An inflection point for the Fed

The Treasury General Account drawdown

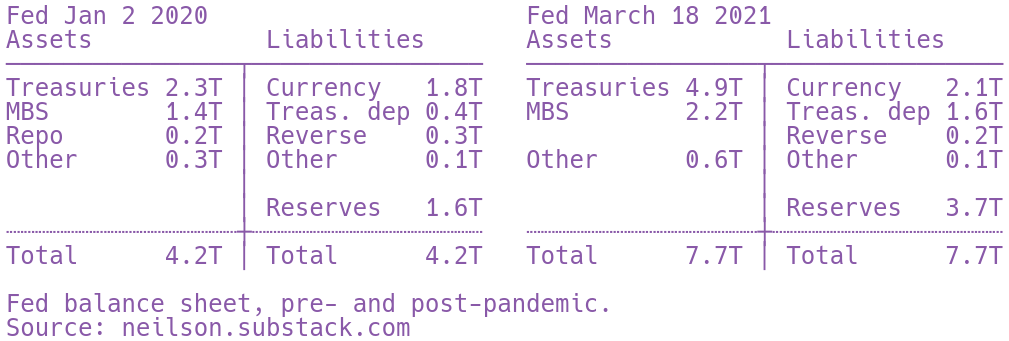

During 2020, the US Federal Reserve bought more than $3 trillion in securities. In an earlier post, I put this in the context of the transformation of the Fed's balance sheet since the 2008 crisis.

Most of the bonds that the Fed purchased were Treasuries. Some of these bonds were purchased out of the holdings of the private sector; others were newly issued. The US government's stimulus spending has lagged behind its borrowing, so the Fed's purchases led to expanded deposit liabilities in the Treasury's general account, which is the deposit account that the Treasury uses for most of its transactions.

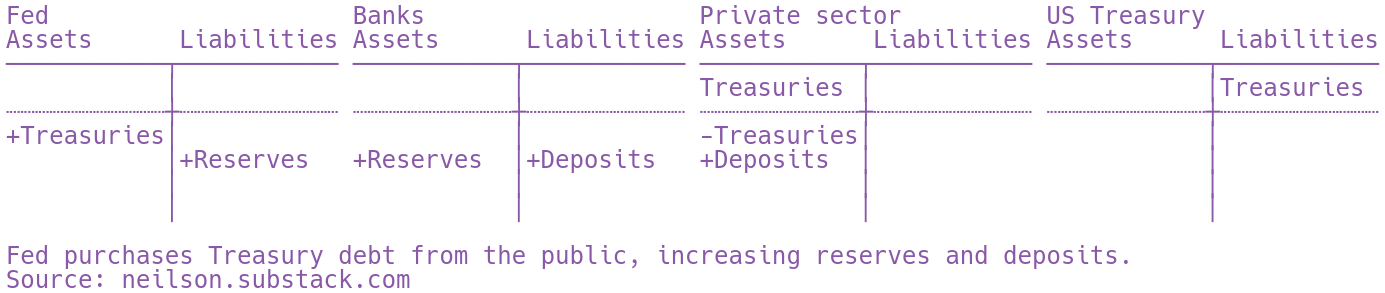

Now the Treasury is quickly running down that balance and slowing issuance of new debt. I think of the Treasury as using stimulus spending to acquire an equity stake in US productive capacity. "Equity" because in a sense it is residual—the availability of tax receipts depends on uncertain future levels of taxable incomes. These T accounts show both the initial borrowing (above the dotted line) and the subsequent spending (below).

The Treasury's drawdown began in early 2021 and now totals more than half a trillion. This graph shows the initial increase, with reserve balances and the TGA balance increasing together, and the drawdown, with reserves increasing and the TGA balance decreasing beginning in Feb 2021.

The Fed, meanwhile is continuing to purchase Treasury debt. But because new issuance is declining, the marginal source of government debt is the holdings of the private sector. Likewise, the marginal source of funds is commercial bank reserves:

Both stimulus spending and the Fed's asset purchases have the effect of increasing bank reserves and deposits. This in turn increases banks' leverage ratios (capital to assets), a constraint that is now starting to bind as pandemic exemptions expire. At the same time, bank lending has not grown, though opinions vary as to whether this is a consequence of prudence on the part of banks, as SocGen's chief economist Michala Marcussen argued, or lack of demand, as JPMorgan's CFO Jenn Piepszak suggested. Perhaps the distinction is not so great.

In any case it seems to be an inflection point: one of the big balance-sheet items from the monetary response to the pandemic has gone into reverse. There is little reason to think that bank reserves will follow soon. More likely, leverage ratios will be adjusted to accommodate the high level of reserves, and we will wait to see what happens next.