The Fed's balance sheet during the pandemic

A tiny financial history

The financial system sometimes produces payment imbalances that are too large for private balance sheets to absorb. The origins of such imbalances might be financial, as in 2008, or non-financial, as with the pandemic. Big imbalances risk destabilizing the institutions of the payment system, so central banking practice has been to absorb them onto the central bank's own balance sheet.

The COVID-19 pandemic has been a source of (among other things) large financial imbalances, and indeed one can read something of the financial history of the last two years off the Fed's balance sheet. Asset purchases, the centerpiece of the Fed's pandemic balance-sheet policy, are now being tapered off, and with concerns intensifying over recent inflation measures, tapering may now unfold even more quickly than was envisioned at the November FOMC meeting. All this is to say that we are at another turning point, and so it is a good time to check in on the central bank's balance sheet.

Four turning points

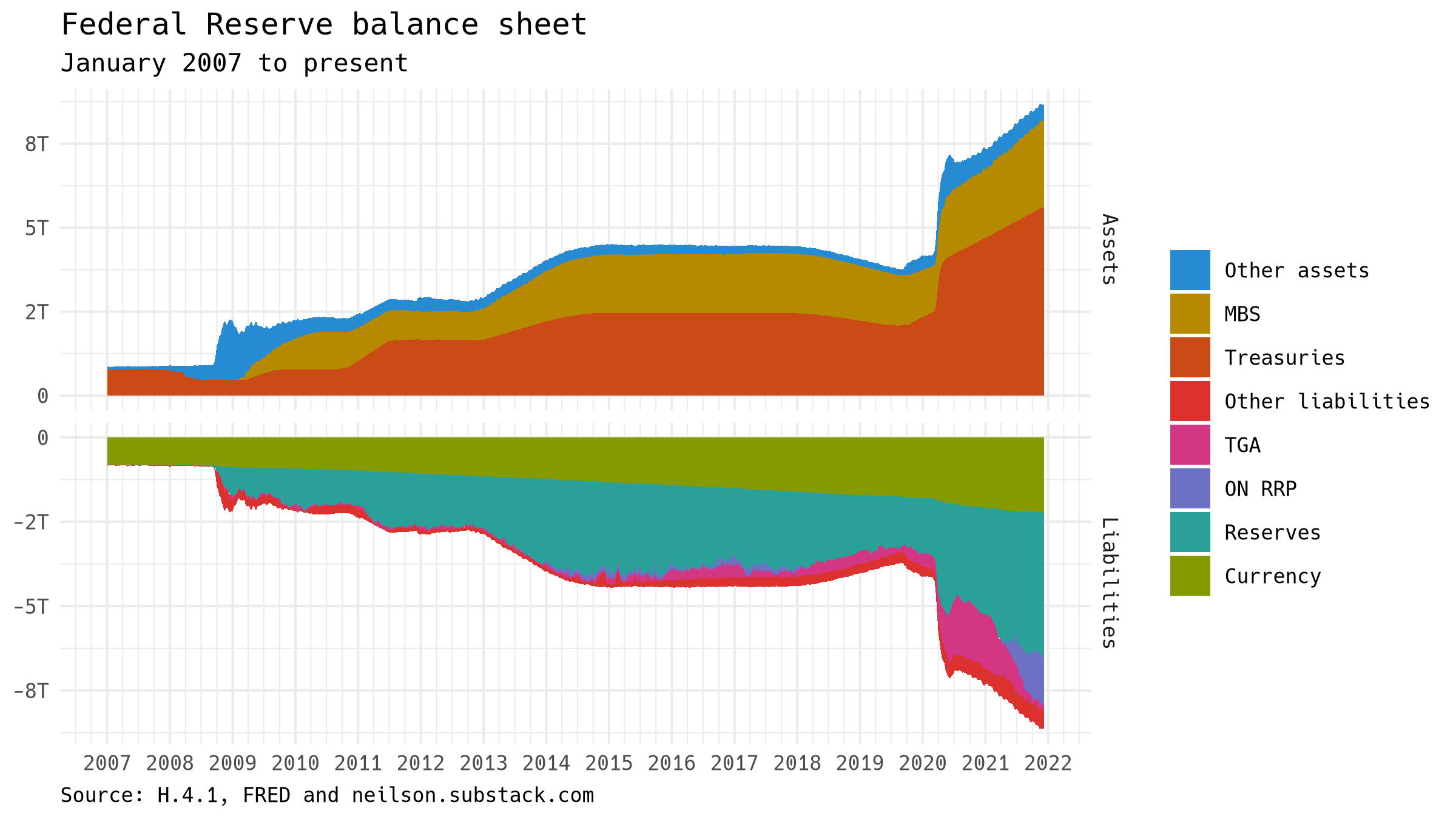

The graph below is my preferred visualization of the Fed's balance sheet. It shows what are (in my view) the key entries, those that are large in dollar terms and most significant for understanding what the central bank is doing. Assets are in the upper panel, liabilities below as negative numbers. The balance sheet balances, so at each moment in time total assets equal total liabilities; or geometrically speaking, the outer limits of the graph are symmetrical. Every entry not shown individually is grouped into the "Other" categories, either assets or liabilities, and so the total balances to the Fed's published H.4.1 release.

Using the Fed's balance sheet, we can define four financial turning points since the beginning of the COVID-19 pandemic, marked with vertical lines in the graph. The first came in March 2020, when (as we will not soon forget) it became widely recognized that the pandemic was going to be a big deal. The Fed rapidly expanded its balance sheet by some $3 trillion, purchasing Treasury and mortgage-backed securities on the asset side, funded by expansions in reserves and government deposits (TGA) on the liability side. The bump in the other assets category comes from about $400 billion lent via the FX swap facility.

We could draw the second turning point in July 2020. That proved to be the high-water mark for government deposits, and the FX swap facility was drawn down. By that point, the world was into the pandemic proper, and the Fed had likewise settled into its asset-purchase program of $120 billion per month, the pace that was to continue until the end of 2021.

The third turning point came in March 2021, one year into the pandemic. This was a more purely financial transition, one that does not map neatly onto non-financial developments. It was at that point that the supplementary liquidity ratio began to bind for banks. This meant that further asset purchases by the Fed would have to be matched by a different entry on the liability side. The ON RRP facility, which already existed and had been used in a limited way early in the pandemic, provided the needed entry, and bank reserves largely stopped growing at that point.

The fourth turning point I place, for the time being, in November 2021, with the beginning of the tapering of asset purchases. The taper is hard to see in the graph above, but is more visible below, where the components are shown separately. The line for Treasury securities becomes perceptibly flatter. (MBS purchases are also being tapered, but with the monthly repayment cycle, it is harder to see.)

A longer arc

It is helpful to frame the Fed's balance sheet during pandemic period, but at the same time we should not forget that history is not so neatly organized: in early 2020, the Fed was already responding to disruptions in the repo markets that had peaked in September 2019. That period is visible in this longer view:

And all the way over there on the left, we can see the 2008 crisis, the details reduced here to "Other." The 2008 crisis provided the Fed's template for responding to COVID-19, different though the circumstances were.