Age of contraction

The Fed’s balance sheet at the end of 2022

Between the collapse of FTX and anticipation of next week’s continued dollar rate hike, there has been plenty for market-watchers to fuss over. Meanwhile, and so far uneventfully, the Fed has been moving ahead with balance-sheet contraction. In this post, I check in on the Fed’s balance sheet and the process of QT.

First, a word on why this is worth doing

Central banks, and especially the Federal Reserve, get attention mostly because they exert some control over interest rates, and they use that control to make monetary policy, for better and for worse. It is less obvious, perhaps, that much of central banking is concerned with payments. Indeed, most central banks operate their currency area’s payment system, and that is what they are at the center of.

Payment systems rely on credit, so that debts not settled today can smoothly be rolled over into new debts due tomorrow. To reduce the amount of debt that has to get rolled over, most payment systems make use of netting, so that, whenever possible, debts are settled by offsetting them against other debts. Roughly, if I owe you and you owe me the same amount, we can write off both debts without further ado. To reduce flows through the center, most payment systems rely on hierarchy, encouraging debts to be resolved at lower levels.

This kind of system mostly works, and so whatever payments do flow through the center must be those that could not be netted, and could not be resolved lower in the hierarchy. These payments accumulate as credit instruments, promises to pay at various points in the future, owned or owed by the central bank. In other words, the assets and liabilities on central banks’ balance sheets are the trace, the net result of a history of payment imbalances. Reading the central bank balance sheet is therefore like reading a very concise summary of the entire economic system.

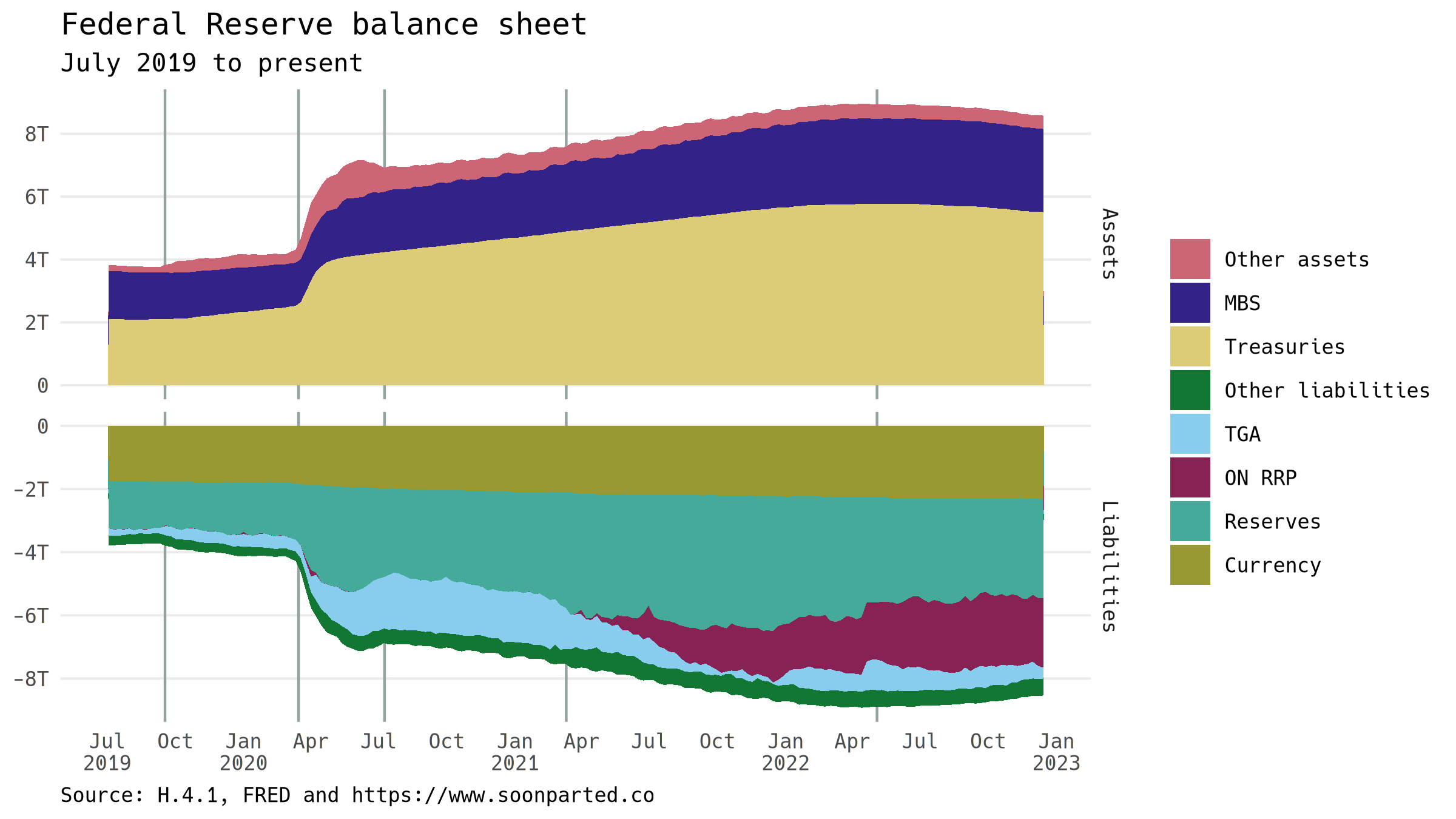

Two pictures of the Fed’s balance sheet

The last three years have been a time of pandemic and war, both of which have given rise to big payment flows, including attempts at both fiscal and monetary countercyclical policy. The effect on the Fed’s balance sheet has been substantial, as shown by the graph below. Assets are shown in the top panel, liabilities are shown below as negative numbers. This choice of presentation helps illustrate the fact that the balance sheet does in fact balance, which in visual terms means that the two panels are symmetrical:

Symmetrical in total, but not in structure: the Fed’s intermediation pushes and pulls on the financial relationships that cross through its balance sheet. The US central bank accepts funds from banks, money market funds, the US government and the general public, recorded on the liability side as reserves, repo (ON RRP) deposits, the Treasury General Account, and currency issuance respectively. The Fed places funds, purchasing mostly US Treasury debt and US mortgage-backed securities.

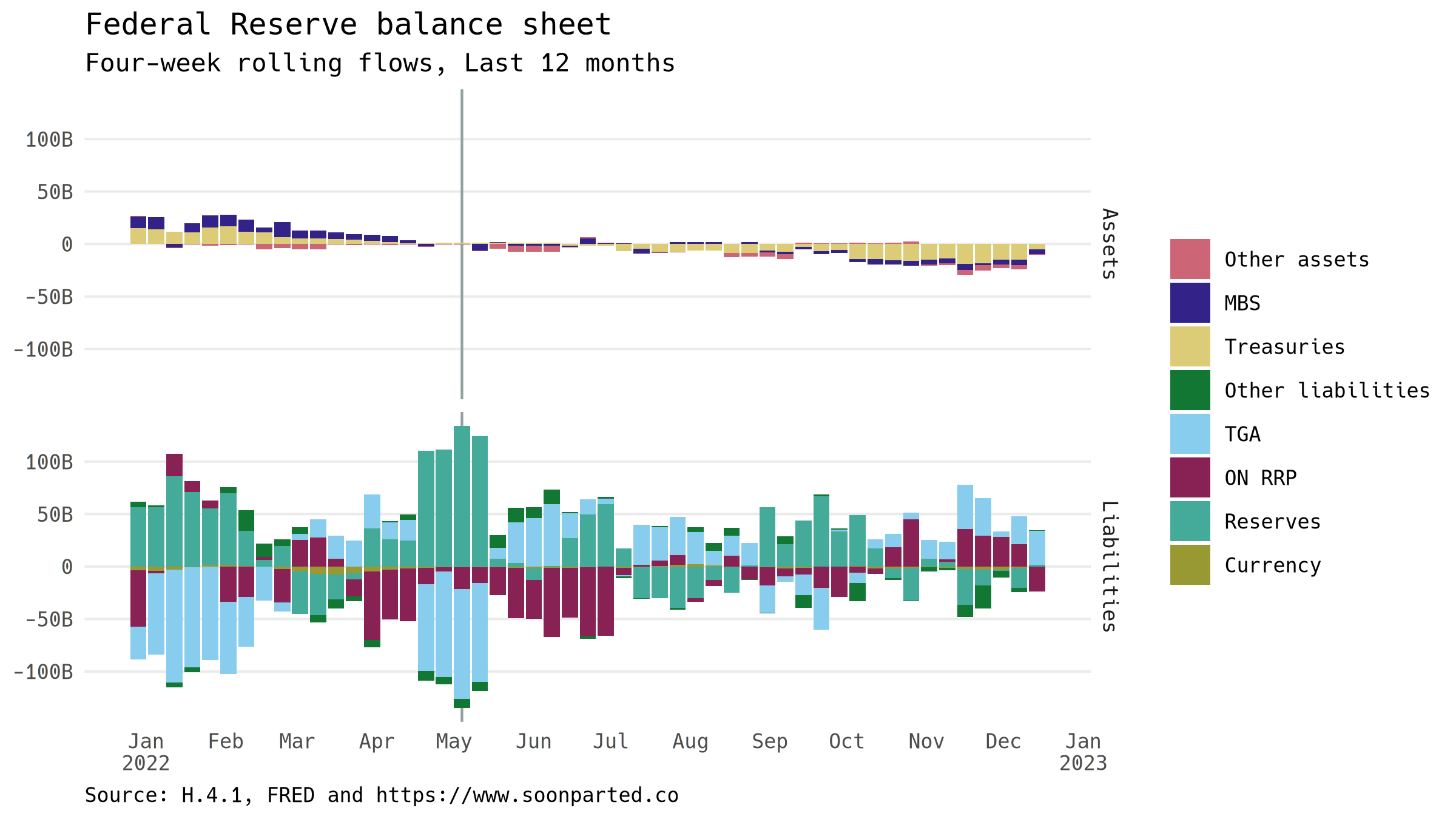

The Fed’s balance sheet has been contracting since the middle of the year, but that process has picked up speed in the last few weeks. This graph, based on the same balance-sheet data as above, illustrates not the levels but rather the changes in the various balance-sheet entries. Columns pointing outward indicate expansion, columns pointing inward indicate contraction. (Specifically, each week shows one-fourth of the four-week change in each entry, which smooths out week-to-week lumpiness and allows the month-to-month trends to come through clearly.)

At the end of 2021 and into the beginning of this year, at the left of the graph, the Fed was still buying securities, shown by positive flows on the asset side. In recent weeks, the balance sheet has swung decisively into contraction. Most of the reduction has come through runoff of Treasury securities; MBS holdings have dropped, but not much. This is despite the preference of some on the FOMC, who would like to get the Fed out of the mortgage market as soon as possible. Perhaps they don’t want to risk sparking a downturn in the housing market.

Conclusion

Changes on the liability side are more complex than those on the asset side, and the interpretation is not as clear. As the flow graph shows, funds have moved back and forth among ON RRP, reserves, and the TGA, during both expansion and contraction. In the last couple of weeks, however, the ON RRP facility has been contracting quickly, with reserves holding steady. Together with signs of normalization in short-term [money markets][leaks-to-flood], this suggests another turning point may be coming soon.