The government sector

Macroeconomics note 3

This is the third in a series of notes for a semester-long macroeconomics course. The first note is here. The point of the course is to create a practical and open-ended introduction to macro, with a coherent role for money and without reproducing IS–LM.

An important debate in the history of macroeconomics tries to resolve this important question: “In a market economy, can a government redirect spending using taxes and borrowing, so as to increase total incomes?” This question was of central importance in the global depression of 1929-1933: around the world, total spending, and so also household incomes, dropped sharply. The consequence was high unemployment and so decreased access to the means of human subsistence.

Some economists argued that it might be that, using the centralized spending power of a government, it would be possible to change the patterns of spending, increasing incomes and improving people’s lives. In other words, it might be possible using centralized economic decision-making to improve upon the results of decentralized market-driven decisions. This argument is strongly associated with the name of John Maynard Keynes, an English economist whose work during and after the Great Depression helped create macroeconomics, and changed the way that we think about recessions and depressions. We should be clear that this question is inherently political-economic. By changing how decisions are made about resource allocation, necessarily some people will end up with more resources and others will end up with less. The politics are important, but let’s first try to model the spending flows.

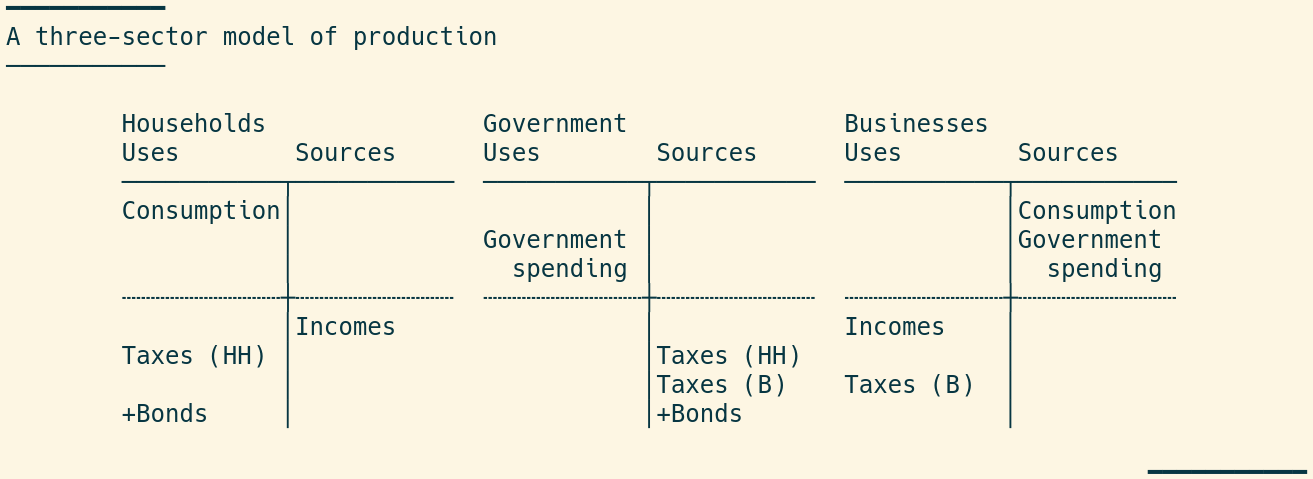

The main theoretical task is to fit a government sector into our picture of macroeconomic flows. In both the two-sector model of production and in the supply-chain model, we had only households and businesses, with no explicit place for production. But in most places today, governments control a significant fraction of economic flows, and they decide how to direct those flows in substantially different ways than either households or businesses. So the added complexity of an additional sector seems like a fair price to pay for capturing the important macroeconomic impact of government.

This three-sector model is a step in that direction. Previously we had used the label “product” to refer to businesses’ source of funds; now we divide that into two categories, household consumption and government spending. In macroeconomic equations, these are usually written as C and G respectively. Both are flows, monetary values associated with a duration in time, as are all the entries in this model. In words, we still have a single sector in which all production takes place, “business.” This business sector sells its output to households as before, but now also to government. You can think of a government contracting with a private business to build a road or an airport.

In simpler models, we defined gross domestic product as the total of all production flows that are sources of funds to business. That is still the case, but now there are two components to that production. So GDP in this model is consumption plus government spending, Y = C + G.

This model also includes a schematic version of government finance. The government sector has sources of funds of two kinds, taxation and bond issuance. Taxes are income flows, legitimated through the legal system and collected from households and businesses under threat of punishment. Tax is a one-time flow, an expense to households and businesses that is gone once the tax has been paid. Governments can also fund themselves by issuing bonds, which is a way of borrowing money. Bonds are different from taxes, because they entail a future flow in the opposite direction, when the bonds are repaid. Repayment is not shown in our T accounts—for now we are thinking only about new borrowing. Note that I write a plus sign, “+Bonds,” which indicates that a stock of outstanding bonds continues to exist after this period is done, unlike taxes, incomes, consumption or government spending.

We can use this model to consider a couple of scenarios. Suppose that the economic policymakers in a government observe that household incomes are low, so that people’s access to material necessities and comforts is limited. Such a government might choose to increase government spending as a stimulus measure. Increasing government spending adds to businesses’ sources of funds, so increasing also the incomes paid to households.

But to keep our model in balance, increased spending by government must be paid for. If it does so by increasing taxes on business, then you can see that the increased tax burden will completely absorb the new spending flows, and household incomes won’t rise at all. If government pays for the increased spending by increasing taxes on households, then incomes will rise, but the entire increase will be absorbed by the higher taxes. Or if government pays for the increased spending by issuing new bonds, then it will need to sell those bonds, again absorbing any increased income to households.

But this doesn’t mean that stimulus spending can’t increase incomes. In fact, there are a couple of ways that government can increase total incomes. We can see one of them in the model we have so far. If government can use its spending power to convince households that incomes are improving, then households might themselves choose to spend more. How do they afford the increased spending? Interestingly, consumption spending is a source of funds to businesses, who therefore pay out more incomes to households: the increased spending pays for itself.