Along the curve

The New York Fed’s SOMA securities lending facility

I was inspired by an interesting chart in DC’s Chartbook #17 (about a third of the way down) to look into the New York Fed’s securities lending facility. This post is a quick dive into the data, which gives some insight into understanding conditions in the money markets.

The mechanics

The New York Fed allows primary dealers to borrow securities (mostly Treasury securities) from the System Open Market Account, the US central bank’s asset portfolio. The idea is that the Fed owns a huge—$8 trillion—inventory of securities. Because it intends to hold most of these to maturity, the Fed is usually not too concerned about which specific Treasury securities it holds. A billion dollars coming due in one month is about the same as a billion dollars maturing in the next month. But other market participants sometimes do, for example if they have taken a short position. So the Fed offers to lend specific issues for a fee (on which more below), almost always overnight, out of the SOMA.

One of the central bank’s jobs is to ensure that the market for US sovereign debt is working well, and making markets along the yield curve is a way to do that. The Fed’s New York branch receives a specific authorization to carry out these transactions from the Federal Open Market Committee, as it also does for open-market operations.

The sec lending facility sees consistent use—some 30 to 40 billion dollars a day in 2021 and 2022. The graph below shows the daily amount of securities lent out by FRBNY. I have taken a 14-day moving average to smooth out day-to-day variation. The vertical gray lines mark the passage of time by showing dates on which the FOMC changed interest rates (down in 2019 and 2020, up in 2022):

Pricing

The Fed normally charges a fee of 5 basis points for securities lending. This fee should be understood not as an interest rate but rather as a spread between interest rates. Specifically, it should correspond to the difference between the repo rate on the borrowed security and the repo rate on a typical (“general collateral”) security. Repo is thought of as a loan of money, but because it is collateralized, it can also be used to borrow securities.

When a specific issue of a security is expensive to borrow, because it is scarce or because the borrower is in a hurry, the cost of getting hold of it in the repo market becomes high (equivalently, the cost of borrowing cash against it becomes low). FRBNY will lend securities, evidently at terms sufficiently competitive that its offers are taken up. Presumably the Fed is not the only lender of such securities, so the quantities lent are a lower bound for what is happening in the wider market.

The fee paid and the quantities borrowed therefore give a measurement of dislocations in the Treasury yield curve. In the graph above, I have classified the borrowed securities by the fee charged. The standard fee, which is also the minimum fee, is 5 basis points. The fee rises to a few percentage points on rare occasions.

The source of the leak?

Rare occasions, but not as rare as they once were. Since mid-2021, in fact, the Fed has been lending consistently at higher spreads above GC repo rates, and for the last several months it has not infrequently has billions outstanding at spreads of 100 bp or more. This suggests the following graph, which just excludes all transactions priced at less than 7 bp. In other words, it shows when the Treasury yield curve was sufficiently lumpy that borrowers were willing to pay significant premiums to get the securities that they needed:

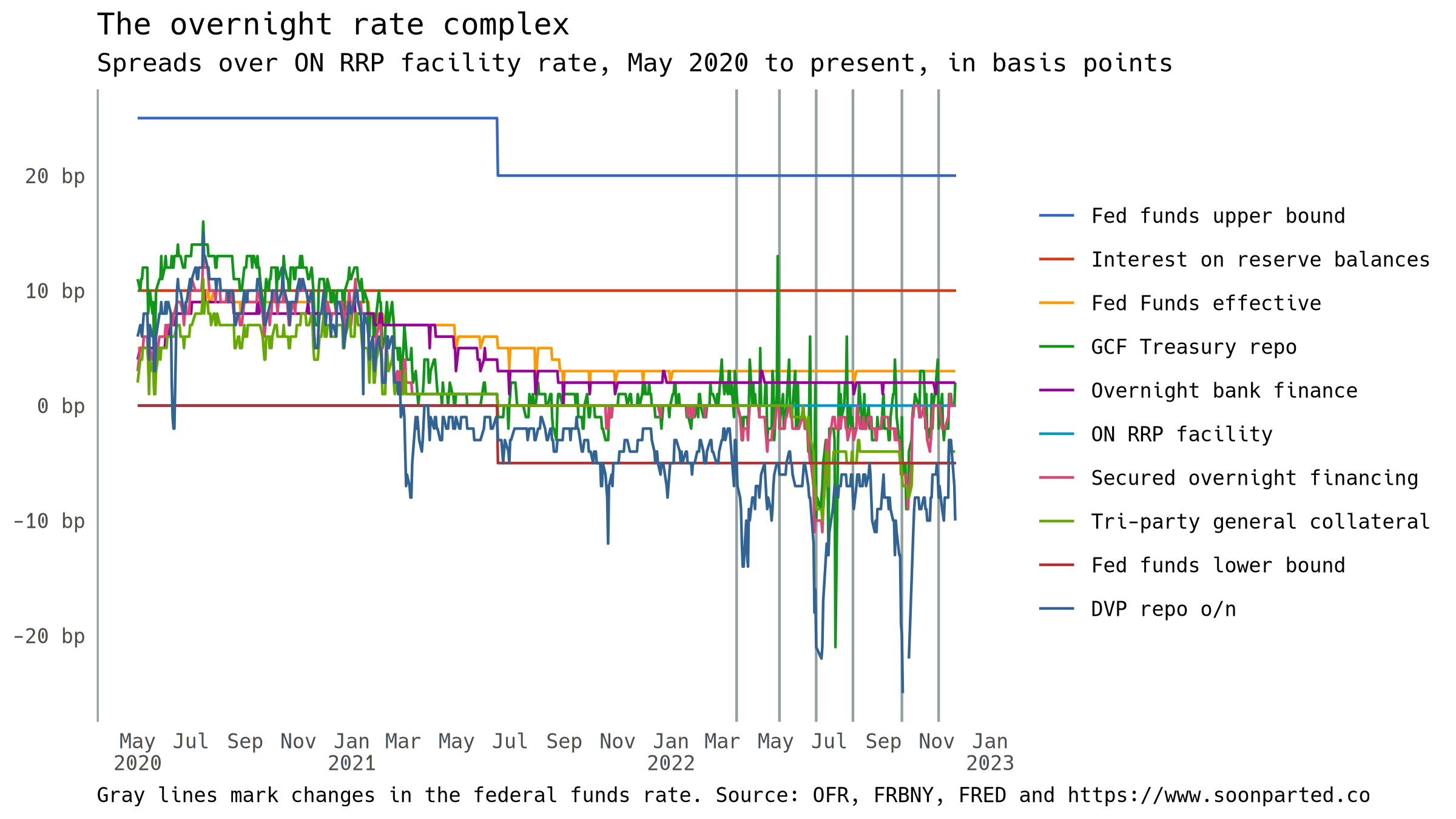

This period of disruption mirrors almost exactly the leaky floor in overnight interest rates:

If borrowers of collateral are accepting big spreads from the Fed, they are also probably accepting big spreads in the DvP repo market. So this fills in an important gap in understanding the Fed’s difficulties in getting traction on the entire overnight rate complex.