Plumbing for tokenized finance

R3’s Corda project

Trying times for stablecoins. The collapse of TerraUSD, and the weakening of Tether’s peg to the US dollar, attracted a lot of attention, including from Soon Parted. This has coincided with a general crypto malaise-though not yet a rout.

Less visible shifts are also underway. Last week, Japanese lawmakers passed a bill affirming that issuance of stablecoins is a regulated activity, and that issuing entities must submit to oversight as banks, trust companies, or money transfer agents. This is consistent with the perspective of IOSCO, whose March 2022 report mapped crypto terms into existing regulatory language. That makes it easier for Japan’s FSA to now simply say “stablecoins are bank deposits.”

Covering the new law, the FT’s Leo Lewis and Kana Inagaki note in passing the announcement of a plan from Japanese bank Mitsubishi UFJ to create a platform and token system called Progmat. The details of the plan seem to be available only in Japanese—so if any Soon Parted readers can find or create a translation of this document, which seems to describe Progmat’s plumbing, please let me know!

The secret sauce seems to be Corda

So I don’t know too much about the financial structure of Progmat itself. But it seems that its technical layer is built on R3’s Corda distributed database platform. This piqued my interest, because R3 also provided the infrastructure for two separate cross-border CBDC prototypes from the BIS. That means that the company has worked with teams from the BIS and at least half a dozen central banks. Now, R3 shows up again, working with Japan’s largest bank on the exquisitely timed rollout of a wholesale distributed ledger system.

Clearly, R3 is doing something that works for those inside the regulatory fence. I set out to learn what that is.

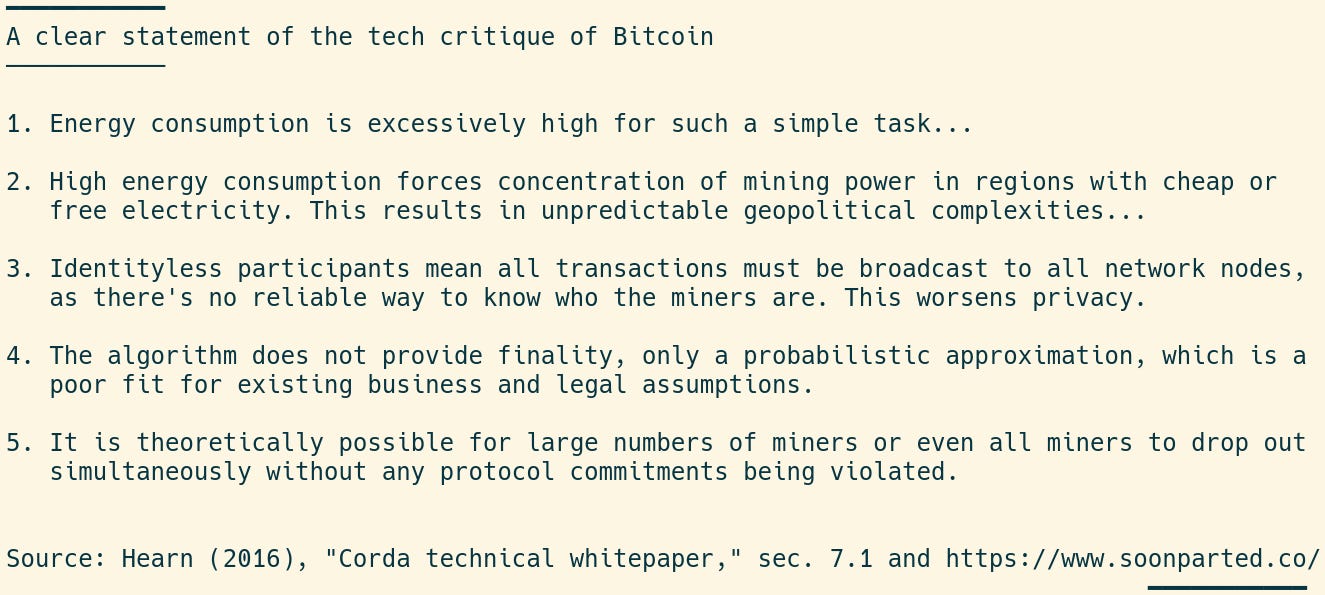

Corda offers a readable technical whitepaper by Mike Hearn, lead engineer for the Corda project until early 2021. Before that, Hearn was an early Bitcoin developer, and corresponded as early as 2009 with Bitcoin’s pseudonymous creator Satoshi Nakamoto. I mention this pedigree because Hearn’s Corda paper offers a clear and concise critique of Bitcoin, on crypto’s own terms—from one software engineer to another. I have reproduced it, slightly condensed:

These are good arguments against Bitcoin, and in various ways and to varying degrees against Ethereum and other public blockchains. Naturally, R3’s technology responds to all of these points.

For example, Corda provides an explicit path by which transaction finality can be achieved, through the use of “notary” nodes whose explicit role is to provide an interface with existing legal structures. More generally, Corda makes peace with existing institutional structures in a way that typically breathless crypto claims do not.

A Corda transaction can include an attachment, e.g. a PDF document meant to be read by humans, that could be a legally binding contract and take precedence over the programmed aspects of the transaction, which could, if necessary, be reversed through manual intervention. This is in contrast, for example, to the “move fast and break things” spirit of non-fungible tokens (NFTs), which have enacted new models of tokenized ownership while disregarding existing property rights regimes.

Readers of Soon Parted will appreciate that Corda also makes explicit room for both assets and liabilities. The technical whitepaper includes (Sec. 6.2) a discussion of liabilities and netting that is far more recognizable, from a monetary point of view, than what one might encounter in the world of DeFi. I am reminded of Citi’s Tony McLaughlin’s vision for a regulated liability network, with circulating asset and liability tokens—and it turns out that R3 and Citi saw the connection too.

The future of crypto is in this general direction

Whatever future crypto has will be, in my opinion, within and between regulated institutions (and it will have a different name, or no name at all). R3 has a sophisticated and informed critique of crypto, and its own financially literate technology Corda. From Hearn’s paper and a less technical introduction, by R3’s CTO Richard Gendal Brown, one can see why central bankers and commercial bankers have found it possible to collaborate with them.

To be clear, I do not have a horse in this race, nor would I presume to be able to call the winner. But as stablecoins get absorbed into banks, someone will have to design the new plumbing, and R3 has a more convincing pitch than most.

For the sake of discussion, I think it's worth noting the difficulty in the adoption of products that support Corda and it's underlying architecture. At the heart of this is the difficulty of any legacy institution to adopt solutions that shift the value chain in fundamental ways.

That R3 developed Corda specifically for existing financial instutions and that this adoption difficulty still exists, speaks to the structural challenges facing markets today. I would not have expected Corda to be such a fundamental jump, but it seems to be so. Where this dissconnect is occuring is worth debate, such as if it's in the technical operational demands or if it's in the way Corda reduces emphasis of certain central clearing functions, among a few ideas.

I'm not sure what the answer is, but I think the Innovators Dilemma by Clayton Christensen is the best framework to view this challenge. And to me that means that whatever is happening in the crypto space holds quite a significant advantage if they can figure out how to bridge the gap into real markets.