Macro accounting frameworks

For when we need to talk about macro and finance at the same time

Sometimes it is helpful to be able to look at spending and financial flows, together, at a systemic scale: a macro framework fully integrated with financial and monetary flows. Macroeconomic theory does not really provide such a thing. But even if they are imperfect, clarifying the accounting frameworks that macro models actually use is already of some use. This—somewhat infrastructural—post works through three familiar macroeconomic frameworks using explicit accounting, a first step in making them more useful for monetary considerations.

Aggregate supply–aggregate demand

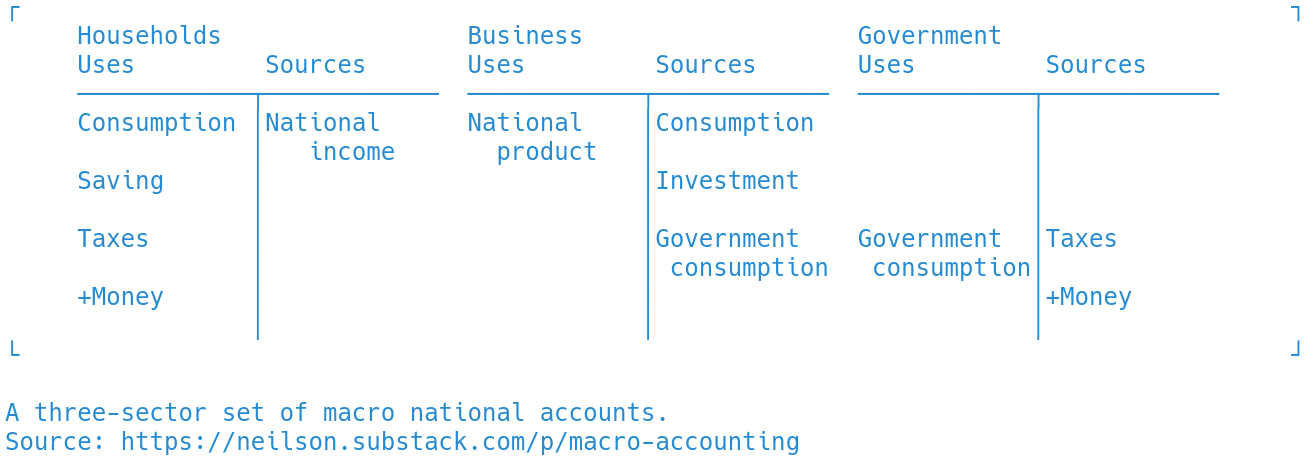

This first set of T accounts shows a macroeconomic accounting framework in which finance is almost absent. Most of the quantities are flows of spending that do not accumulate, so sources and uses accounting is the clearest way to represent them. Consumption spending, for example, is a use of funds for households that results in the destruction of the consumption goods. Each sector in this framework gets a T account, with uses of funds to the left and sources of funds to the right:

Such a macroeconomic structure imagines business selling to households and government, and selling investment goods (to which we return at the end). These funds are paid out as national product to households in the form of wages, dividends, profits, rents and interest. These same flows are called national income when thought of as a source of funds to households. National income in turn is absorbed by consumption, saving, taxes and money accumulation. Money is issued by a government sector. Together with taxes, money issuance funds government spending.

The accounting structure is most of the way to a theory. It ensures that national income equals national product, and so it then follows from the accounting structure that savings equals investment. One way to interpret this is to imagine that households engage in "real saving," i.e. by buying the physical capital and renting it to businesses. One can make assumptions about the dependencies of the different variables on interest, or add a model of price determination, as macro courses often do.

There is basically no room for a financial sector here: the only finance is a money issuance by a consolidated government sector. As such the framework can speak to monetary policy only in a limited way.

Stock–flow consistent modeling

The stock-flow consistent (SFC) modeling paradigm begins with an explicit, quadruple-entry consistent accounting structure. In the SFC literature, sources and uses are typically distinguished using positive and negative numbers, which can be translated into debts and credits (left and right sides) as I have done below. These T accounts show the accounting structure for model PC ("portfolio choice") from Godley and Lavoie's (2007) SFC textbook:

Production is similar to the first picture, though investment is left out. On the financial side, the model is a step forward, showing two types of financial claim circulating alongside one another along with corresponding interest and profit payments. It is not conceptually more difficult to add further financial detail, though my T account representation would quickly become cramped. The ambitious SFC agenda has been to build complex models that can be estimated and simulated in detail. It is not my purpose here to follow them in that goal.

Hawtrey's "great credit-machine"

A third framework comes from Ralph Hawtrey's 1919 book Currency and Credit, not standard reading in macro these days but still relevant. Hawtrey was trying to understand an integration financial and production system, based on the issuance, exchange and discounting of commercial bills. The framework is payments-based, and so it creates a central role for finance from the very beginning.

These T accounts show my interpretation of Hawtrey's macro framework. An expansion of credit, finances manufacturers' production expenses. These expenses become the income of households (e.g. wages), which they accumulate as bank deposits, the source of funds that allows the banks to lend in the first place. Manufacturers then sell their product to merchants, who also buy on credit. Merchants sell to households, who pay using deposits. The merchants can then use those deposits to pay off their debt.

The result is a system where production, exchange and finance are closely connected. Flows of credit and flows of spending go hand-in-hand at every step. Hawtrey's framework is no more complicated than the others, but focuses on private credit, private money issuance, and shows how finance is closely connected both to production and to exchange.

## Macro for monetary theory

I don't think that my interests require me to commit to a single macro theory. But it is helpful to be able to map them out in language that connects to the financial and monetary flows that are more central to my work. These sketches may prove useful in the weeks and months to come.

Hi Daniel: Engin Yilmaz forwarded this post to me; I find it very clear and coherent. (And the whole blog is very interesting.)

I wrote what ended up being a kind of lengthy reply, and I though I'd share it with you here. Thanks and cheers.

Very useful and short understanding of macro-model frameworks, how to impart them clearly and coherently.

Basically, what's your economic model's "story" of how the economy works, and how does that story look, precisely, in sources and uses T accounts? Is it accounting-coherent?

How does your story divide the economy into "sectors" (or often, "functional categories" of actors/institutions, which are often orthogonal to any national-accounts sectors). And what sectors are absent?

What objects (assets) are included (and not) within the T-account cells? Do they model transfers of M2, bonds, real (long-lived) goods, etc.?

What are the relationships between the sectors, and the measures therein, as played out in the T accounts? When actors in sector X do Y, what changes are caused, in what other sectors?

The T accounts give precise form to the narrative description of the story, and let others see in condensed form what's included, what's missing, and how the included items relate.

Focusing a bit on those "functional categories" used in many models: As an inveterate "Show-Me-The-Numbers" guy from Missouri, I mostly find these "functional" categories less than useful, because I can't go look at the time-series for them in national accounts.

Researchers/model-builders are forced to effectively build their own national-accounts "sectors," and assemble time series for them from disparate sources. These series:

1. Are often/mostly not published with the model, at least in tractable form.

2. Are often missing precise, accounting-coherent descriptions of their derivations and mutual identities.

3. Are generally somewhat idiosyncratic (and not-infrequently, erroneous). It takes some serious work to unpack that down to the level of time series.

More generally: they don't provide a good basis for the larger macro-modeling conversation, based on published, carefully defined and documented series that in toto are accounting-identity coherent. With very few exceptions, those sets of mutually-coherent time series are and almost must be issued by national accountants.

PSZ tables are one good counter-example to these objections. There are certainly others. But understanding their relationships to national accounts tables requires some seriously lengthy and rather excruciating yeoman's work. I'm here to tell ya. ;-)

So I would suggest that modelers should think long and hard before building models, T accounts, and their associated stories that are not tightly linked to generally-available and broadly "legible" national-accounts sectoral series.

This is basically suggesting a fundamentally empirical limit on modelers' imaginations. In general, try to build models in which the time series do not have to be heavily massaged, and a whole novel "sector" assembled — with all the opaqueness and at least potential error that inevitably result.

FWIW...