Stablecoins are banks

As Tether is demonstrating

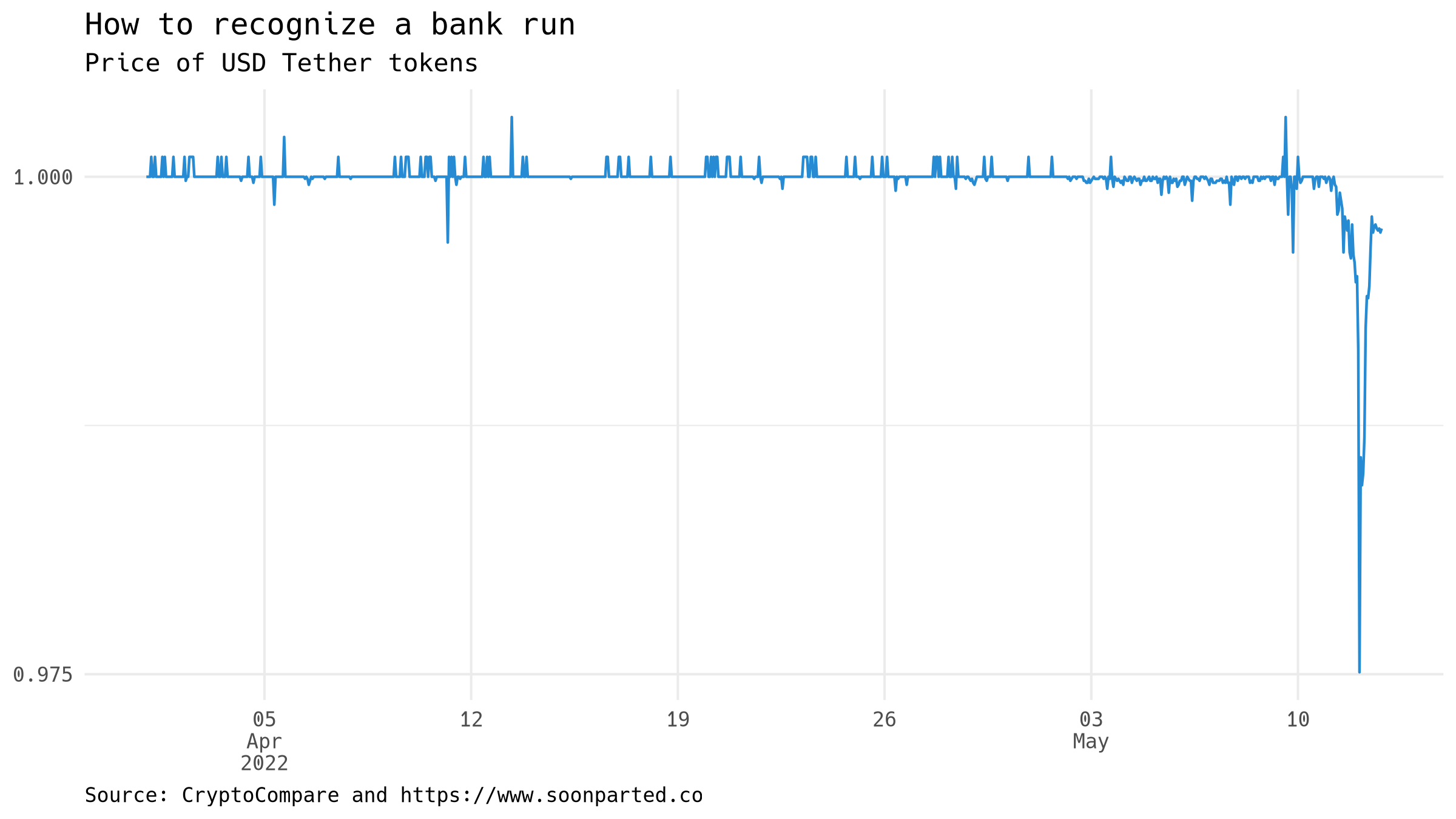

In recent days, stablecoins issued by Tether, Inc. have been caught up in a flight to cash across many markets. The company is the most prominent among issuers of moneylike assets on public distributed ledgers, which have come to serve an infrastructural role in crypto finance transactions. Tether manages its tokens so as to keeps their price fixed at one dollar. That has proven difficult:

It seems like the perfect opportunity to remember that Tether is a bank, and that all banks are always at risk of a run.

Tether is a bank

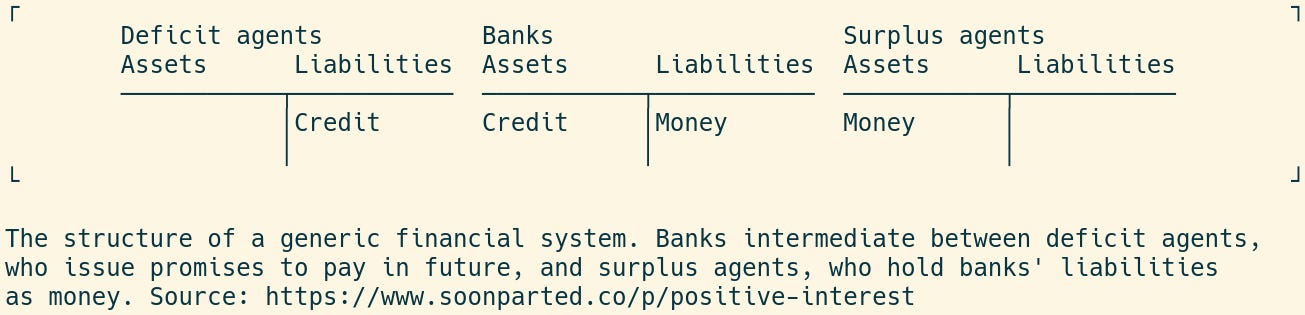

The most basic banking activity is to intermediate between two groups of customers. One group faces a payment deficit, a need for cash, and so must borrow. The other group enjoys a payment surplus, cash in hand but not needed today. Between these two groups steps a bank, buying credit issued by the deficit agents and selling money to the surplus agents. A given bank will make its business by developing relationships with some particular set of deficit agents and some particular set of surplus agents.

Deficit agents thereby become able to pay their bills, surplus agents can enjoy the benefits of money unspent, and the bank collects interest or fees as compensation for its efforts. The creation of money and credit leaves in its wake a set of financial relationships, which can be written using T accounts like this:

Tether is a bank: it buys credit instruments and sells moneylike stablecoins. On the asset side of its balance sheet, it holds a portfolio consisting mostly of US Treasury securities and commercial paper. This is just like a money market mutual fund, another bank-like entity. The liability side is more innovative, consisting of tokenized moneylike claims trading on public distributed ledgers, mostly the Ethereum and Tron blockchains. I say that Tether’s stablecoins are moneylike, because they are meant to be fixed in price at one, and because they are meant to be redeemable on demand.

(Note that this version of the balance sheet is schematic and based on the limited information the company puts out.)

All banks face the possibility of a run

The basic problem created by arrangements like these is that any bank depends on the forebearance of those who hold the money it has issued. The bank pays its liabilities using the proceeds of its asset portfolio. These payments come in only over time, and cannot necessarily be collected early. If holders of the bank’s moneylike liabilities want their funds all at once, as they are entitled to do, the bank may struggle to meet their demands. If the flow of redemptions becomes large, the bank may need to sell assets out of its portfolio in order to keep up.

Every once in a while, some particular bank’s liability holders find they have to form a queue while they wait to get paid. This has happened enough times in the history of finance that it has a name: a bank run.

There have been banks and bank runs for centuries, but enough of the details change from decade to decade that periodic updating is required. An important example of institutional change has been the shift from bank-based credit to market-based credit. In a bank-based system, credit appears in the form of non-marketable loans, while money shows up in the form of bank deposits. In a market-based system, credit and money both come in the form of marketable securities.

Such institutional differences may matter, when push comes to shove, because they determine the order in which people get paid. 2008 was a crisis of the market-based credit system, and so the run on that system looked like a rush to sell securities. The result was intense pressure on the securities dealers that had to absorb a one-sided flow. Different institutional arrangements meant that the Panic of 1907 looked like depositors lining up in the streets.

This time is the same

Tether offers new institutional variation on the generic banking theme. The chief innovation is the company’s assertion that it is not subject to the regulations that govern banks or money market funds, on which basis it provides only minimal details about its assets. Another distinction is the functionality that stablecoins offer in programmable and unattended financial arrangements. This makes Tether an artery between off-chain and on-chain money, and so locates it squarely along the escape route from the wider crypto downturn.

Tether may well survive this bout. Still, the many technical innovations that arrived with cryptocurrencies have done nothing to change the logic of banking. That logic means that the risk of a run is always present, and sooner or later the real meaning of decentralized finance will become clear.

I would say a key distinction between banks and other issuers of short-term debt is that when banks issue deposit liabilities they buy a newly created credit instrument, when tether does so (buying a us treasury for example) its buying an asset already in circulation. Another would be that I assume non-banks settle most of their transactions with bank deposits, whereas banks settle their transactions with reserves, which would entail a hierarchal relationship not an equal one. Maybe the hierarchy has flattened with the numerous fed facilities. In any case, I could be just nitpicking here, but I’ve heard this line of thinking before (not just with stablecoins but with all non-bank FIs) and wanted to get your opinion. Are you using the word ‘bank’ just to describe issuers of short term liabilities where those liabilities are expected to maintain a stable value?

One larger difference between stablecoin liabilities and those issued by banks (deposits) and mmfs ($1 shares) is that stablecoin issuers also have the ability to defend their peg in the secondary market with their own liquidity resources. This seems to me a new function of this system and something a) not widely discussed, but also b) has many more unknowns as to how the stablecoin issuer will use it’s liquidity resources - is that to defend the secondary market price or will it be to satisfy redemptions. What is the interaction between one of these mechanisms on the other?

What are other thoughts on this? Are there other analogs that I may not be thinking of?