The post-pandemic Fed

Early hints

Note: I'll be away from my desk next week, so Soon Parted will take its first vacation. I'll be back June 1.

The current conversation on monetary policy has focused on the connection between the Fed's asset purchases, continuing for now at a pace of USD 120 billion per month, and prices, understood variously as the prices of equity shares, commodities, producer inputs, or consumer goods. I think there are two important limitations to this point of view. First, although the Fed has a mandate on inflation, the channel by which the central bank can affect the price level (much less employment) remains murky. Second, the Fed transacts with the money markets daily, too fast for inflation to be the main guide.

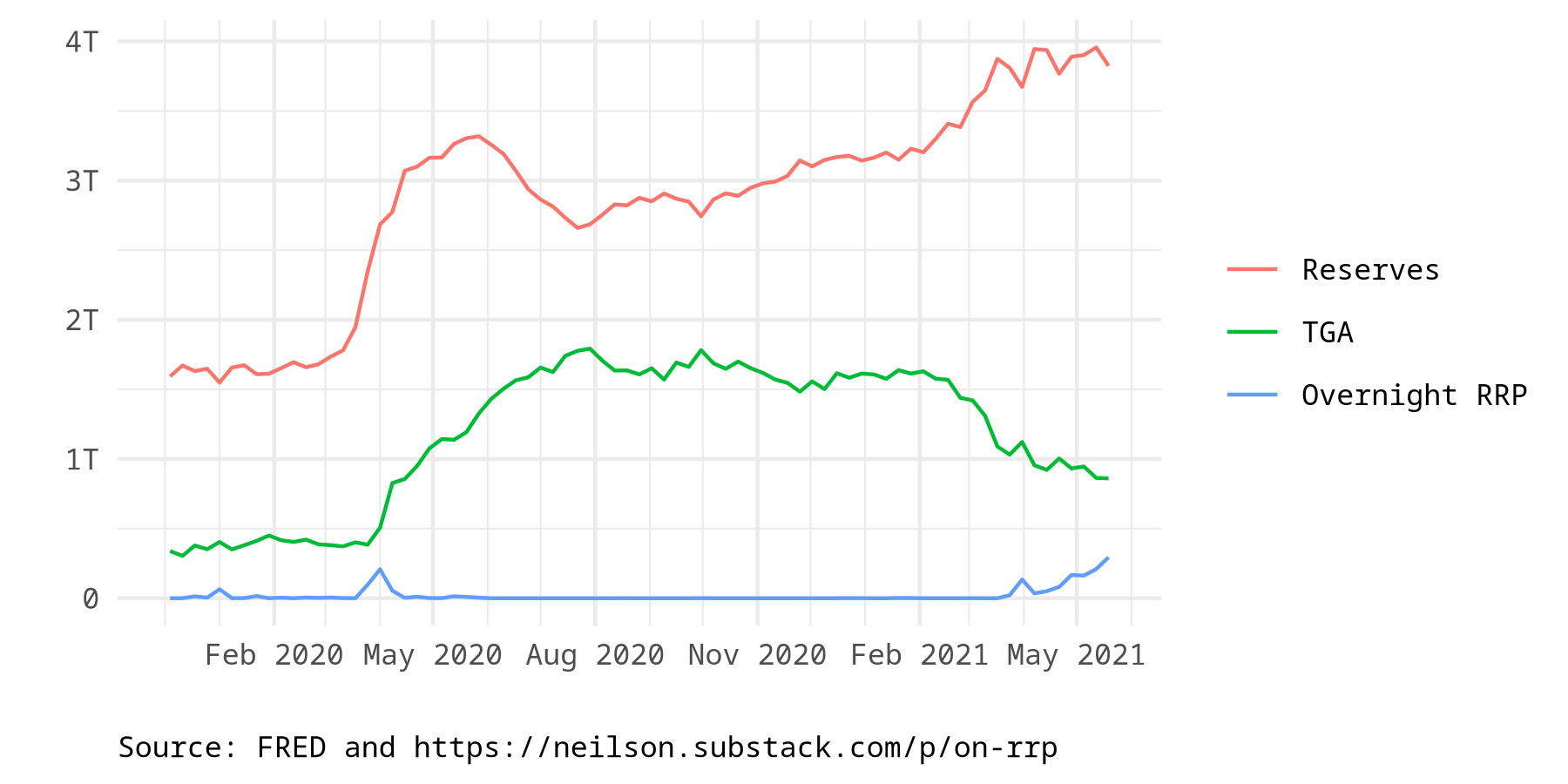

If we look not at inflation but rather at how monetary policy is implemented, a different understanding emerges. Almost independently of the conversation about inflation, big items on the Fed's balance sheet are already moving. Recently I wrote about the Treasury's drawdown of its General Account at the Fed. As the Treasury spends down this account, reserves are mechanically created for banks. This increases banks' supplementary leverage ratios (SLR), which are now close to regulatory limits.

The Fed is buying assets, not selling, these days, so reducing reserves is off the table. Instead the Fed is channeling funds into its overnight reverse repo (ON RRP) facility. This graph shows reserves (red), the drawdown in the TGA (green), and the increased use of ON RRP (blue).

What's happening? As the TGA balance falls, the Treasury is spending and those funds are flowing into banks as reserves. But banks can't hold any more reserves, so they are directing the funds into their asset-management divisions. There they end up as shares of money market mutual funds (money funds or MMMFs). The Fed's ON RRP facility provides MMMFs an asset that they can hold against these funds. (I think of the Treasury as acquiring an equity claim on the private sector, payable out of future taxes but not unconditionally so.) In T accounts:

The Fed chose this path earlier in the year: rather than easing the SLR limit so that banks could hold more reserves, it expanded per-counterparty access to the ON RRP facility, from USD 30 billion to USD 80 billion, explicitly to support accommodation of the TGA account drawdown. Zoltán Pozsár correctly called this.

How does the Fed drain reserves using the ON RRP facility? This set of T accounts tries to show the transaction in some detail. Think of the money fund as starting with deposits at a bank, though in fact the two might be part of the same holding company. In a reverse repo transaction, the MMMF lends money overnight to the Fed, who places a Treasury security with the MMMF as collateral. The loan is structured as a sale with an agreement to repurchase the following day. Between the sale and the repurchase, reserves are replaced on the Fed's balance sheet with ON RRP:

Possible Interpretations

These T accounts show both the money leg and the collateral leg, though the official H.4.1 release shows only the money leg. But we learn something by watching the movement of collateral.

The TGA ballooned by USD 1.5 trillion early in the pandemic because the Fed bought newly issued Treasury debt. The Fed was able to do so, because it could create the funds on its own balance sheet, and it chose to do so, observing the necessity for paying for the public health response. Now the bonds exist, and as the messy details of how the funds will be spent are negotiated in the legislature, the messy details of who will hold the debt are being negotiated in the financial system.

I offer three interpretations, not mutually exclusive.

First, the minutes of the April FOMC meeting put the ON RRP facility into the context of an eventual exit from crisis policymaking. At the meeting, there was substantial discussion of the creation of a standing repo facility, comparable to the ON RRP facility, but on the other side of the balance sheet: a way to add reserves rather than drain them. This suggests that the Fed would like, once it starts tightening, to have a repo corridor, with the ON RRP facility absorbing reserves and a new RP facility adding them. Overnight reverse repos, one side of the corridor, already exist, and the facility will give the Fed some operational data going into establishing a future two-sided framework.

Second, with the ON RRP facility, the Fed is, in a limited way, getting the private sector to hold some of the newly enlarged stock of Treasuries. At this point it may be largely symbolic: the transactions are only overnight, they are still small relative to the whole balance sheet, and outright asset purchases are continuing anyway. We are not talking about contraction yet. Still, even if just for a day, and even if it's not reported this way, the Fed is in some sense doing this:

A third and final interpretation is that, with the ON RRP facility, the Fed is gently reimposing discipline. At the beginning of the pandemic, the Fed intervened swiftly, increasing elasticity throughout the financial system. The daily discipline of having to return collateral to the Fed might serve as a subtle reminder to everyone else that they still have to pay their debts.

Thanks

Thanks to Zeynep Uslu, who translated my piece on Tether into Turkish. Teşekkür ederim!