Mechanics of quantitative tightening

Animating Zoltan

The Fed now seems likely to raise overnight interest rates from zero at its March meeting. With that move apparently baked into the cake, everyone is talking about "QT," quantitative tightening. Based on the minutes of the December meeting, the central bank seems poised to begin contracting its balance sheet relatively soon after interest rate lift-off.

Zoltan Pozsar of Credit Suisse last week put out a series of his Dispatches laying out analysis, opinions and questions about how this contraction will go. This is a process we will have much more to say about, so in today's post, I follow Zoltan in spelling out the mechanics of the basic question: how will the Fed's balance sheet get smaller?

Worth a thousand words

Start by recalling what the Fed has been up to since the beginning of the pandemic: some $4.5 trillion of balance-sheet expansion, Treasury and mortgage-backed securities on the asset side; reserves, overnight repo and Treasury deposits on the liability side:

I summarized the key turning points of this expansion in a recent post. Now the central bank is bringing the expansion to a halt, and at least in theory, preparing to switch to contraction.

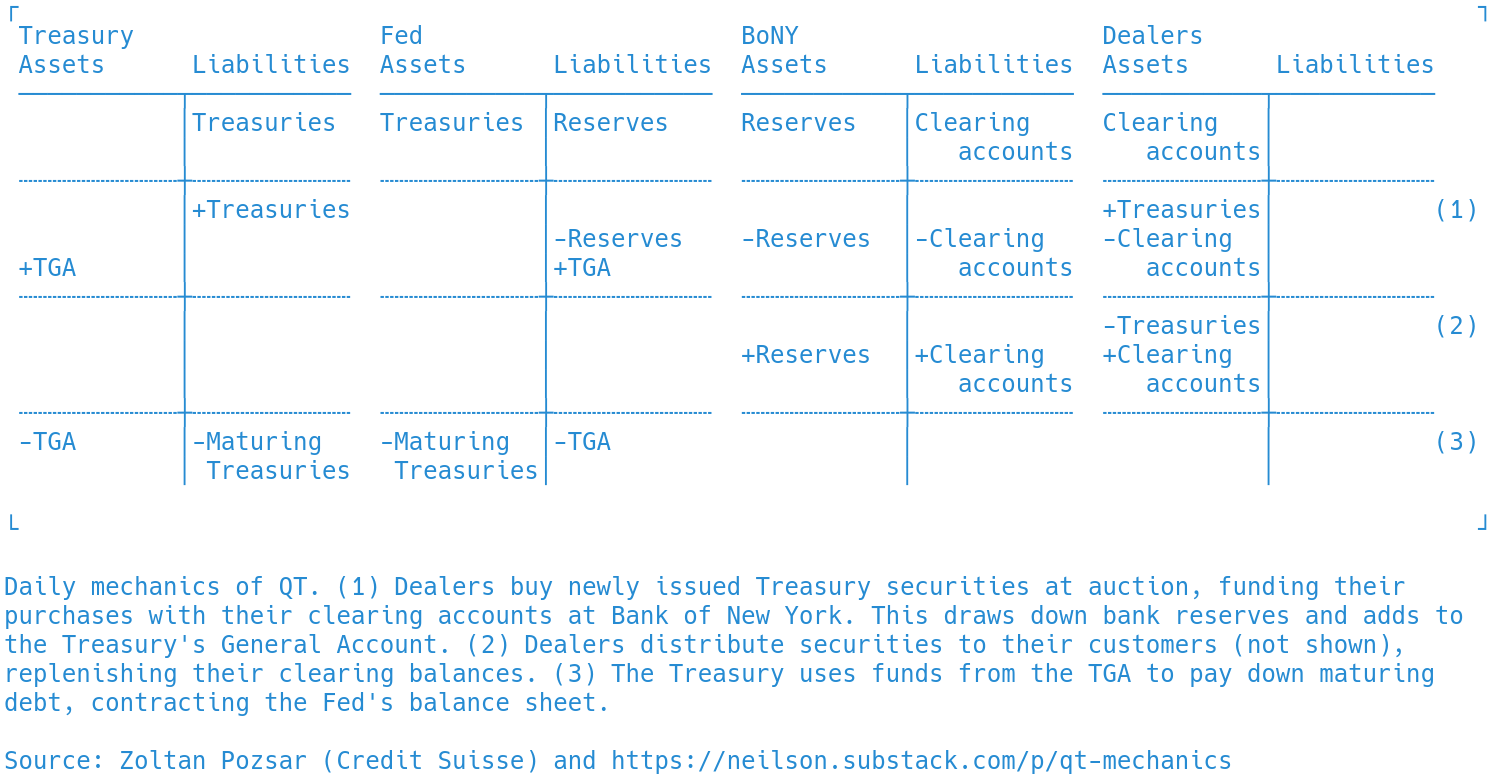

In this shorter piece from last week, and this longer one from the Fed's last attempt at shrinking its balance sheet, Pozsar maps out the transactions by which the central bank's balance sheet will actually contract. These T accounts describe the mechanics in my own style:

The process unfolds according to the Treasury's daily rhythm of borrowing and repayment. Securities dealers purchase newly issued Treasury securities at auction. They fund these purchases by drawing on their clearing accounts, which after Basel III are all at Bank of New York. BoNY draws down its reserves correspondingly, and the proceeds shift into the Treasury General Account, the US government's deposit account at the Fed. All of this is represented in step (1) in the figure.

In step (2), dealers then sell these securities to their customers, using the proceeds of these sales to replenish their clearing accounts. (The dealers' customers are not shown.) If dealers sell all of the securities that they bought, then their balance sheets are restored to their initial positions. The Treasury, finally, draws on its TGA deposits to pay down maturing securities, step (3) above. This payment destroys both the maturing securities and the TGA deposits, contracting the Fed's balance sheet.

Animated

Here is the same thing, animated (and so worth a million words?):

Big questions

As Zoltan notes, there are variations on these mechanics, which will be important for how the Fed's balance-sheet contraction plays out in money markets. Much depends on who end up being the ultimate buyers for the new Treasury securities. Banks' reserves, money funds' overnight reverse repo deposits, or both could be drained. Many other balance sheets will also have to shift, and so patterns of short-term rates are also likely to change. Finally, there is also an intraday dynamic involving the timing of the repo market. Whether or not the Fed manages all of this smoothly will be interesting to find out.

Do you know why the pdfs of Zoltan's Dispatches are no longer available at the original links? I only see a blank page when I click on them.

Why assume bond redemptions go only to the Fed? If Treasury redeems private bond holders out of the TGA, aren't reserves shifted to private banks where they survive, not disappear as claimed in the blog? Is it wrong to say that reserves are only destroyed if the TGA pays the Fed and the Fed chooses not to reinvest for arbitrary, fickle, psychological, policy reasons, not any sort of necessity?