One BRICS short

The BRICS bank tries to get out from under the dollar

How does one escape dollar hegemony? The question vexes finance ministers and central bankers everywhere, except in the US of course. The dollar is the dominant currency of international trade and financial flows, so issuers of sovereign debt must constantly attend to exchange rates, the price of their own money in dollar terms. Borrowed dollars will be repaid using funds collected in local currency, and so the real cost of that borrowing depends on the exchange rate. The risk is always that dollars will become more expensive, making debt harder to repay.

The New Development Bank, also known as the BRICS bank, has declared its intention to chip away at this challenge on behalf of a plucky group of challengers. Dilma Rousseff, former finance minister of Brazil and now leader of the bank, said in an interview with the Financial Times that the NDB would try to make 30% of its loans in local currency this year. At the same time, the NDB is expanding, with invitations extended to six prospective member countries. Would an enlarged BRICS bank stand a chance of freeing finance ministers from having to worry about their dollar-denominated debts?

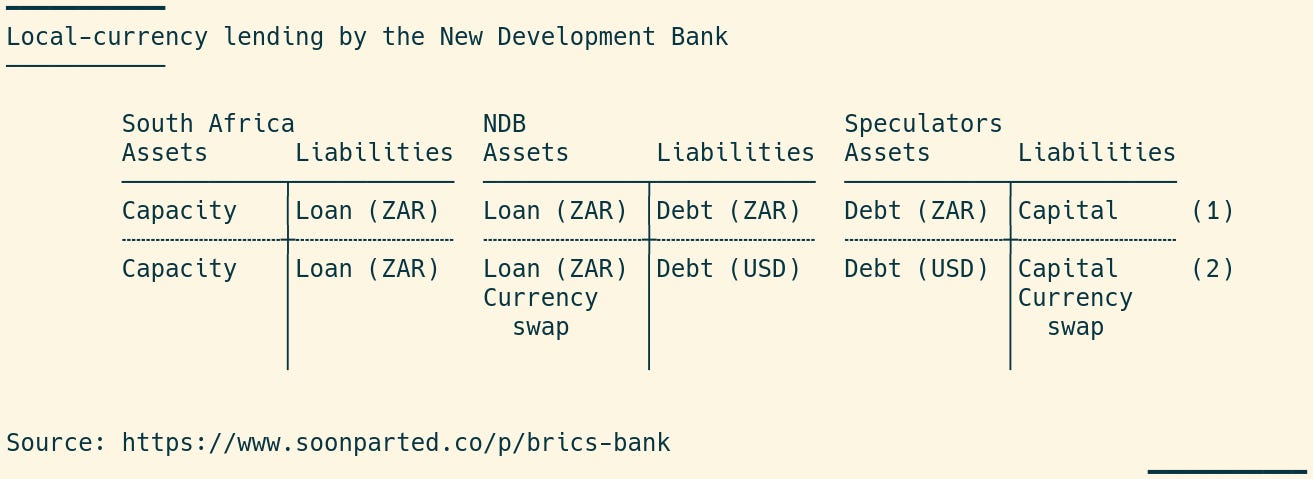

Rousseff mentions two concrete possibilities: the NDB could fund lending with its own local-currency debt, or it could sell exchange-rate protection in the currency swap market. The T accounts below describe the possibilities. In row (1), the NDB makes a loan to the government of South Africa, denominated in South African rand (ZAR). The NDB could in turn issue its own ZAR-denominated debt. I show such debt as being held by “speculators.” (The identity of these speculators is the central question, to which I return to it below.)

In the second row, the NDB could instead issue dollar-denominated debt. This creates the possibility that the loan repayments received in rand on the loan would be insufficient to cover the NDB’s own dollar obligations, essentially an exchange-rate risk. To hedge this risk, the NDB could buy protection in the form of a currency swap, a derivative transaction that would, in effect, lock in a future exchange rate. I show the NDB holding the swap as an asset, thinking of it as protection against loss on the ZAR asset position, though it could be that rates move the other way.

Who is on the other side of this swap transaction? Again, I imagine “speculators” as willing to bear exchange-rate risk by taking the other side of the currency swap position.

For either plan to work, there does have to be such a speculator, someone willing to buy rand-denominated bonds. Who? It could be someone in South Africa, where an investor might indeed be perfectly happy to hold assets denominated in rand. But then why bring in the NDB at all? The same speculator could just hold South African sovereign debt directly. It could instead be international speculative capital, hedge funds in New York. But such investors are profit-driven, and would charge a premium for offering protection. The NDB would have to cover that cost, and the ultimate source of funds would have to be the member countries—South Africa itself.

A third possibility, by far the most interesting in political-economic terms, is that the bank could sell FX risk to other NDB member countries. This would mutualize the exchange-rate risk, sharing it among several countries. It is not impossible that an expanded BRICS bank could galvanize some political-economic will, inducing its members to help each other bear risk as part of a path to greater economic self-determination. The dollar would be gradually demoted in favor of multilateral arrangements.

Is this likely to become a reality? Today's system is built around the dollar, overwhelmingly so. Even representing nearly half of the world's GDP, NDB members face a steep challenge in trying to construct alternatives, which will seem doomed to failure or irrelevance. Still, when systemic change comes, it may well come quickly. It would be foolish to discount the possibility.