Greensill

The Greensill affair has called attention to developments in supply-chain finance. The financing mechanisms are being compared to the securitizations that played a central role in 2008, but that's not particularly helpful. The consequences here seem likely to be limited to those with direct involvement.

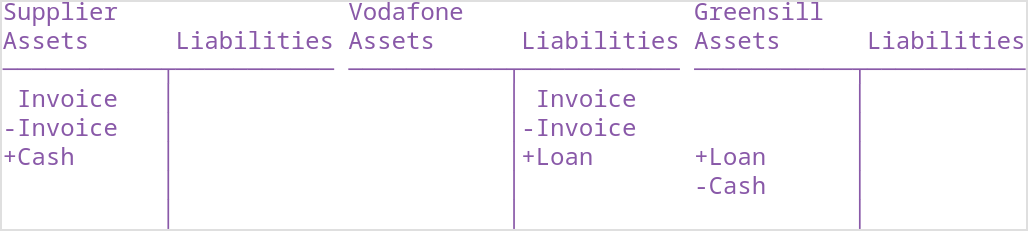

Greensill was providing an elementary banking service based on supply chains. An upstream supplier sells to its downstream customer (e.g. Vodafone), financed on invoicing terms, maybe 3 months. Greensill steps in to pay the invoice by lending to Vodafone and paying the supplier immediately, but at a discount. Here is the supply-chain finance leg in T-accounts:

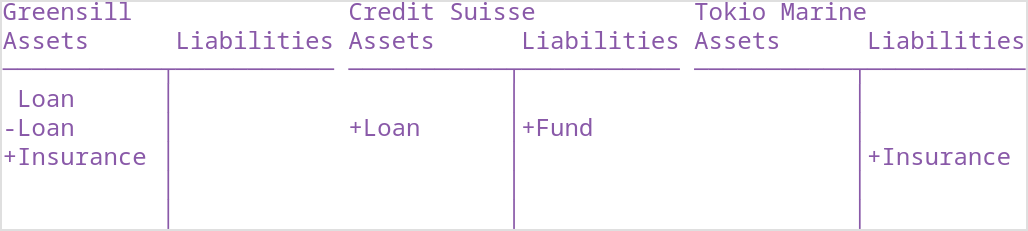

Greensill needs cash in order to engage in this business. This they obtained by selling the loans on, for example to Credit Suisse, who in turn held the loans in funds marketed to its clients. The grease that made this work for all concerned was that Greensill bought insurance on the loans, notably from Tokio Marine. Greensill's inability to renew its insurance was what triggered the breakdown. Apparently Tokio Marine had grown uneasy about the extent of its $7.7bn exposure to Greensill. Here is the funding and insurance leg (Credit Suisse's customers not shown):

This is routine financing. There's some fragility that shows up when Greensill can't replace its insurance coverage, and the whole thing falls apart. There are a couple of smellier aspects to the story. Greensill's supply-chain finance financing was deployed to make less-than-arm's-length deals. For example, Japanese conglomerate SoftBank owned stakes in both Greensill and hotel business Oyo. Oyo borrowed from Greensill for financing, Credit Suisse bought the loans and packaged them into funds, and then SoftBank bought shares in those same funds. Here it is in T accounts:

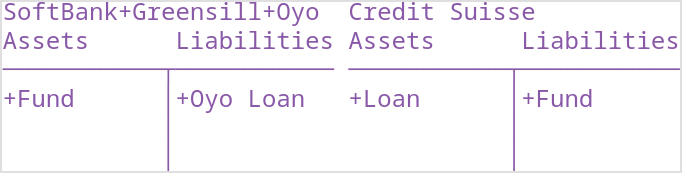

The self-dealing is more transparent if you consolidate SoftBank with its ownership stakes in Greensill and Oyo (note this is schematic accounting to show the financial relationships, not formal standards-based accounting):

In other words, SoftBank was using supply-chain finance to borrow from Credit Suisse, using the proceeds to invest in its own loans, repackaged as CS funds. Presumably fee income was substantial while it lasted. CS was obliged to clean house.

Greensill also seems to have been involved in excessively cozy financing with companies affiliated with metals conglomerate GFG Alliance.

My take

Mapped out like this, there's nothing here that we haven't seen countless times before. Finance attached to a big stream of cash flows (supply chain) supported by risk transfer (insurance) that scaled up to support fee income until it became fragile and illiquid and finally broke.

This is embarrassing and expensive for Credit Suisse and others involved. But probably not systemic—there's no sign yet of unexpected spillover into more general financing channels.