PBOC easing part 2

Foreign currency reserves of Chinese banks

Late last month the PBOC made two policy moves to ease monetary conditions in China, following a string of negative economic signals. Last time I wrote about the first, a reduction in mortgage rates for first-time homebuyers. The second move was to lower the reserve requirement faced by Chinese banks on their deposits denominated in foreign currency. In this post, I try to establish the mechanics of those reserves, and to see what is the range of possible outcomes of reducing the reserve requirement.

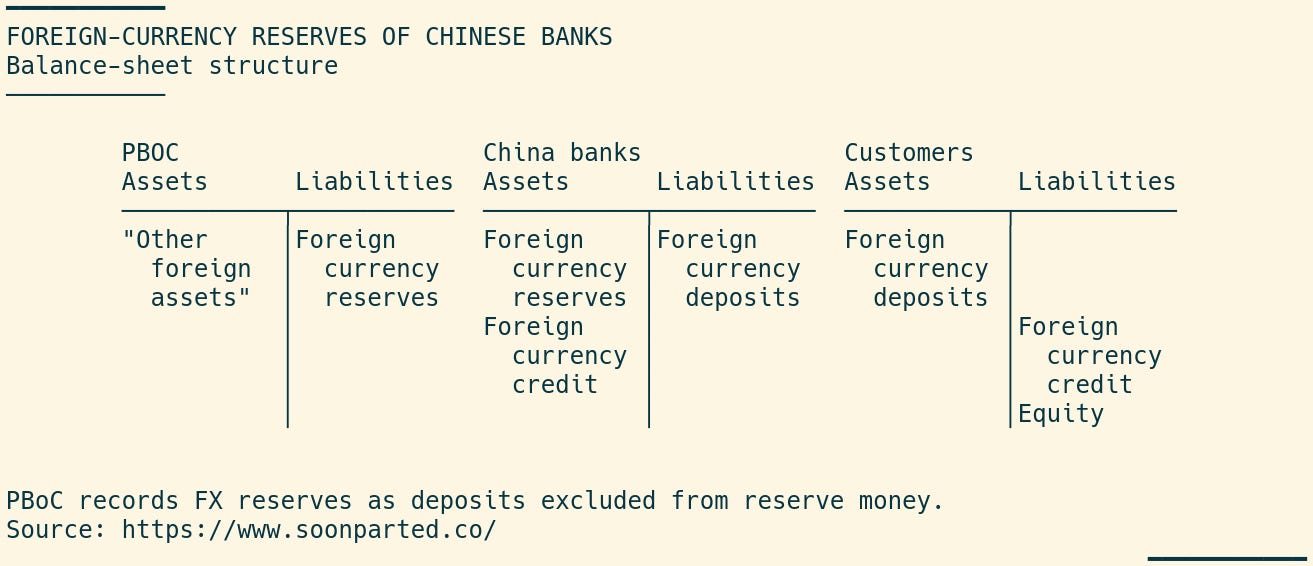

It strikes me as unusual that the PBOC requires Chinese banks to post specific reserves on FX deposits. I’m not aware of other countries where such a requirement exists. Offshore deposits are in general a private affair, neither protected by public deposit insurance nor specifically regulated. The mechanics are therefore apparently unique. A 2009 CFR piece by Brad Setser and Arpana Pandey, on related matters in a different context, offers a framework that seems to be mostly correct.

Chinese banks are required to post reserves at the PBOC against their foreign-currency deposits. These deposits are substantial, at $822 billion as of July 31 2023. Setser and Pandey suggest that the PBOC holds these reserves in the form of securities, and records them separately from the main FX reserve portfolio (as “Other foreign assets”). The balance-sheet relationships must be something like this:

The main issue here is that the Chinese central bank itself is not an issuer of dollars. So if the PBOC is imposing a reserve requirement on deposits denominated in foreign currencies, what instruments are being used? It seems likely that Chinese banks must pledge FX-denominated assets as reserve deposits, US Treasuries for example. The PBOC holds these, recording them both an asset (the pledged securities) and a liability (the obligation to return those securities to the bank).

What then does this mean for the reduction in the reserve requirement on foreign currency deposits? Possibilities are two. If Chinese banks sell their reserve assets, buying RMB assets, that will in general be supportive of PBOC’s goal to limit dollar appreciation, which increases input costs for Chinese businesses. But, as has been widely reported, the actual amount of dollar assets freed up this way is fairly small, in the tens of billions of USD, and likely not enough to make much difference to the exchange rate.

An alternative view, consistent with the balance-sheet analysis above, is that the reduced reserve requirement would allow Chinese banks to create a greater level of dollar deposits on the same base of reserves. If depositors could be satisfied with offshore dollars created within the Chinese banking system, the policy change would address pressure on the exchange rate, because the supply of dollars would be increased. The effect is much bigger, in the hundreds of billions of dollars. The risk is that Chinese banks may struggle to honor those promises, with fewer dollars in reserve. In a possible future rush for the exits, more substantial FX intervention would then be required from the central bank.

If any readers have more on these mechanics, please drop me a line.