Three big ideas for tokenized finance

JPM’s multicurrency CBDC experiment

From their late 2021 peak to date, the collapse in prices of crypto assets has shone a light on mismanagement (as at Celsius), broken well-intentioned but flawed concepts (such as algorithmic stablecoin Terra/Luna), and created somewhat odd historical revivals (SBF as JP Morgan). Despite the turmoil, some deep crypto ideas have not yet faced a true political-economic test. The existence of public blockchains, for example: I have argued that they will eventually be enclosed, but for now I don’t see that happening.

At a deeper level, the underlying financial innovations have held up pretty well. Three big ideas emerged alongside crypto assets, and have so far stood up to the challenges. The first is tokenization, the idea that counterparties to a transaction must demonstrate what they have, not who they are. Such bearer instruments are suited for use on distributed ledgers, by which counterparties to and observers of a transaction each reckon the flows individually and then reconcile with one another. This enables programmable contracts and their putative benefits: unattended, pre-committed transactions of arbitrary complexity.

In today’s post, I use this reading of the technology to interpret the writeup of a multicurrency tokenization experiment carried out by Onyx, JPM’s tokenized finance division, with the central banks of France and Singapore. The demonstration took place in July 2021, and the document is dated November 2021, so I caution against taking this as an up-to-date measure of the state of wholesale tokenized finance—much has changed since November. But it takes place at the monetary core, and so is worth a look.

Tokenization

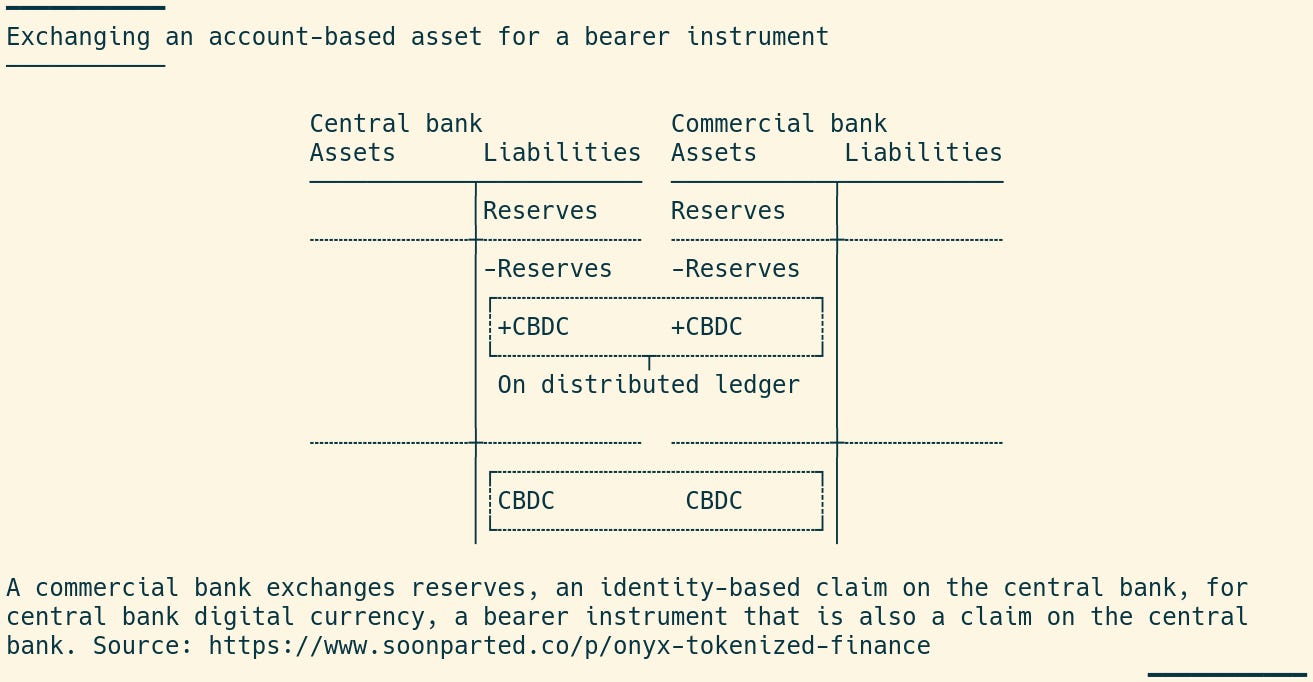

Tokenized assets are just a starting point for this Onyx experiment, so much so that the mechanics do not merit any discussion in the whitepaper. But we can spell it out, as I have done in the T accounts below. I show a commercial bank exchanging an account-based reserve deposit for an equal amount of tokenized central bank digital currency.

The balance-sheet structure of the two forms of money is the same, but the instrument is different. Reserve money is account-based, attached to the identity of a legal counterparty, and not usable on the distributed ledger. CBDC is a tokenized asset, a bearer instrument secured by cryptographic keys, and it exists on the distributed ledger.

Other institutional variations on these arrangements are possible: for example, it might be a private bank and not the central bank that issues the tokenized asset. The essential thing is that someone has to be in a position to take in off-chain money and create on-chain money. The central bank is in a particularly good position to do that, but others could as well.

Distributed ledger

The Onyx mCBDC experiment used a distributed ledger with tokens representing different national monies, much like what the BIS used in its mCBDC Bridge. In this case, the ledger technology comes from Consensys, which offers a version of Ethereum configured for permissioned use.

The Onyx mCBDC whitepaper’s Appendix B, where I spent the most time, gives a step-by-step illustration of the transactions that made up this experiment. At each step, interestingly, it shows which nodes can see the balances of which other nodes.

In a distributed ledger, some transaction information is visible to multiple participants. The design of such a system must take explicit account of who can see what. The whitepaper shows this with a single-entry “wallet” view of the participants’ balances in the system. This does not clearly show the financial meaning of the different tokens, but it does gesture to how we might think about transaction visibility on a distributed ledger. Any trade will be visible to its counterparties, probably to token issuers, and possibly also to supervisory or infrastructural nodes on the ledger. On public ledgers, regular Ethereum for example, transactions are fully visible to the public. There is a political-economic conversation, one that has yet to really happen, about how this might work in a fully developed tokenized financial system.

Why bother with tokenization and distributed ledgers? The Onyx mCBDC project’s value proposition is a familiar one: cross-border payments are complex, slow and expensive. A tokenized system, the theory goes, could offer a solution that is simpler (to end-users at least) and so faster and cheaper. Some of those benefits might come from the distributed ledger itself, which could help simplify correspondent banking chains.

Programmable contracts

The whitepaper is grasping for a bigger prize, though: programmable contracts. Once all of the funds are brought onto a common distributed ledger, they can be used in automated transactions. This particular Onyx mCBDC experiment used an FX market-making mechanism. The idea is to allow currency trades using automated market-making—programmable unattended contracts that can execute without discretionary intervention. They are like options with complex payout conditions.

The outlines of the financial structure are illustrated in the T accounts below. In step (1), the unattended FX pool is funded by a liquidity-providing bank. In the kind of market-making design used in the Onyx experiment, the liquidity provider is obliged to fund both sides of the pool, allowing a two-way market to be made. In this case, the two sides are euros and Singapore dollars. The liquidity-providing bank receives an LP token in return.

The Onyx mCBDC experiment used a constant-product design for the automated market-maker: imbalances in the pool translate automatically into price changes intended to restore balance. Perhaps the Terra/Luna implosion, which took place months after the Onyx demo, will prove to be the end of this line of thinking. The two are similar in spirit, and suffer from the same kind of asymptotic outcomes if the value of one or both of the tokens goes to zero. Still, one could dream up countless variations on automated market-making, some of which may not suffer from the division-by-zero problem faced by the constant-product design.

Mutually unintelligible?

This kind of tokenized financed experiment seems set to continue. The next generation of the technology, I argue, will be built inside regulated institutions.

From the sidelines, it remains fascinating to watch the attempts at conversation: on one side stand the operators of the global monetary system—central bankers, money-center bankers and regulators, whose dialect is that of the money markets. On the other side are the tech upstarts—software developers, cloud providers and fintech entrepreneurs, whose dialect is that of Silicon Valley. Communication between the two has a long way to go.

Hi, I'm James.

I am a crypto writer based in Taiwan. I found this topic is fascinating and enlightening for our readers.

May I translate and reprint the article and will be citing the source?