Leaky floor

Monetary policy is pushing upward, for now

The federal funds rate has been more or less zero for nine of the thirteen years that have elapsed since 2008. During that time, we have grown accustomed to thinking about US monetary policy mostly in terms of balance sheet quantities. But with interest rates now in positive territory, we are obliged to think about rates and quantities together.

Not just a single interest rate

Interest rate policy is often discussed, including by the Federal Reserve itself, in terms of a single rate, the federal funds rate. But it is more helpful to think about a complex of different overnight interest rates.

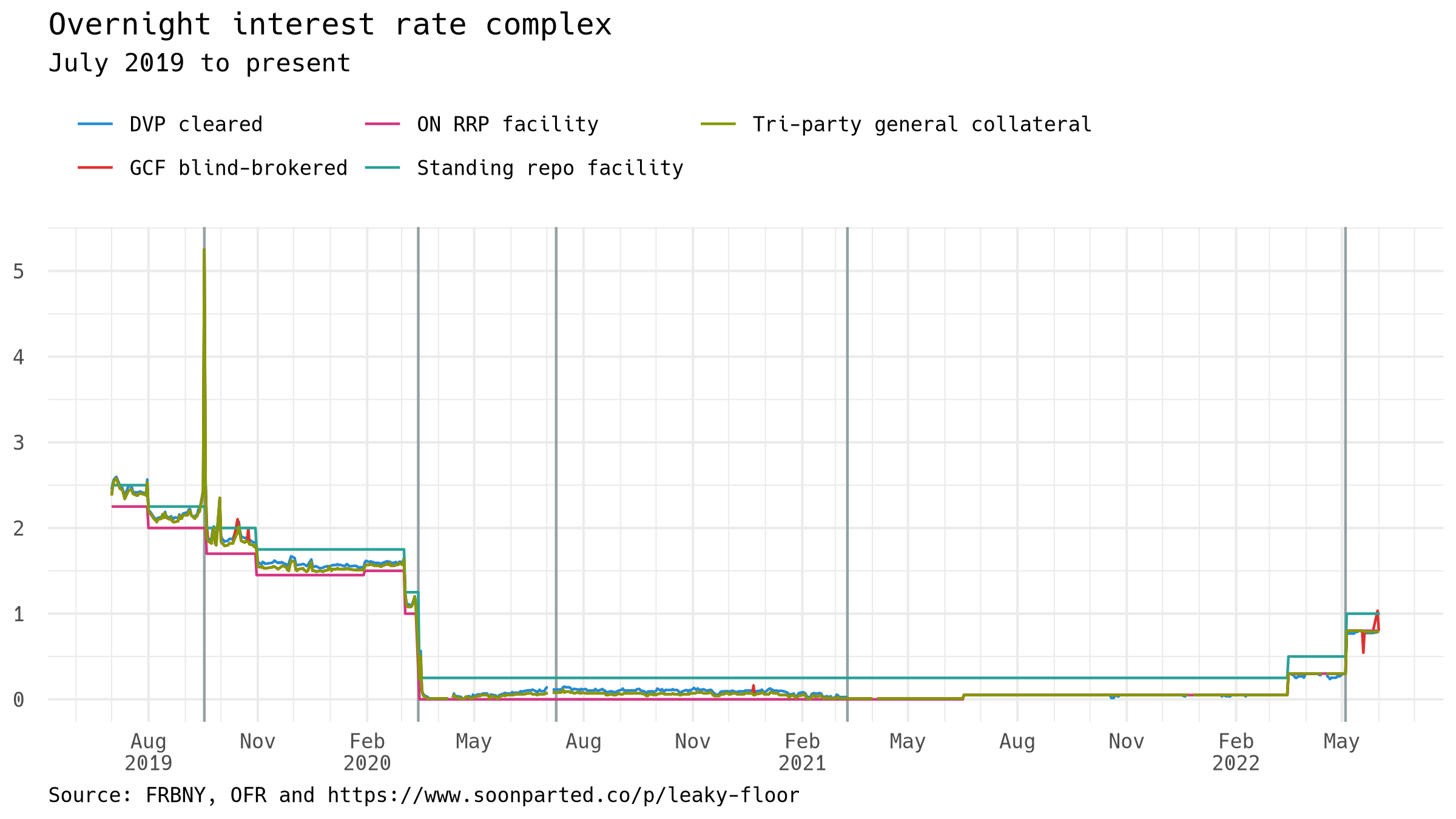

Key rates from the secured overnight funding complex, from mid-2019 to the present, are shown below. The timeline of macrofinancial events comes through clearly. The September 2019 repo crisis was marked by volatility and big spikes in repo rates. Six months later, COVID-19 emerged and rates were promptly brought down to zero. In March of this year, the current cycle of rate hikes began:

(The vertical lines are based on the periodization I use for thinking about the Fed’s balance sheet, see for example this post.)

Each of the various rates corresponds to a significant wholesale secured funding channel. They all tend to move together, so it makes sense to speak of a “complex.” Although there are different prices for overnight funds, these prices are not independent. That is true both in moments of volatility, as in late 2019 when repo rates spiked, and in moments of quiescence, as in the last year or so.

Policy rates and market rates

So much for broad strokes. We can look not only at the outlines of the overnight rate complex, but also at its internal structure. Importantly, the arrangement of rates within the complex is both stable enough to have some meaning, and variable enough to be informative.

In the graph above, it is easy to see that there are market rates, set by profit-motivated market-makers, and which fluctuate from day to day; and that there are policy rates, set by the central bank, and which change only at policy meetings. The market rates are mostly contained by two policy rates, one above and one below.

The various prices of overnight money, that is, are usually cheaper than the interest rate charged by the Fed at the standing repo facility (SRF), which acts as a ceiling to the other rates. The various prices of overnight money are usually dearer than the rate paid by the Fed at the overnight reverse repo facility (ON RRP), which acts as a floor.

The graph below shows the same rates as above, measured now as spreads over the ON RRP rate, or in other words measured upward from the floor:

ON RRP is a leaky floor

ON RRP is a standing deposit facility which pays interest to the money market mutual funds that place funds with it. The ON RRP rate, currently 80 bp, acts as a floor to overnight interest rates: it is effectively unlimited, so those with funds to place can always be sure of receiving that rate, rather than accepting a lower rate elsewhere. ON RRP is intended to serve this purpose: the Fed sets the rate near the bottom of the target range for the fed funds rate, as a way to keep rates from going too low.

But as the graph shows, the floor is leaky: other rates do occasionally pass below it, into the basement as it were. These events have been isolated, so far, with the various rates each dipping below the floor for a few days at a time.

Isolated, but not random: it is easy to see that the floor leaks because of a strong downward tendency in overnight rates. The floor is pushing back, albeit imperfectly. Monetary policy is currently pushing rates up from below. But as the Fed’s balance-sheet contraction plans get underway, conditions in overnight funding markets could change quickly, and the secured rate complex could come up off the floor. Stay tuned.