Dear dollar

The strange pretense of a flat system

There is an odd, and mistaken, conviction at the center of the global monetary system: the US Federal Reserve makes monetary policy as though the matter is primarily a domestic concern, when in fact dollar financial conditions affect the entire global system.

The global dollar is notably absent, for example, from the minutes from the September FOMC meeting. International considerations enter only in a peripheral way: “other central banks lifted policy rates and indicated … that they would likely continue to tighten.” The dollar is mentioned in a handful of places, compared to extensive discussions of US productive activity. This makes it sound like the Fed makes US monetary policy, and other central banks are invited to do the same, as though each central bank were free to act independently. Call this the pretense of a flat system.

To the contrary, recent hiccups in the UK, Japan and Korea make particularly clear that, in fact, dollar monetary policy sets strong limits on what other central banks can do. In this post, I try to sketch out a way of thinking about global monetary policy.

Flying in formation

This graph shows short-term policy interest rates for the dollar and four other major currency areas. These are the target rates set by monetary policymakers at each currency area’s central bank. The details differ from place to place, but all are short-term rates in highly liquid money markets, and so are comparable.

The current period of rising interest rates began in late 2021, and all of these central banks bar the Bank of Japan have been hiking since then. The gray vertical lines mark dates on which the Fed changed US policy rates (rate cuts in early 2020, increases more recently). Importantly, the Fed has hiked more than the other central banks. The Bank of Korea and the Bank of England are within a point of the Fed; the ECB is a full point lower. The BoJ, uniquely, is enjoying the respite from decades of deflationary conditions, and has so far held fast with negative rates.

The flat-system perspective would insist that each of these central banks is responding to inflation. Inflation is high everywhere, so everyone hikes, except Japan which is still trying to get more inflation, and these actions are independent of one another.

But the system isn’t flat

This is indeed the sense one gets from the FOMC minutes. But if we note that actually the system is not flat, but rather is dominated by the Fed and its dollar, we can give a more informative interpretation of these policy rates. The graph below shows each rate as a spread against fed funds. For these four currencies, rates are below dollar rates, and so the spreads are negative:

Simply put, a negative spread means that overnight funds earn a higher rate if they are held in dollars than if they are held in another currency. As the Fed has gotten further out in front of other central banks—as policy rate spreads have widened—those who are able to have been buying dollars and selling everything else.

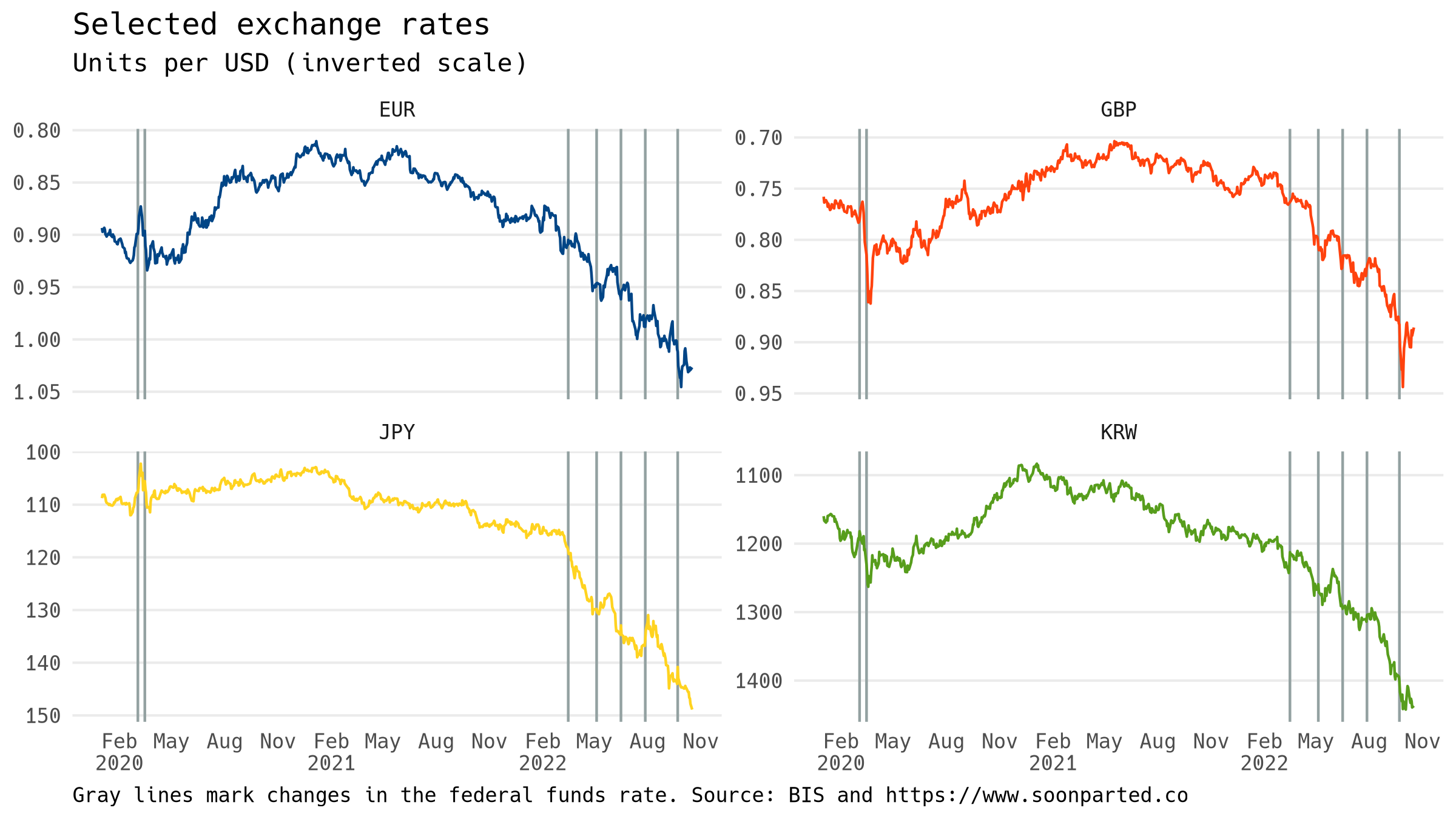

This pushes up the price of the dollar in foreign exchange markets, or equivalently it pushes down the dollar price of other currencies. This graph shows the exchange rate over the same time period for the same four currencies, and with changes in US interest rates marked in the same way. Vertical scales are inverted to correctly convey the falling value of each of these currencies:

In broad strokes, the pattern is the same across the four different currencies—a big drop from March 2022 forward. It’s hard to explain the synchronization in a flat system. In a hierarchical system with a dominant dollar, it is simply a matter of rising rates.

Conclusion

The September FOMC meeting’s main message, by my reading, is that US production had not by then shown much response to tightening financial conditions, and so higher rates and balance-sheet contraction are set to continue. Exchange rates get less space in the minutes—the dollar is appreciating because of economic weakness elsewhere, and rate spreads are a decidely secondary concern.

Using the global dollar view, we could say instead that widening spreads have made it more costly to meet dollar payment commitments. So far, US economic activity has held on, and instead we have gotten increasingly fragile financial conditions globally.

The likelihood is increasing, that is, that an international liquidity crisis will emerge before the Fed succeeds at stamping out price growth. The more we cling to the pretense that the system is flat, the more likely that becomes.