Do central banks borrow?

Three "Yes, but ..."s

A Soon Parted reader has invited me into a long-running—interminable?—debate over how to interpret central bank money.

It seems that most contributions to this debate want there to be a single-point answer of some kind: the Fed should not pay interest on reserves; we should account for central bank money differently; the central bank should fiddle with its dividends. These arguments have more than a whiff of chiropractic money: "if we could just shift this one thing..."

Money is never just one thing; it is a complex social phenomenon involving history, institutions, behaviors and relationships. There are reasons that these are the way that they are. We certainly are not obliged to like it. But pretending that things are simple—when plainly they are not—doesn't help anything.

All this runs the risk of being unhelpfully abstract. Let me put some arguments on the table that could be helpful in this debate.

Central bank funding

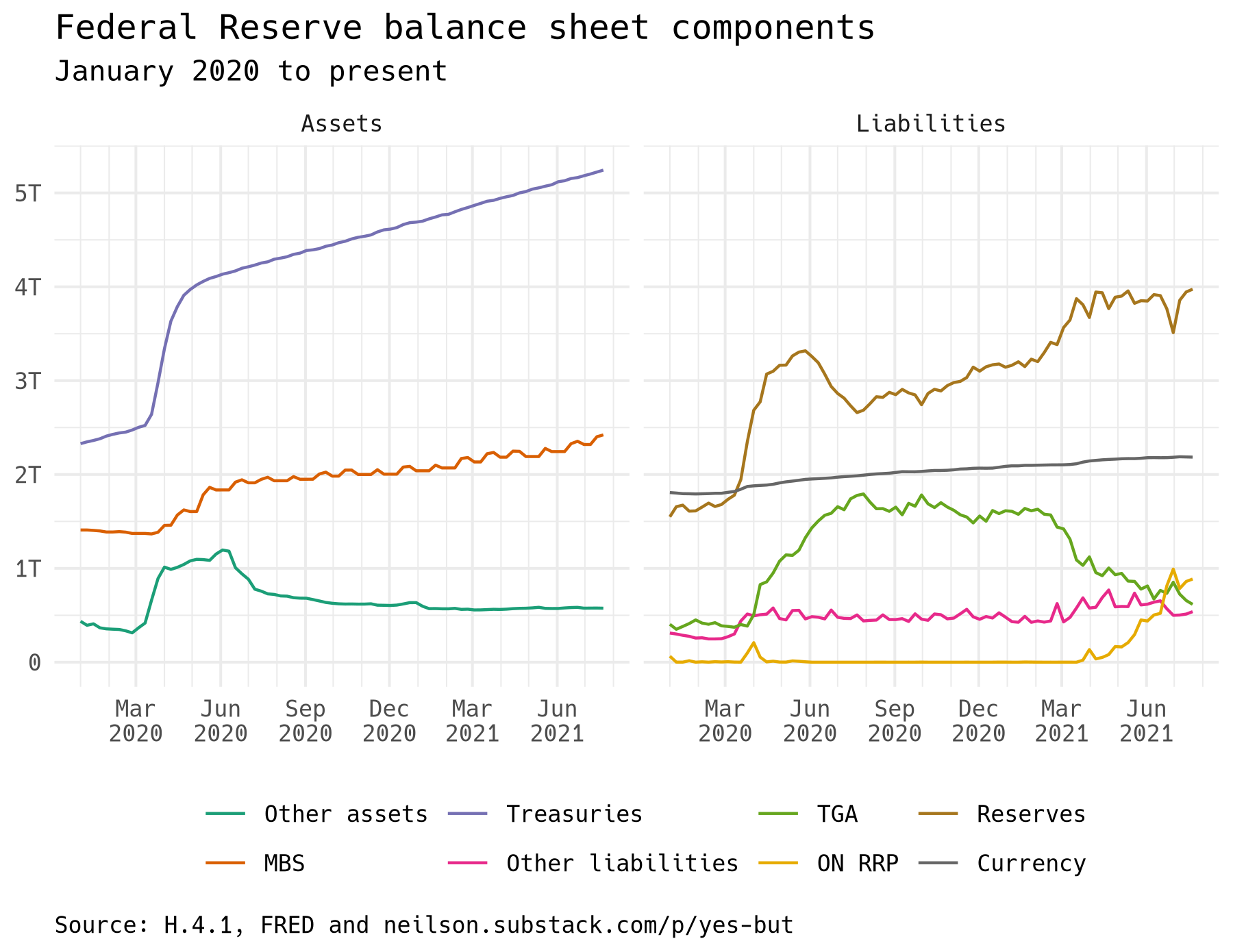

Start, as Soon Parted often does, by looking at the balance sheet of the Federal Reserve. These are the figures published by the US central bank each Thursday in its H.4.1 release. I create the series for "Other assets" by subtracting Treasuries and mortgage-backed securities from the Fed's "Total assets" series, and likewise for "Other liabilities." As a result, everything on the H.4.1 release is here. Total assets and total liabilities are equal at each point in time, about $8.2 trillion as of last week.

Since the beginning of the pandemic, the lines for Treasuries and MBS, on the asset side, have been climbing at a steady pace. Together, the growth in these two asset positions represents the $120 billion-per-month in quantitative easing that has been the centerpiece of US monetary policy during this time. Note that all three of the asset series—Treasuries, MBS, and everything else—are smooth. (There is a cyclicality in the MBS series having to do with monthly mortgage issuance and repayment, which I still count as "smooth.") On the liability side, by contrast, the lines for reserves, overnight RRP, and the Treasury general account are not smooth. Fluctuations elsewhere in the banking system cause these liability entries to rise and fall. But the balance sheet balances, assets equal liabilities, so the unsmooth lines on the liability side add up to the smooth lines on the asset side.

There is something very specific happening here: the Fed is making a market between its various liability positions to ensure smooth exchange between bank reserves, overnight RRP with money funds, and Treasury deposits. As the US Treasury has spent down its account, for example, that spending ends up as an asset to someone else, deposited in a bank. So the reserve line rises, and the other liability line wobbles, together offsetting the fall in the TGA (visible in the graph especially from June 2020 to March 2021). The Fed cannot control this. More recently, as banks' reserve positions have maxed out (due to newly binding liquidity ratios), the Fed has opened up an alternative channel, the ON RRP facility, to serve the same purpose but with money funds, rather than banks, as the counterparty.

One conclusion to draw from this is that the asset side and the liability side are closely connected. The Fed is choosing its asset portfolio by buying securities, which sets the size of its balance sheet. It then accommodates everyone else by facilitating adjustment in the composition of its liability portfolio. Note that a single bank can reduce its holdings of central bank reserves, for example by using them to pay off debt. But that only transfers the reserves to someone else. Central bank money is destroyed only when the central bank itself contracts its balance sheet, on both sides. That is true for central banks and not true for other borrowers, even other banks, from which lenders (depositors) can withdraw funding.

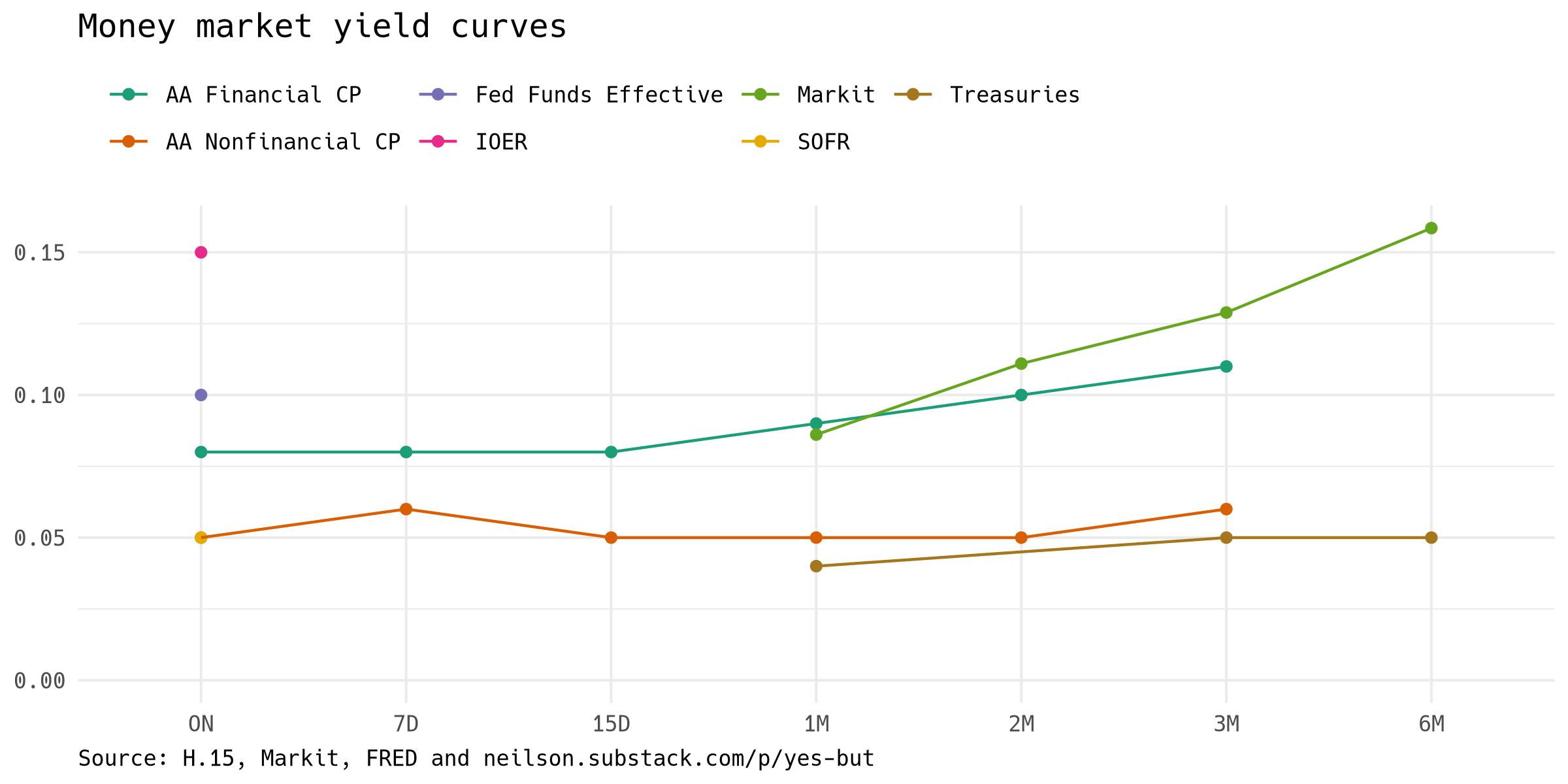

Central banks and the money markets

Reserves and overnight repo are closely connected to other short-term instruments by arbitrage relationships, as this graph of various short-term interest rates shows. The greenish-blue curve, for example, shows Friday's market rates for commercial paper for financial borrowers at tenors from overnight to three months.

At the left edge of the graph is a stack of overnight interest rates. Note the Fed's interest on excess reserves rate, at 15 basis points, the Fed Funds effective rate, at 10 bp, and the secured overnight financing rate, which is a market average currently determined by the Fed's overnight RRP facility. The commercial paper curves reach their overnight endpoint right between SOFR and Fed Funds.

When commercial paper, repo or Treasury bills mature, the borrower settles up by delivering funds at the central bank. What the graph says is that, money tomorrow is worth about the same as money a week, two weeks, a month from now, even in these markets with trillions of dollars of flow. The central bank is succeeding, at the moment, at stabilizing short-term interest rates. But that success is not guaranteed!

Yes, but ...

Do central banks borrow? Yes, they borrow by taking deposits from the banking system, using the proceeds of that borrowing to purchase assets like any borrower. But, distinct from other borrowers, central banks' depositors cannot, in aggregate, stop funding the central bank: there is not, in aggregate, somewhere else that their funds could go.

Is the central bank a bank? Yes, central banks buy assets and sell circulating liquid liabilities that can serve as money like other banks. But, distinct from other banks, central banks' liabilities serve a privileged role at the core of the payment system, so central banks can ease the survival constraint even when no one else can.

Is central bank money special? Yes, central bank liabilities are used for final settlement in ways that other banks' liabilities are not. But, central bank liabilities are part of a group of short-term money-like instruments. These are often close substitutes, as they are now. Even so, a 1 or 2 bp move can cause trillions of dollars' worth of flow through the money markets. Alternatively, those same spreads can widen suddenly when money markets break down, as they occasionally do.

All this said, talk is cheap. Better to watch what central banks (and other banks and governments and money markets) actually do.

First, may I say that I greatly appreciate your use of balance sheets and dealer model diagrams to tell your stories, though I may disagree with some of the morals you derive from the stories?

Second, when you say "[central banks] borrow by taking deposits from the banking system, using the proceeds of that borrowing to purchase assets", haven't you reversed causality? If I am AIG with toxic MBS assets that can't catch a bid on private markets, then the Fed acts as a value investor and fills my coffers with reserves, are you saying those reserves came from other banks' deposits? But didn't they really come out of thin air? The reserves were created first, then used to buy assets no one else wanted at that price? Nothing was "borrowed" from anyone?

Third, is your criticism of chiropractic money itself chiropractic, in the sense that you ignore complex nuances of Lonergan's "dual rate" proposal (note that dual rates are an explicit policy of the ECB), unfairly reducing his views to "if we could just change this one thing"? Are you criticizing the mote in another's eye while ignoring the log in your own?

Fourth, regarding your earlier "Cars and Chips" blog on inflation, aren't expectations of inventory the real driver, and can't the Fed control inflation expectations as needed by buying and selling inflation swaps as part of open market operations? So emotional misestimations of future inventory shortages can be mitigated by compensating buyers for irrational price increases?