it seems too soon to say if a single consensus design will emerge, or if there will be a variety of systems.

Are they deposit accounts?

Much of the e-krona’s logic is based around separating the central bank’s work of issuing and processing payments from commercial banks’ work of managing user accounts. In large part, this seems to be so that central banks will not face know-your-customer obligations.

Previously, I argued that CBDCs would end up offering something more like deposit accounts than anonymous tokens. The e-krona pilot bears out the spirit of that argument, but the operational details matter: e-krona users are not anonymous, but also it is not the Riksbank that is responsible for verifying identities. And while e-kronor are operationalized as “tokens,” the fact that they are single-use means that each transaction must come back to the central bank—more like a deposit account than like a physical token that can be passed around.

Concrete CBDC projects are now in place in the Bahamas, whose “sand dollar” is already in circulation, and in China, where an e-yuan pilot is moving forward quickly. The Bank of England indicated interest in its own project this week. Each pilot project approaches the financial, technological and operational details differently.

It seems safe to say that more projects are coming, that there will be more variation in the details, and that eventually there will be an interesting miscalculation on the part of some central bank.