Inventories and supply chains

Beyond supply and demand

Inflation continues to dominate discussion economic of the macroeconomic effects of the pandemic. Central bank intervention, government spending, and pandemic safety nets are all being judged by their relationship to price-level movements. It becomes harder to ignore the shortcomings of our theories of inflation.

Most theories of inflation from economics are based on a supply-and-demand conception of exchange: high prices entice sellers and discourage buyers, while low prices do the opposite. In between, there is a price that equates supply and demand, and this is the only price that clears the market. This is so whether it is a micro theory of a single market, or a macro theory of aggregate exchange.

The supply-and-demand view imposes a narrow view of production: final demand arising from households, and supply arising from a single productive sector. The COVID-19 pandemic has called attention to the much more complex reality of supply-chain production. This post looks at some of the big-picture supply-chain effects, which could inform a better theory of inflation. The inspiration for this approach comes from a little-known book by John Hicks, A market theory of money (ch. 3, if there are any fans reading).

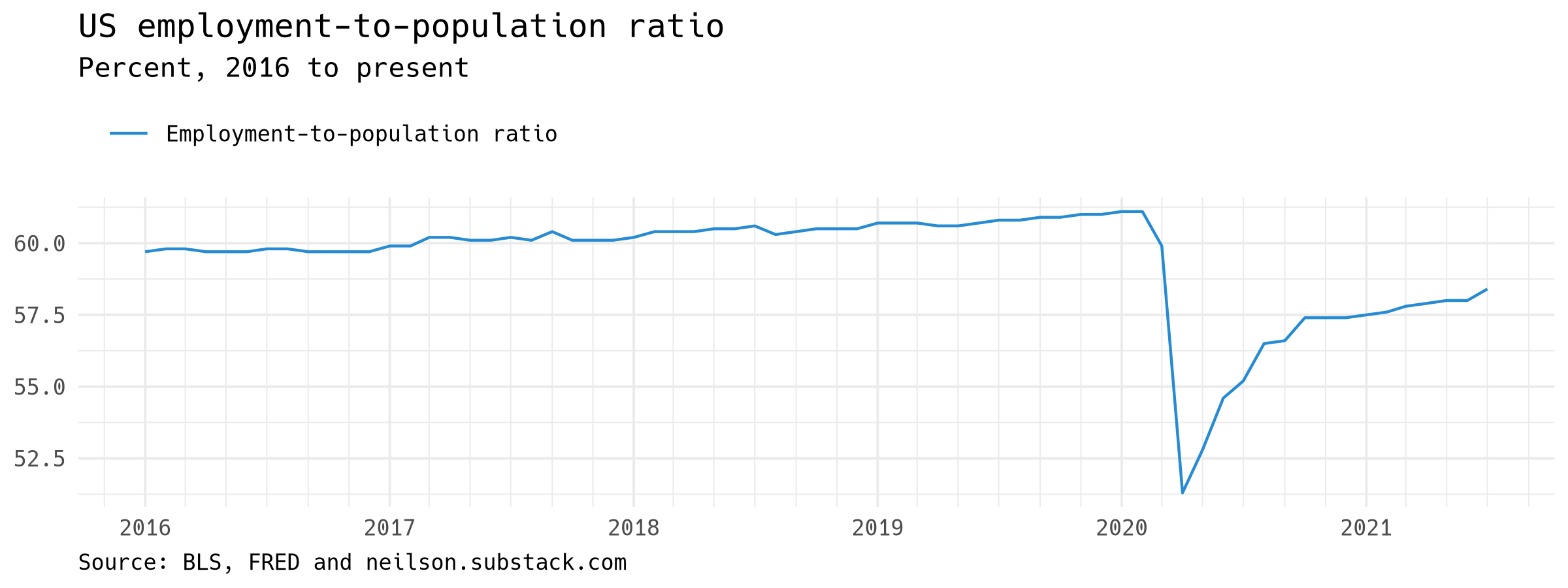

Employment

The immediate impact of the pandemic on economic activity was through the imposition of public-health limitations on physical proximity. This graph shows the US employment-to-population ratio. For context I show the series going back to 2013:

Labor is perhaps not part of the supply chain per se, but it seems important to include it here. Employment is an input to production processes, but unlike raw materials, works in process or finished goods, it cannot be stored as inventory: it can only be employed or unemployed.

Inventories across the supply chain

This graph shows manufacturers' inventories of inputs, work in process, and outputs. Again, I've shown the series back to 2016 for context, but look especially at how these measures have developed over the course of the pandemic: inventories of outputs—goods ready for sale (the green line)—dropped quickly in early 2020, while inputs and goods in process held steady. To me that seems to be the direct effect of pandemic restrictions: production slowed because people could not be together, so stores of finished goods were run down. Purchases of inputs must have slowed as well, or else the blue line would have spiked in early 2020 as well:

Then, starting in the middle of last year, manufacturers' inventories of both inputs and outputs began to rise steeply. Inventories of work in process have risen, but much less steeply. How should we interpret this? It seems to suggest that activity is picking up, causing manufacturers to stock up on inputs, but that supply chains are clogged, so outputs are also piling up.

This supply-chain perspective helps make sense of the graph below, which shows the path of inventory-to-sales ratios (months of inventory) by supply-chain sector for the US. The onset of the COVID-19 pandemic in 2020 corresponded to a spike in all three sectors. This could correspond either to a rise in inventories, the numerator of the ratio, or a fall in sales, the denominator.

For manufacturers, at least, we know from the second graph above that at least some inventories were in fact falling. So for the inventories-to-sales ratio to fall, sales must have fallen even faster. Since the middle of last year, the pattern has continued to shift, with manufacturers currently holding higher, wholesalers lower, and retailers much lower inventories than before the pandemic.

Implications for inflation

The pandemic demonstrates the limitations of the supply-and-demand perspective. None of what these graphs show can be narrowly categorized as being a simple shock to either supply or demand. Instead, production has been impacted in a variety of ways across different supply chains. We can tell that these effects are driving prices, but economic theory doesn't have a good way to make sense of this fact systematically.

"I think that the price level and rate of inflation are literally indeterminate. They are whatever people think they will be. They are determined by expectations, but expectations follow no rational rules. If people believe that certain changes in the money stock will cause changes in the rate of inflation, that may well happen, because their expectations will be built into their long term contracts."

Fischer Black, "Noise"