Automated liquidity for FX?

It still depends on funding

This post is informed by discussion with Larissa De Lima, Raphaele Chappe and Sébastien Derivaux. I am solely responsible for the views represented here.

These days, it is the regulators who are deciding the course of decentralized finance, a big change from the heady days of 2020 and 2021. Those DeFi institutions that have survived are re-working their pitches for a tougher political-economic climate. A new white paper from Uniswap and Circle, two big names in decentralized finance, makes a case for one of DeFi’s most interesting ideas, automated market-making, as applied to foreign exchange markets.

If we had to boil the paper’s claim down to a single sentence, I would write it like this: Under current arrangements, cross-currency payments must pass through a system that is complex, expensive and risky; automated market-makers (AMMs) would allow a system that is simpler, cheaper and more secure. Until that thesis is resolved, AMMs seem likely to be the focus of continued investigation.

Like most arguments for automated market-making, the paper focuses on a small set of convincing benefits: 24/7 availability, fast settlement, and low fees. In this post, I suggest one big addition to the paper’s perspective, which could help clarify the risks of a more systemic role for automated-market making.

How it works

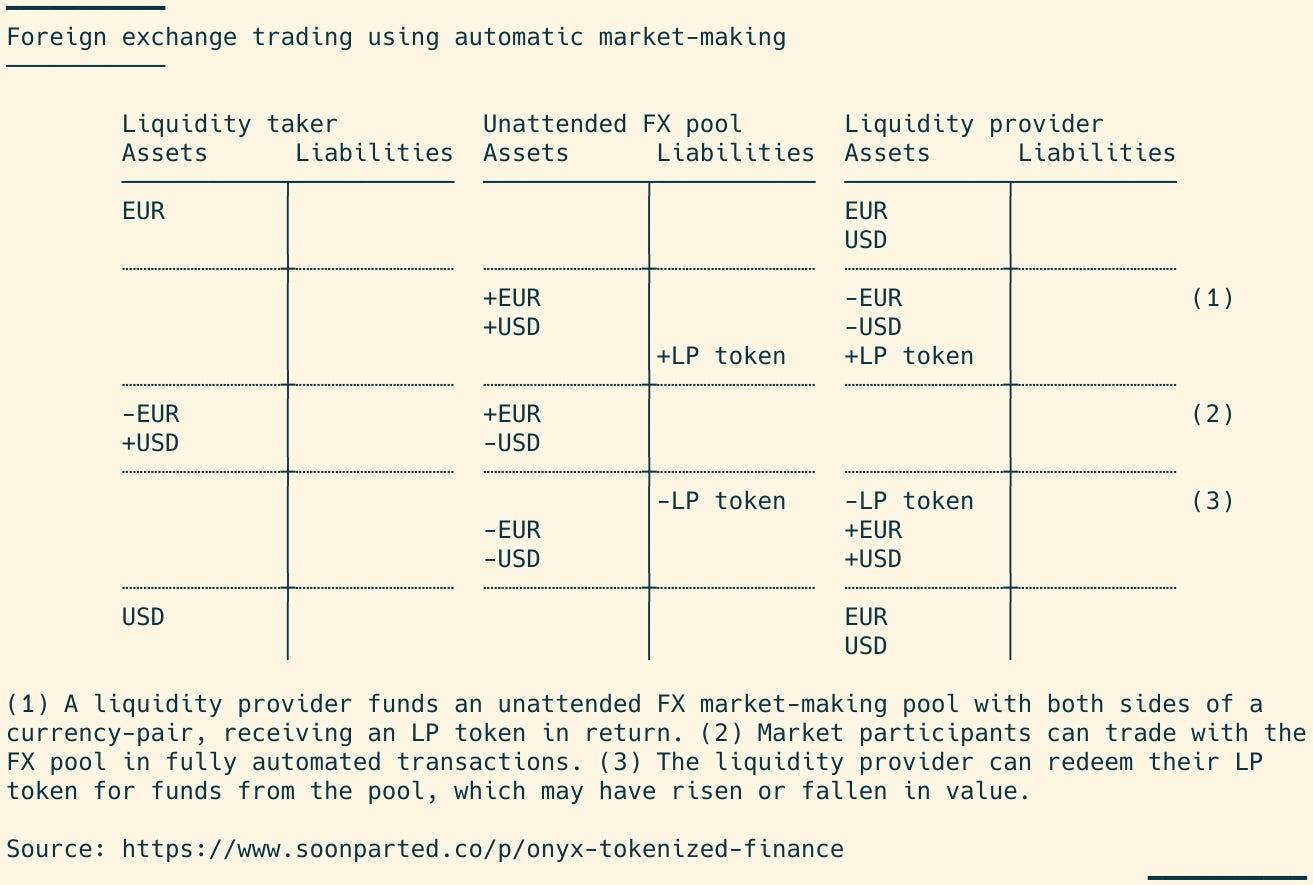

What is automated market-making? We can paint a fair picture by starting from a regular ATM, which is an unattended, automatic system for making bank deposits and withdrawals. AMMs, such as Uniswap, are similarly automatic and unattended, while adding two other characteristics. First, rather than facilitating banking transactions, they facilitate exchange, at a varying price, between two assets—dollars and euros, say. And second, AMMs are entirely immaterial: they exist only as software operating on digital distributed ledgers.

The T accounts below illustrate the mechanics of an automated market making contract for foreign exchange. Imagine a holder of euros who wants to sell them to buy dollars. AMMs hold reserves of two assets, and make two-way prices between them. They are funded by the deposits of speculators who act as liquidity providers. At any time, a liquidity provider may deposit quantities of both assets into the pool, receiving a single deposit token in return (1). The ratio in which the assets can be deposited (i.e., the price) fluctuates according to the AMM’s algorithm.

Once the FX pool is funded, other users can use it to make foreign exchange transactions (2). Later, the liquidity provider can withdraw their funds, redeeming their LP deposit token for quantities of the two underlying assets, in a proportion that may have changed since the LP token’s issuance (3).

Follow the funding

Funding an automated market-maker is therefore itself a speculative investment. The liquidity provider buys an LP token and sells it later, and can make either a profit or loss on this speculation.

This dimension of AMMs receives no attention from the Uniswap paper, but if we are to imagine AMMs at a more systemic scale, it cannot be ignored. The liquidity provider also takes foreign exchange risk. Big funders will necessarily have to think about that risk, and trade accordingly. Uniswap and other AMMs have, up to now, operated at a small enough scale that this fact can be ignored. But to imagine a systemic role for AMMs, operating at greater scale and closer to the center of global finance, the question of who owns the LP tokens, and when they might try to liquidate them, becomes inescapable.