The 2008 crisis, part 1

Tales of crisis past

This is the first part of a short financial history of the 2008 financial crisis. Part 2 is here. Part 3 is here. All of the crisis facilities are depicted as animated gifs here.

The global financial crisis of 2008, still sometimes called the subprime crisis, which kicked off the Great Recession, is now more than a decade gone. The exigencies of the COVID-19 pandemic have pushed the 2008 crisis further into memory and history.

But much of today’s political-economic configuration comes out of the 2008 crisis. And while no two financial crises are identical, there is surely a family resemblance. Financial crises are very similar at a high level and very different in the details. Even as new issues command our attention, it would be foolish to forget what happened in 2008.

So I thought it could be helpful to offer a simple, but accurate and coherent, financial narrative of the 2008 crisis. This version is compact enough that it can be remembered and, when needed, recreated on a napkin or a chalkboard. It is, I think, accurate in the financial substance. Many details are omitted, but if you remember the T accounts, you will have a place in your memory for the details.

This version draws heavily on this paper that I wrote with Perry Mehrling and David Grad, and which is closely connected with Mehrling’s book The New Lombard Street. It also draws on this paper on market-based credit. I offered a parallel account of the crisis in context in the first chapter of Minsky, but this Soon Parted version zeroes in on the financial mechanics of the crisis itself.

Stress in market-based credit

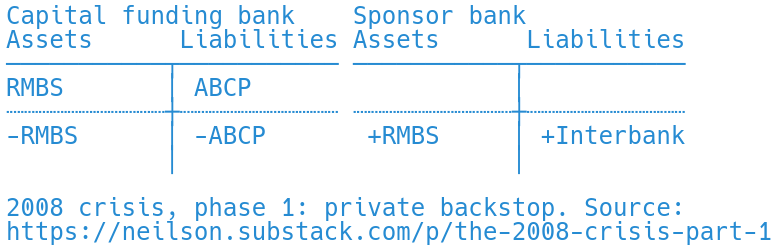

The basic financing failure that initiated the crisis was this: capital funding banks had built up substantial positions in US residential mortgage-backed securities, financed by issuance of asset-backed commercial paper. This was typical of the market-based credit system that had come to dominate US financial activity in the decades preceding the crisis:

“Capital funding banks” is an informative name for what have more colorfully been called “shadow banks.” Before the crisis, they were legally formed as off-balance-sheet entities called special purpose vehicles (SPVs) or structured investment vehicles (SIVs).

Importantly for the crisis that was to follow, this arrangement was based on marketable securities on both the asset and liability sides. Like any bank, the liabilities were of shorter maturity and higher liquidity than the assets. So capital funding banks were vulnerable to runs. The ABCP was funded by issuance of even more liquid claims, in an economic function that could generally be called “money dealer.” This role was played by different entities at different times.

Capital funding banks wanted to exit these positions starting in summer 2007. It had become clear that the US mortgage lending was overextended, and it became impossible to roll over ABCP positions.

At this pre-crisis stage, capital funding banks’ exit from their positions was facilitated by arrangements with their sponsor banks: the off-balance-sheet vehicles fell back onto banks’ balance sheets. As ABCP funding matured and could not be renewed, the sponsor banks absorbed the RMBS position, financing themselves in interbank markets with LIBOR as the marginal cost of funds. One of the first signs of the crisis was a spike in the spread of LIBOR over the Fed Funds rate.

Because the refinancing problems were in marketable securities rather than non-marketable loans, securities dealers also became involved. Here I show two kinds of dealer. Securities dealers were willing to absorb the flow out of RMBS so long as they could finance it in repo markets. Money dealers wanted out of their ABCP positions but were, at this stage, still willing to hold the MBS repo though at elevated rates.

End of the beginning

In the early weeks of what was to become the 2008 crisis, the private dealing and banking systems were able to manage the flight from the RMBS and ABCP markets. The strain was visible in interbank and repo lending rates and liquidity conditions.

When Bear Stearns failed in March 2008, it became clear that these private mechanisms could not extend any further. This marked the end of the first phase of the crisis.

Please subscribe

There will always be another financial crisis! Sign up to get Soon Parted in your inbox so you don't miss it:

Neil, I just discovered your page here, I'm having a blast going through all your previous posts. Right, so I started to read your paper with Mehrling and Grad (The evolution of last-resort...), but I got stuck in figure 1 there. (USD overnight rate spreads x fed funds): How come the treasury repo rate spiked below the fed funds? Can you expand a little bit on that? Thanks