Pricing the global dollar

The Fed sets a global outside spread

A couple of weeks ago, I looked at the Fed's creation of two new standing facilities as part of its administration of the global dollar. The new lending mechanisms, the standing repo and FIMA repo facilities, along with the existing facilities, the Treasury General Account and the FX swap lines, are all mechanisms for adding dollar reserves to the payment system. To complete the picture, we should add the Fed's two other standing facilities, which drain dollar reserves.

Repo facilities for draining reserves

The overnight reverse repo and the FIMA overnight reverse repo facilities have already been in heavy use, a consequence of the central bank's balance sheet expansion (i.e., quantitative easing) stance over the course of the COVID-19 pandemic. The Fed acts as a borrower in both cases; the transaction is conducted in the repo market in both cases. These T accounts show, above the double line, the two facilities as they are recorded on the Fed's balance sheet. Because they are repo transactions, there is also collateral flow. The Fed does not record these on its balance sheet, but I have done so, below the double line:

Own-issuance facilities

The two own-issuance facilities (as I have labeled them), the TGA and the FX swap lines, also absorb reserves, though in a different way. Both the Treasury General Account and the FX swap lines provide USD dollar reserves using the depositors' own liabilities as collateral. For the TGA, this collateral takes the form of Treasury securities; for the swap lines, reserve deposits at other central banks. Because the collateral is a liability to the depositor, there is no need for a special mechanism to absorb reserves: the depositor can always absorb reserves simply by cancelling them against its collateral.

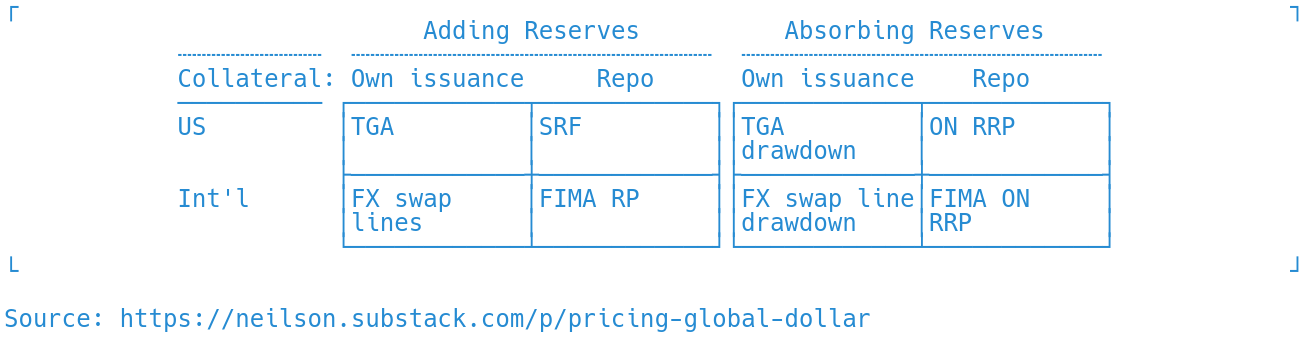

Both sides of the market

This analysis arranges the standing facilities into a nicely symmetrical picture:

There are three dimensions: adding vs. absorbing reserves; domestic vs. international, and own-issuance vs. repo. All eight possibilities exist, though as I have shown, the mechanics are not perfectly symmetrical.

Pricing the global dollar

How are all of these mechanisms meant to work together? The way that the facilities are priced suggests an initial interpretation, though experience over time will be more informative. Closest to zero are the reserve-absorbing reverse repo facilities, priced since June at 5 basis points. Money markets have been stuck to this floor since then. The reserve-adding mechanisms are intended for a post-QE future, in which reserves sometimes need to be borrowed. They are priced at 25 basis points, above current money-market rates.

The intention is for normal money-market prices to be set by private dealers, with recourse to the standing facilities being the exception not the norm. The Fed will make an outside spread, that is, while private dealers make a narrower inside spread. The standing facilities will ensure that when private market-making breaks down, a lot of liquidity is available just at the edges of the corridor.

In this Treynor diagram, I think of private money market dealers establishing a price along the sloped, dashed inside spread lines. When their position reaches its max long limit, i.e. when money markets have lent as much as they can, they will have to borrow reserves from the Fed at the SRF rate. Similarly, when money markets have borrowed as much as they are willing, they can offload any excess by depositing at the Fed at the ON RRP rate.

I have shown the FX swap lines as being priced even further out. There is an important ongoing conversation on the international dealer of last resort function. Building that connection will have to be work for the future.

Hi Daniel, I would love to see a post with some balance sheet diagrams explaining how "minting the $1T coin" would work. At this point it seems very unlikely, but I'm interested in the theory behind it. In particular, I've heard it said that it's equivalent to issuing debt, but I don't really understand that. Cheers.

Zoltan was saying this exact thing on the Odd Lots podcast a couple days ago. reverse repo facility makes sure interest rates dont go too low, Swap Lines make sure it doesn't go too high. We finally have an officially standing dealer of last resort.