Digital currency across borders

The BIS's mCBDC Bridge

The Bank for International Settlements, the central bankers' central bank, has been busy thinking about cross-border digital payments. This week the BIS announced, with the central banks of Australia, Malaysia, Singapore and South Africa, a new venture to build a multi-currency distributed ledger.

This new project, dubbed Dunbar, follows an earlier BIS proof of concept, the mCBDC Bridge, with the central banks of Thailand, Hong Kong, China and UAE, which is the subject of this post. Project Dunbar has its own name and a non-overlapping list of participants, from which I surmise that it is a deep reboot of the earlier cross-border CBDC project.

But the two projects face the same problem (use central bank digital currency for cross-border payments) and offer the same solution (create a multicurrency ledger). So it also seems safe to surmise that the BIS prefers this path to other less-ambitious options. Drawing mostly on a 2020 report put out by the Bank of Thailand and the Hong Kong Monetary Authority, this post looks at how the financial design of the mCBDC Bridge project addresses the key issues.

A shared ledger for cross-border payments

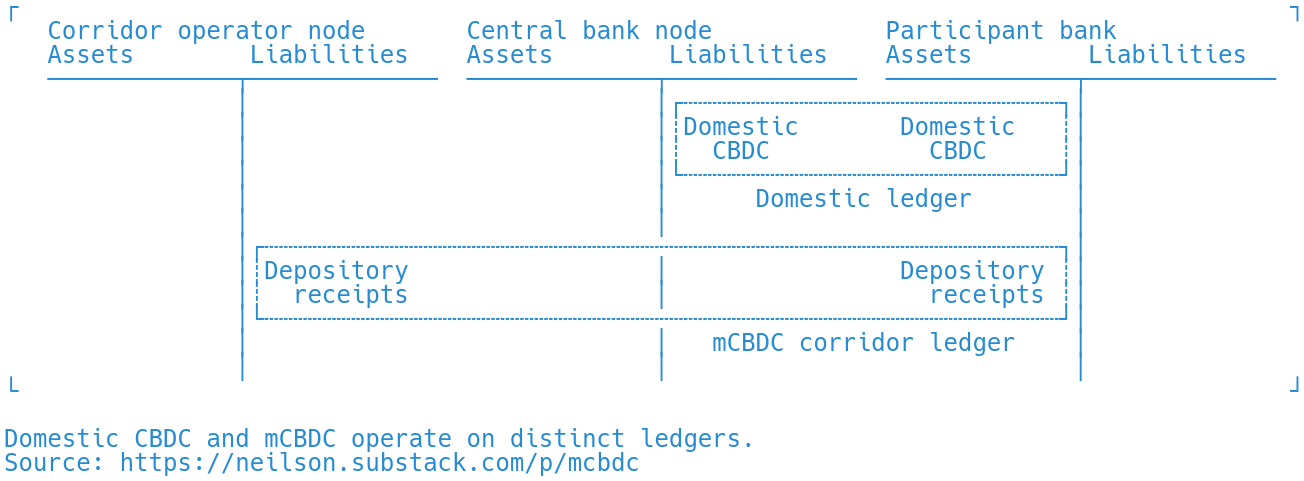

The mCBDC Bridge platform is meant to facilitate payments across multiple domestic digital currency systems. It does so by creating a new ledger, the mCBDC corridor, using Corda decentralized database technology. Within the mCBDC corridor, digital assets denominated in different currencies can circulate alongside one another.

In this system, central banks issue domestic CBDCs, which circulate on separate domestic decentralized ledgers. A so-called operator node, jointly managed by the central banks, issues depository receipts, digital assets that circulate on the mCBDC corridor ledger. Central banks facilitate entry into and exit from the corridor by offering to exchange between the two types of circulating liability. These T accounts show the operator node and one domestic branch of the mCBDC system:

The rectangular boxes show that domestic CBDC and corridor CBDC ("depository receipts") exist on distinct decentralized ledgers. Though they are denominated in the same national currency, domestic CBDC are issued by each central bank as part of its domestic payment system, while mCBDC depository receipts are issued by the single operator node and are part of the mCBDC payment system. Domestic and international CBDC are claims on two different entities that exist on two different ledgers.

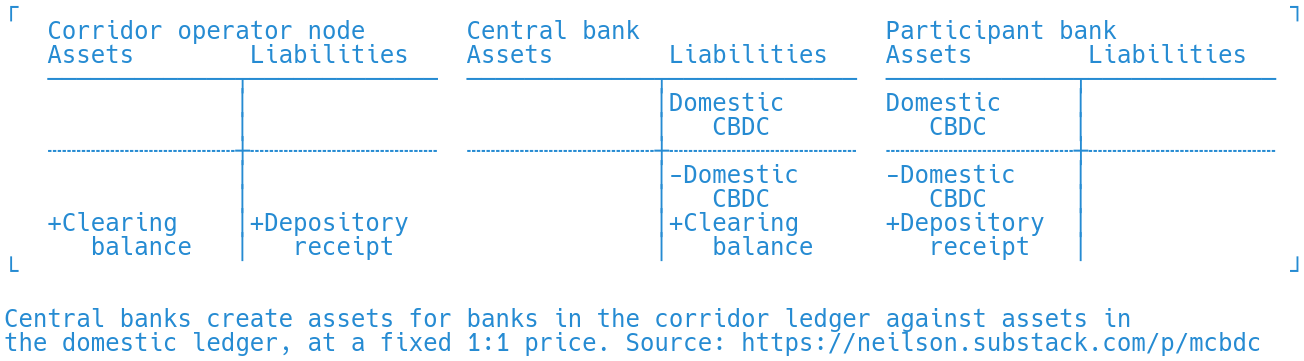

The prototype system provides a mechanism to allow the exchange of domestic and international CBDC. Each national central bank stands ready to create and destroy domestic CBDC against destruction and creation (respectively) of mCBDC depository receipts. For example, if a participating bank wants to buy money on the corridor in order to complete a cross-border payment, it can do so by destroying domestic central bank money:

The national central bank destroys domestic money and instructs the operator node to create international money on behalf of the participant bank. The BoT–HKMA working paper does not describe the financial details of this part of the process, so I have speculated a bit and added a clearing balance entry, the operator node's deposit at the central bank. Something along those lines must be happening, otherwise the accounting is not complete.

So far I have shown only a generic domestic branch of the mCBDC Bridge system, but the whole point is that the operator node issues depository receipts denominated in multiple currencies, which circulate together on the mCBDC ledger. This set of T accounts shows two branches at the same time. There are two central banks, A and B, each issuing a national currency. I show a representative commercial bank in each national system, which also participate in the mCBDC corridor.

Each central bank provides par (one-to-one) exchange between its own domestic ledger and the shared corridor ledger. All of the assets that circulate on the corridor ledger are liabilities of the operator node, which in turn holds (non-circulating) clearing deposits at each central bank. Again, these clearing balances are my hypothesis: what we know is that, in the BoT–HKMA proof of concept, the corridor is jointly managed by the two central banks, and that the operator node issues monetary claims in the corridor.

Finally, in addition to par clearing, the mCBDC Bridge design also provides mechanisms for foreign exchange liquidity to be provided within the corridor ledger. Private market-makers can post rates of exchange between depository receipts denominated in the various currencies, and foreign exchange transactions can be completed within the corridor ledger. Presumably the central banks themselves could act as FX dealers if they wanted to affect FX rates.

Observations

What to make of this?

The corridor design is posed as a way to reduce the costs of cross-border transactions. What it offers, so far, is a mechanism for bilateral exchange between peripheral currencies. The current system, by contrast, uses the US dollar as an intermediate currency, because of the vast liquidity that such a structure provides. The mCBDC Bridge does not, by itself, create more liquidity or change anything about the global monetary system.

More generally, one gets the impression that the central banker types and the blockchain types in these projects are not communicating with one another very well. The tech teams have solutions in search of problems (distributed ledger technologies), and the central bankers have problems for which DLT is not a great solution (volatile exchange rates and capital flows, high prices for access to global payment systems).

Soon enough, the Fed will weigh in, after which we will know much more about where the system is headed.

Hello, it would be great if you could comment on the recent project Jura https://www.bis.org/about/bisih/topics/cbdc/jura.htm It will be interesting to know what is the essential difference between this new modus operandi and what woud happen if the same transaction took place on the actual settelement/payment facilities.

Neilson, is like Target 2 ?