Taper notwithstanding

The Fed raised limits on the reverse repo facility

Last week's meeting of the Federal Open Market Committee has been understood mostly as marking a decisive turn toward a reduction in the Fed's asset purchases. But another policy change that occurred at the meeting has gone less remarked: the per-counterparty limit on the overnight reverse repo facility was raised from $80 billion to $160 billion. This information was conveyed not in the main statement but in the implementation note that accompanied it.

We will learn more about the discussion that led to this shift when the minutes of the September meeting are released next month, but it seems likely that the Fed raised the per-counterparty limit because it expects some counterparties to exceed the old limit. Though the policy is now clearly leaning toward tightening, asset purchases are still continuing for now, and the increase on the ON RRP limits means that the Fed is still having to work to make room on its balance sheet for those purchases.

What the overnight reverse repo facility is doing

The overnight reverse repo facility, recall, is a standing deposit facility at the Federal Reserve, open to money market funds. Money funds make deposits by lending overnight to the Fed in the tri-party repo market. The central bank currently pays interest of 5 bp on the deposits, and also posts collateral, typically Treasury securities, with the depositing fund.

The ON RRP facility exists to allow the Fed to pursue its policy of asset purchases even though banks can't hold much more in their reserve accounts. Rather than loosen the rules for banks, the Fed has engineered a big shift in money fund asset portfolios.

This graph shows money market fund assets on a monthly basis. At the beginning of the pandemic, MMFs purchased some $1.5 trillion in Treasury debt, expanding their balance sheet in aggregate. Since about March 2021, MMFs' usage of the ON RRP facility has grown significantly, and since about May, that usage has more or less exactly been offset by a reduction in holdings of Treasury securities, leaving money funds' balance sheets unchanged. The Fed's asset purchases, at this point in the pandemic, amount to this:

Draining reserves

As of last week's meeting, the Fed has doubled the per-counterparty cap on the ON RRP facility, a clear indication that central bankers expect ON RRP usage to continue to expand. Commentary on the FOMC meeting has focused on the Fed's beginning to taper its asset purchases, a turning point that may now arrive as soon as the November 2–3 meeting. But even if tapering proceeds smoothly over the following twelve months, there is nearly a trillion dollars' worth of asset purchases still to come ($120bn in October and another $780bn if tapering takes 12 months). If money funds continue to be the marginal sellers of securities and the marginal buyers of Fed liabilities, the ON RRP facility will have to continue to expand.

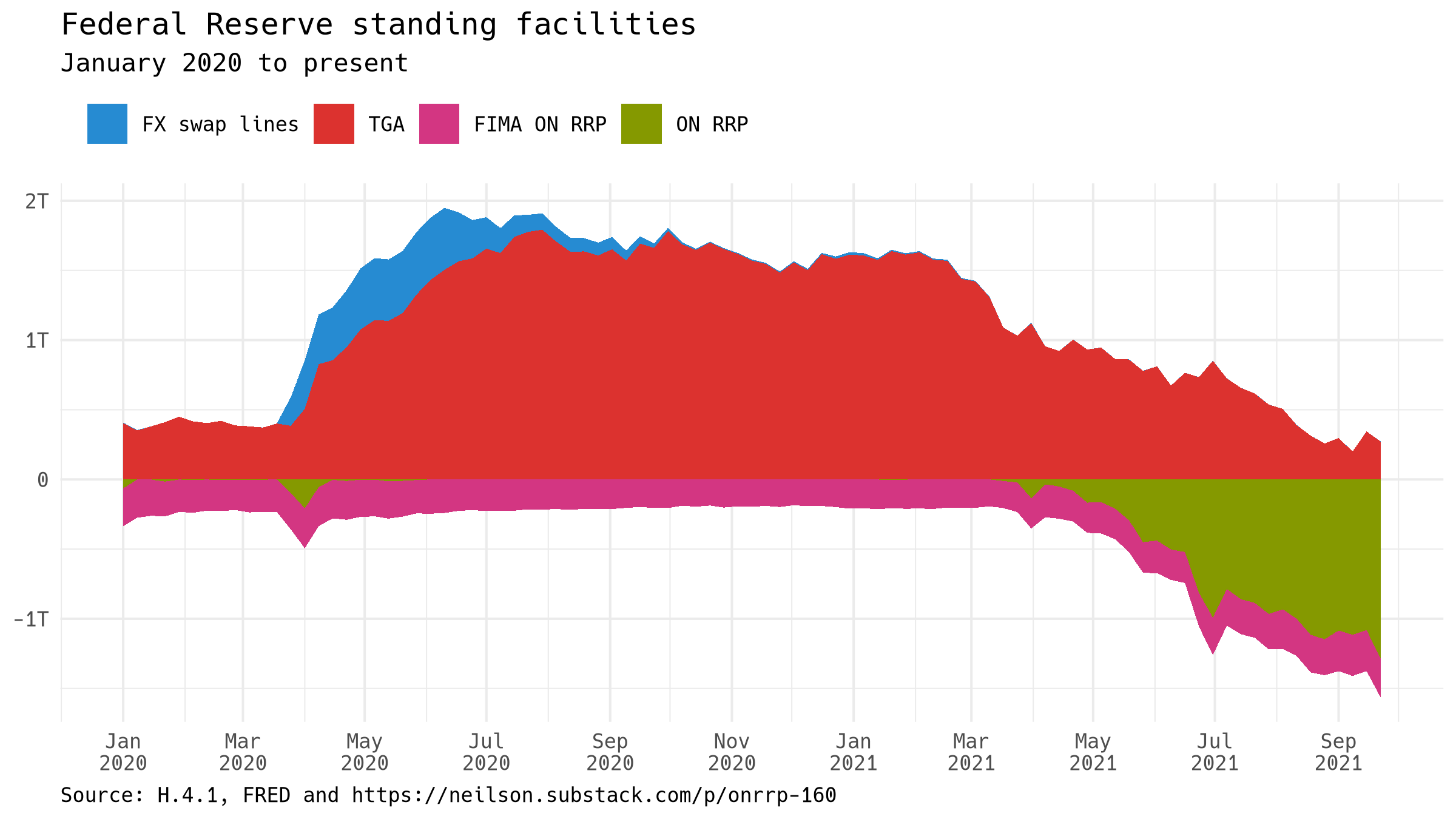

Over the course of the pandemic, the Fed has been adding reserves, very quickly at the beginning and continuing steadily since then. At the beginning, borrowing reserves by the Treasury and by other central banks indicated a general shortage of reserves. More recently, use of the ON RRP facility indicates a general excess of reserves. This graph tries to capture this dynamic.

Note, the graph does not show the overall level of reserves. Instead it shows the four standing facilities, mechanisms by which the Fed's counterparties can add or drain reserves, that have seen use during this time. Facilities for adding reserves are shown as positive numbers in the graph. The expansion of the Treasury General Account, along with the use of the FX swap lines, were mechanisms for adding some $2 trillion in reserves. Facilities for draining reserves are shown as negative numbers in the graph. The two RRP facilities are together absorbing about $1.5 trillion at present. The extent to which this graph is pushed into negative territory measures, in a way, how hard the Fed has to work to make space on the balance sheet for more asset purchases.

Taper isn't everything

Certainly the message from the Fed is that tapering is coming. But even if the pace of asset purchases slows, the central bank's balance sheet will be growing for some time to come. The Fed is still pushing hard on the monetary system, and the new per-counterparty limits on the overnight reverse repo facility show where and how it is pushing.