From leaks to flood

What’s going on with overnight rates?

Monetary tightening comes in two forms—either central bankers can let rising rates go, or they can push up against falling rates. These days, tightening is of the second type: the Fed is raising the floor, which by the beginning of June had started to leak.

These leaks—overnight rates printing below ON RRP—grew during June, but rather frustratingly, I can’t come up with a clear story for why. In this post, I try to put the facts in order in the hopes that readers will point me to the explanation.

Short-term rates

Since March, the Fed has added 150 basis points to its targets for overnight interest rates. Formally, the central bank sets policy using the federal funds rate. But the various overnight lending markets are close substitutes and are usually quite liquid, and so are connected by tight arbitrage relationships. Prices for overnight money usually stay quite close together. As a result, monetary policy typically moves the entire overnight rate complex as a unit.

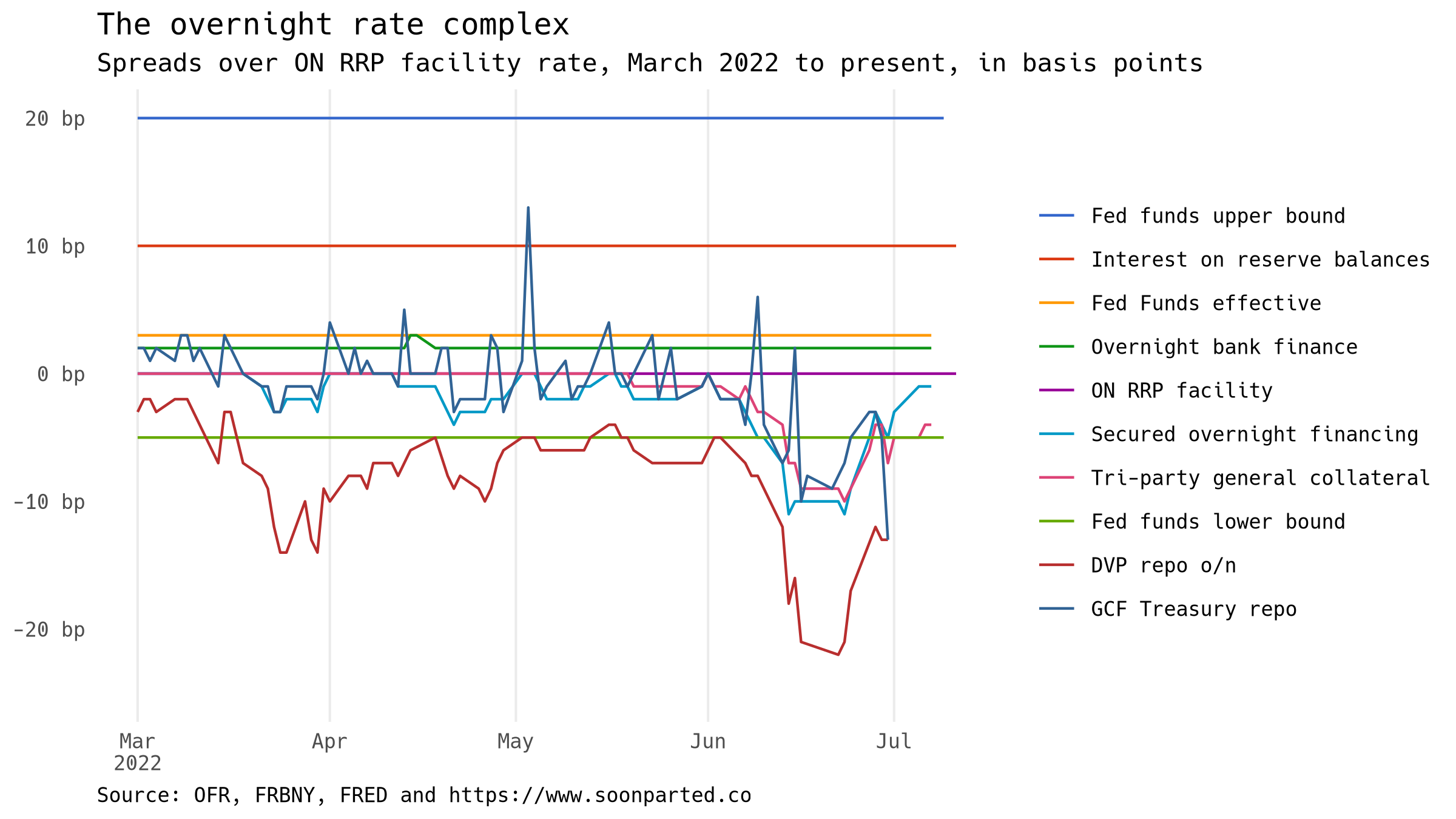

This graph shows the key overnight US dollar interest rates. From March 2021 until March 2022, the overnight reverse repo (ON RRP) deposit facility provided a fairly effective floor to money markets. Intuitively, depositors should not accept less interest than the ON RRP rate, because they always have the option of depositing with the Fed. The ON RRP is open only to money market mutual funds, but because it is unlimited in size, it should still be able to soak up extra funds in other places, perhaps indirectly. In the graph, I have expressed each rate as a spread relative to the rate paid by the Fed at the ON RRP facility.

The graph is a little busy, showing ten different overnight rates, but I think it’s worth it for the satisfyingly high information density. Note that the rates are not fully independent of one another. ON RRP transactions, for example, are conducted in the tri-party repo market, and so form part of the basis for the measurement of the tri-party general collateral rate (TGCR). This in turn is a subset of transactions counted in the secured overnight financing rate (SOFR), as are the DVP and GCF cleared repo services.

Worsening leaks

One might be forgiven for concluding that the central bank does not have a perfect grip on short rates at the moment. As the graph shows, the overnight rate complex has not held together very well since March—around the time the fed funds target was raised above zero. All of the key secured financing rates have recently been printing below ON RRP, and even below the bottom of the target range for the federal funds rate. This graph zooms in on this recent period:

Roughly speaking, we can think of overnight repo in four segments: 1) ON RRP with the Fed, 2) other tri-party repo, 3) GCF blind-brokered, and 4) DVP cleared repo. The graph says that the ON RRP facility rate, far from providing a floor, is currently the highest of the repo rates. Even though the Fed is paying top dollar for repo deposits, in other words, it has not succeeded in driving the price up.

More questions than answers

How should we interpret this? Literally, it means that there are plenty of people with cash who are accepting less than what the Fed pays for money market funds. This should create a riskless arbitrage for someone: borrow in the repo market and deposit with the Fed for a profit of more than 5bp since March, and over 20bp in late-June. For a bank, with access to the IORB rate, the gap is 30bp. The exploitation of that arbitrage would cause it to close.

I have been talking about rates, but this is not a separate story from the balance-sheet positions involved. On this, see this recent piece in Alphaville by Meyrick Chapman, who suggests banks are shifting from holding securities to holding loans and connects this to the low secured funding rates. Chapman interprets the low rates as indicating high liquidity, so that an unexpected spike is unlikely. But I wonder whether this situation is as stable as that. Could it reverse quickly as the Fed’s balance-sheet contraction gets underway?

Jeff Snider would argue a premium is being paid for scarce collateral and UST’s etc are simply balance sheet tools these days. I recommend Jeff’s work as he looks at money matters more from the collateral side rather than the cash side. His writing can explain far better than I can. See Old work at Alhambra Investments. Now at Macro Plus Insider and has written for years at Real Clear markets. Thanks again Daniel for your work.

Very nice post, Daniel. I’ve been looking into this too, and have a few thoughts:

- The market participants who could possibly benefit from the arbitrage are probably balance-sheet constrained (banks and dealers). We can see this by banks shedding deposits to MMFs and dealers’ constraint via (deteriorating) market liquidity.

- With this, the rate “gap” between funding markets and ON RRP take longer to close following a hike. Can see this in 1-month bill/ON RRP spread which the past three hikes have taken roughly 20 days to recover; MMFs (and other cash investors) rebalance their portfolio from Bills to ON RRP over this time. This is the main mechanism right now w/ bloated balance sheets per above.

- Participants without Fed access (asset managers, pensions), are a bit more agnostic between bills and MMFs given the fees/expenses of MMFs, but I think the recent growth of ON RRP speak to more rotation out of bills and into MMFs as well (which then deposit in ON RRP).

Still thinking through impacts of QT...more to come...