Closed circuit

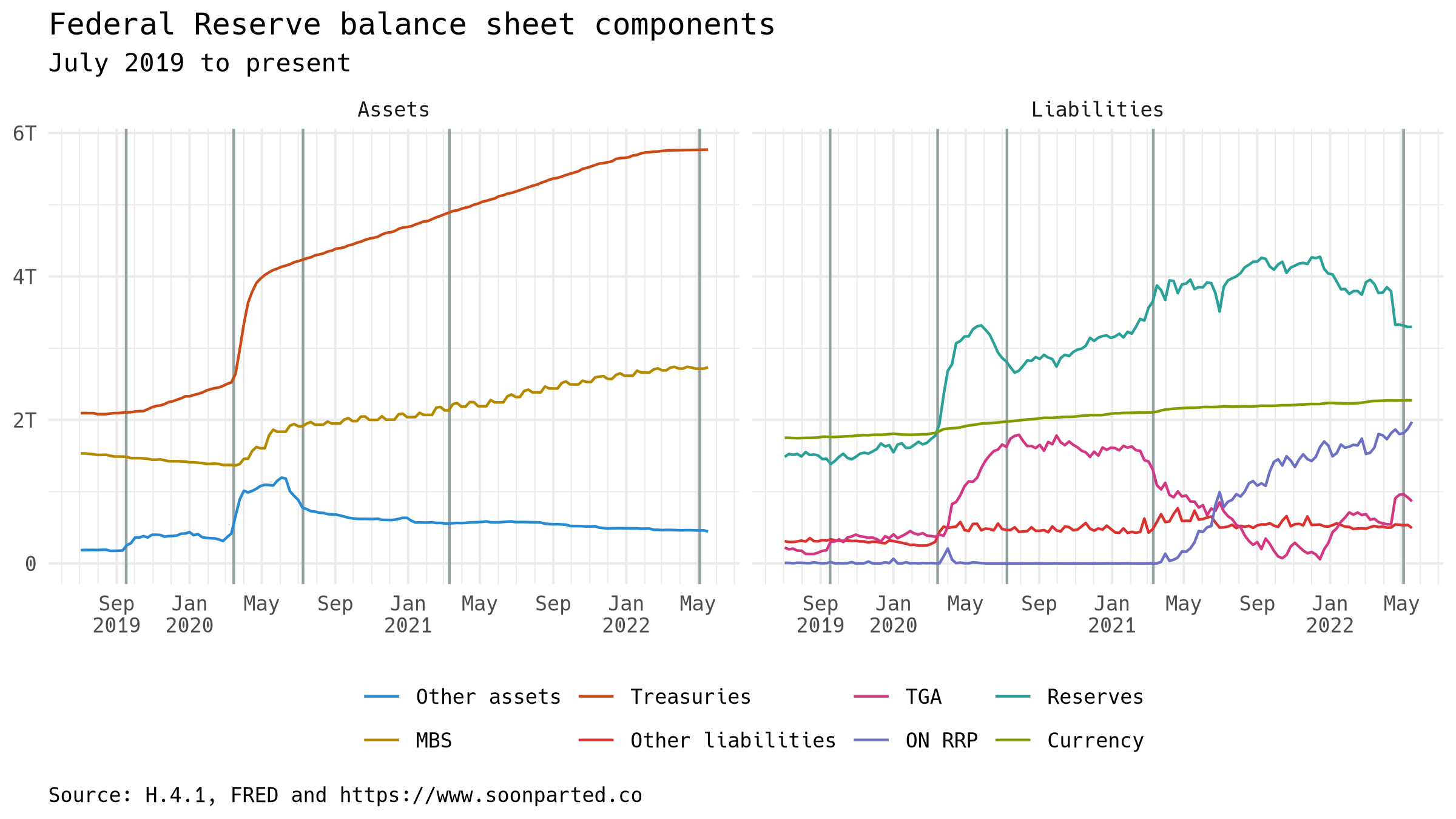

The overnight reverse repo facility reaches $2 trillion

Repo deposits at the Fed’s overnight reverse repo (ON RRP) facility surpassed $2 trillion this week for the first time. The $2 trillion threshold is symbolic, a reminder that in 2020 and 2021, the Fed’s asset purchases got big enough to require a whole new liability to pay for them. What is more, the milestone comes at a pivotal time in the path of the Fed’s balance sheet, after expansion has tapered and ended, but before contraction begins next month.

Coverage in the financial press of the ON RRP facility, even from my favorite sources, falls into a common misinterpretation. In this post, I try to correct the monetary fallacy of “no better alternative investment.”

A reduction in ON RRP would mean an increase in bank reserves

The US Federal Reserve’s overnight reverse repo facility accepts deposits from US money market mutual funds (money funds or MMMFs). First tested between 2013 and 2019, ON RRP was scaled up rapidly starting in March 2021, as the central bank needed a way to pay for its program of securities purchases. Now a $2 trillion liability entry on the Fed’s balance sheet, ON RRP is comparable in scale to the reserves of the banking system, at $3.3 trillion, and currency issuance, at $2.3 trillion.

The Fed pays interest on ON RRP deposits, currently 0.8 percent (80 basis points). The rate is set at 5 basis points above the bottom of the target range for the federal funds rate, and 10 bp below the rate the Fed pays to banks on reserve balances (IORB). The ON RRP rate functions as a floor to the overnight rate complex: since money market funds can deposit funds at the facility whenever they want, receiving interest at the ON RRP rate, there is no reason for them to accept a lower rate elsewhere. The floor has been effective, the exceptions being interesting but few.

So far so good, but here comes a possible misinterpretation. Yes ON RRP deposits are above $2 trillion, and yes ON RRP sets a floor on rates, but it is wrong to draw the conclusion that money funds are using the ON RRP facility because there are no better alternative investments.

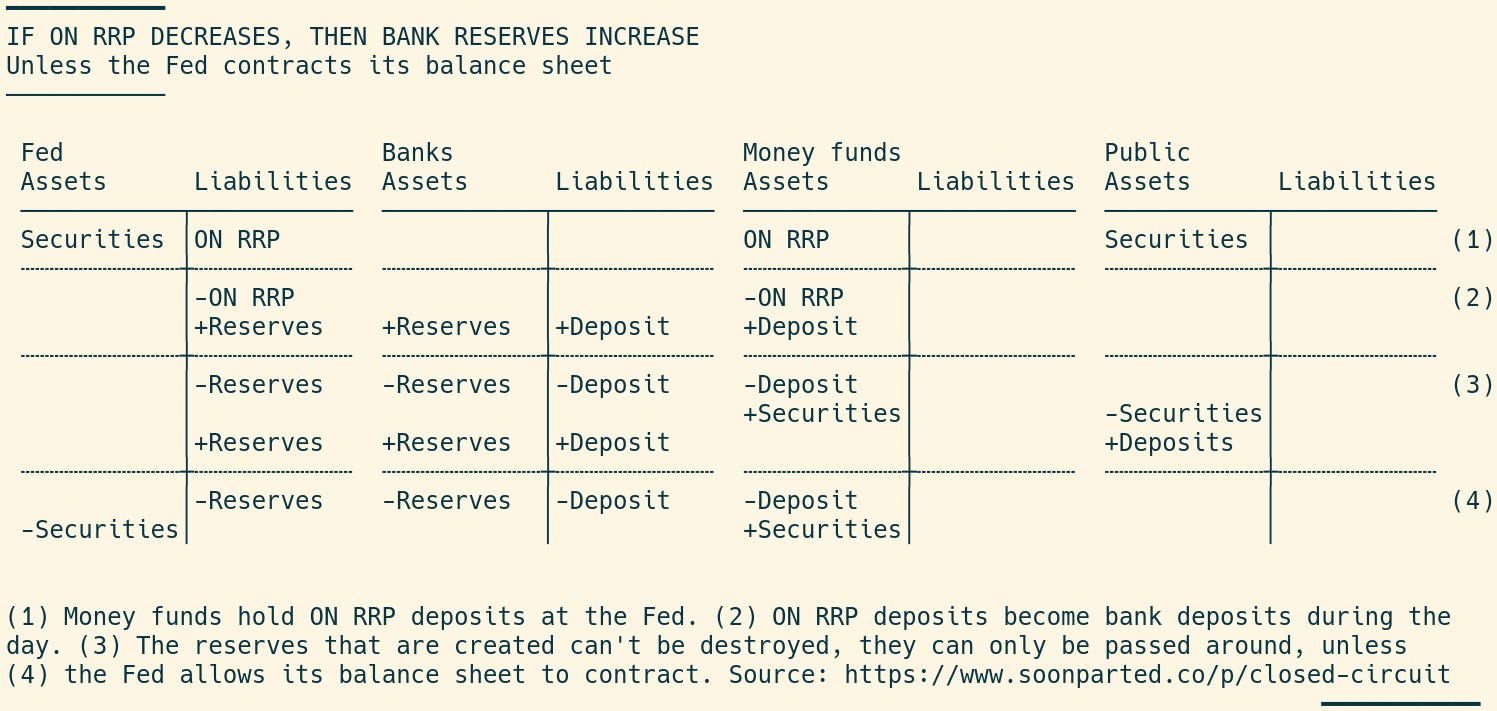

Suppose, to the contrary, that there were better alternative investments for money funds. The T accounts below illustrate. At the outset (1), money funds hold overnight repo deposits at the Fed and the public holds securities paying more than 80 bp. Each morning, ON RRP deposits mature and become bank deposits (2). Normally, money funds would roll them back over into the ON RRP facility at the end of the day, but instead suppose that they want to buy the higher-yielding securities.

They can do so (3), but the purchase transfers bank deposits to the seller, so banks end up with that amount in reserves, and the Fed with the same amount of reserve liabilities. There are many variations on this transaction, and if you want to see all of them, you will have to write out your own T accounts. If you do so, you will find the following: money can move between the Fed’s liabilities—ON RRP, reserves, the Treasury General Account, currency—but it cannot be destroyed unless (4) the Fed reduces its asset holdings. This contraction will begin soon, but it has not begun yet.

A different interpretation

So if it were the lack of better alternatives that was stopping money funds from reducing ON RRP balances, we should see steady balances of bank reserves, or even increasing balances if banks faced the same problem.

In fact, banks are reducing reserve balances, while money fund ON RRP balances are expanding. Reserves pay 90 bp, ON RRP pays 80: money is moving from the higher- to the lower-interest investment. Conclusion: banks are reducing reserve balances because they want to, for a reason other than interest rates.

ON RRP, meanwhile, sets a floor under interest rates: it is literally the worst asset money funds can buy. Yet ON RRP deposits are increasing to record levels. Conclusion: money funds don’t have control over ON RRP balances.

Banks are contracting reserves because they can, money funds are expanding overnight repo because they have to.

Hmm. I'm getting stuck. I still don't understand why "it is wrong to draw the conclusion that money funds are using the ON RRP facility because there are no better alternative investments."

Where am I going wrong?

If there *were* better alternative investments for money funds, then we'd see:

1. Money funds holding less RRP and more securities.

2. The public holding fewer securities and more deposits.

3. Banks holding more reserves.

Is that correct?

And if there *weren't* better alternative investments for money funds, we'd see:

1. Money funds holding more RRP and fewer securities.

2. The public holding more securities and fewer deposits.

3. Banks holding fewer reserves.

"So if it were the lack of better alternatives that was stopping money funds from reducing ON RRP balances, we should see steady balances of bank reserves, or even increasing balances if banks faced the same problem."

Why would the lack of better alternatives cause steady or increasing reserves?

"In fact, banks are reducing reserve balances, while money fund ON RRP balances are expanding."

I don't understand why this isn't exactly what you'd expect if money funds were using ON RRP because there were no better alternative investments.

"Reserves pay 90 bp, ON RRP pays 80: money is moving from the higher- to the lower-interest investment."

Right, but money has to move in this direction the public is pulling out its deposits from the banking sector to buy securities from the money funds. Right?

"Conclusion: banks are reducing reserve balances because they want to, for a reason other than interest rates."

They're not reducing their reserve balances because ON RRP is causing a reserve drain out of the banking system as a whole?

"ON RRP, meanwhile, sets a floor under interest rates: it is literally the worst asset money funds can buy. Yet ON RRP deposits are increasing to record levels. Conclusion: money funds don’t have control over ON RRP balances."

If money funds had better investments, what prevents them from moving out of RRP?

"Banks are contracting reserves because they can, money funds are expanding overnight repo because they have to."

I'm not convinced. But like I said, I might be missing something.

This is very interesting. Why would banks willingly reduce reserves? As reserves attract penalty from SLR, I assume banks have more profitable uses for their balance sheet.