Ledger

Monetary technologies #2

169—Ledger

Monetary technologies #2

Daniel H. Neilson

2023-06-16

This post is part of a Soon Parted series on monetary technologies. Crypto ushered into public view a wave of financial novelty, capturing the collective imagination with white papers, prototypes, proofs of concept, a couple of genuinely new ideas, and some potentially instructive failures. Now banks, exchanges and regulators are trying to find out whether any of that novelty could be incorporated into the monetary infrastructure.

Until crypto, the word ledger had been primarily reserved for accountants. The bitcoin and ethereum blockchains have turned out to be examples of a broader class of “distributed ledgers,” not all of which have the particular structure of a blockchain. In this post, I try to see ledgers at their most general. This makes it easier to say what it means for a ledger to become distributed, and why this might matter.

The omniscient ledger

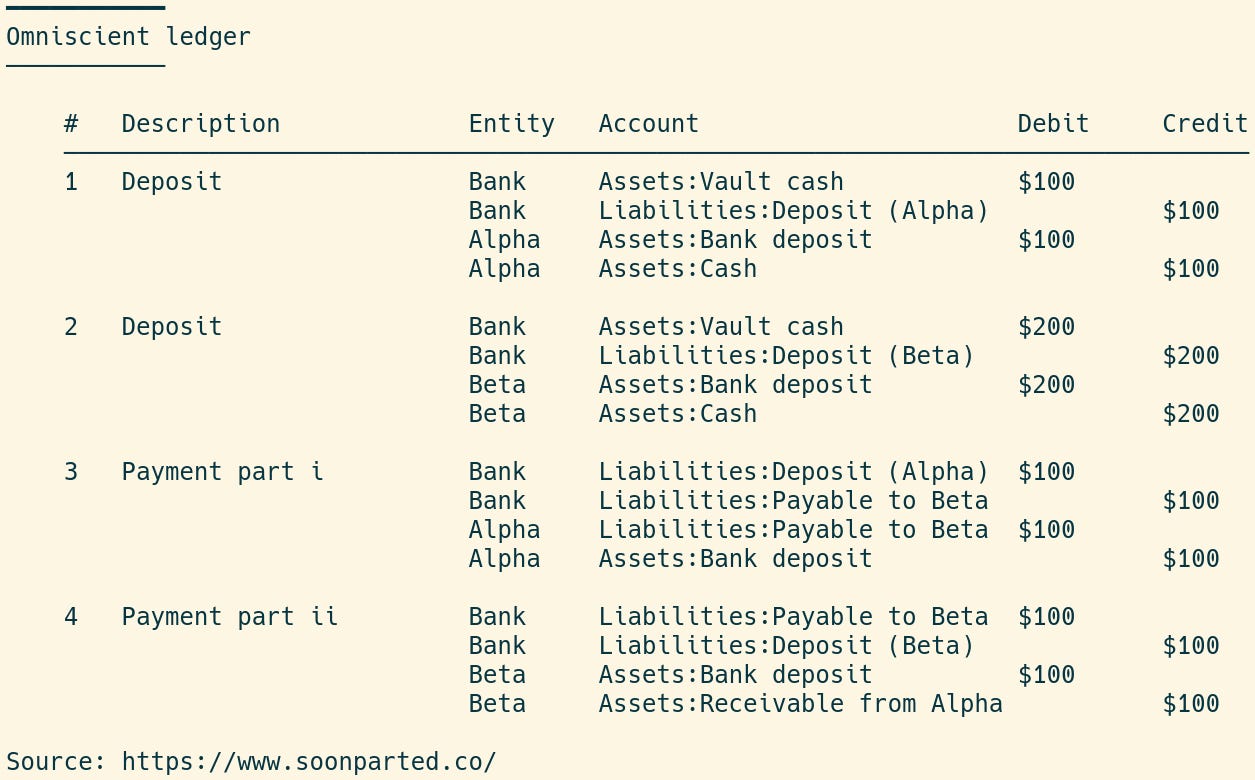

We can think of any particular ledger (a firm’s general ledger, or the bitcoin blockchain, to take two examples) as deriving from a unique, hypothetical master ledger. While we are imagining, we may as well suppose that the master ledger describes all transactions in the entire economic system. To be comprehensive, it would need to show both sides of every transaction, simultaneously and coherently. For this reason I call it “omniscient” to capture the idea that it is a single ledger that reflects the point of view of all economic entities.

The omniscient ledger has to include the two double-entry representations that record each transaction from each entity’s point of view. Each transaction in the omniscient ledger will therefore have four entries. This figure shows four transactions (thus sixteen entries) from such an omniscient ledger. Both counterparties record one debit and one credit entry for each transaction. Each entry gets one row in the ledger, identifying the entity, the account name, and the dollar credit or debit amount.

Note, there are not four different things happening in each transaction. There is one thing happening in each transaction, seen from two perspectives and understood as originating somewhere and going somewhere.

There are practical complications (What if the two parties disagree on the valuation? What about capital gains? What if there are more than two parties to the transaction? What happens if you set fire to a trash can full of paper money?). I stand with my accountant friends in the belief that these quibbles all have very neat resolutions, the details of which I will leave aside for now.

A firm’s general ledger

One can imagine this omniscient, quadruple-entry-consistent ledger encompassing all market transactions, but in practice it cannot be constructed. One place where they show up, in approximation at least, is in macroeconomics, where the entities are consolidated into sectors: rather than a firm Alpha in the example above, one might have a sector like “private nonfinancial business.” Macroeconomic accounting records the sources and uses for all sectors simultaneously, and the underlying ledger has exactly the form of the example above.

The concept of an omniscient ledger has other uses, however, because all non-omniscient ledgers can be derived from it. For example, a firm Alpha’s general ledger is exactly the subset consisting of all entries in the omniscient ledger for which Alpha is the counterparty. Alpha’s accountants may not know the rest of each transaction, but they can certainly know their own half of it. Indeed, each party to the transaction can see the two entries that exist on its own books, one debit and one credit. Sometimes, one needs to be sure that certain entries agree between parties, which has given rise to various processes of reconciliation. We could say that reconciliation is a means by which two entities confirm the quadruple-entry consistency of transactions they have in common.

Distributed ledger

The bitcoin and ethereum blockchains are examples of distributed ledgers. Like a firm’s general ledger, a distributed ledger is a subset of entries from the omniscient ledger. Unlike a firm’s general ledger, in a distributed ledger each transaction shows entries from two different entities. One of these records the transaction as a debit entry, the other as a credit.

Each transaction therefore has a kind of double-entry consistency. But it is not the usual double-entry consistency that applies to the books of a single entity. Rather, the distributed ledger shows the flows between entities.

For any transactions that are on-chain (those that are tokenized), there are not two ledgers that must be reconciled; instead there is just one, a canonical, single source of truth. A transaction can not be recorded in the distributed ledger unless it balances, so there is no need for further reconciliation.

Eliminating reconciliation may be a benefit, but there are costs too: a potential lack of privacy, for example. Current experimentation with distributed ledgers will eventually have to resolve the question of how the benefits and costs stack up.

Monetary technologies

Ledger (this page)