FTX

Mercifully quick

No one, I think, could spend a year of their life with Minsky and not develop a fondness for finance’s most dramatic trope—the liquidity event.

Liquidity is the ability to make payment, immediately and in size; providing liquidity is the business of financial intermediaries.

Though the idea of liquidity is everywhere in finance, and the word itself gets thrown around quite a lot, it is tricky to master. Like the white noise of a ventilation system, liquidity fades unnoticed into the background. When it is interrupted, the void it leaves behind stands out in comparison. Only after it is gone do we find out what liquidity was doing.

Not that there haven’t been plenty of examples. This week’s near-instantaneous evaporation of crypto exchange FTX joins a long list, including recently Terra/Luna, Evergrande, Archegos and Greensill. One could make a comparison to Lehman Brothers, though FTX is far from being a systemically important institution, outside of the cryptosphere that is. Liquidity events, each of them.

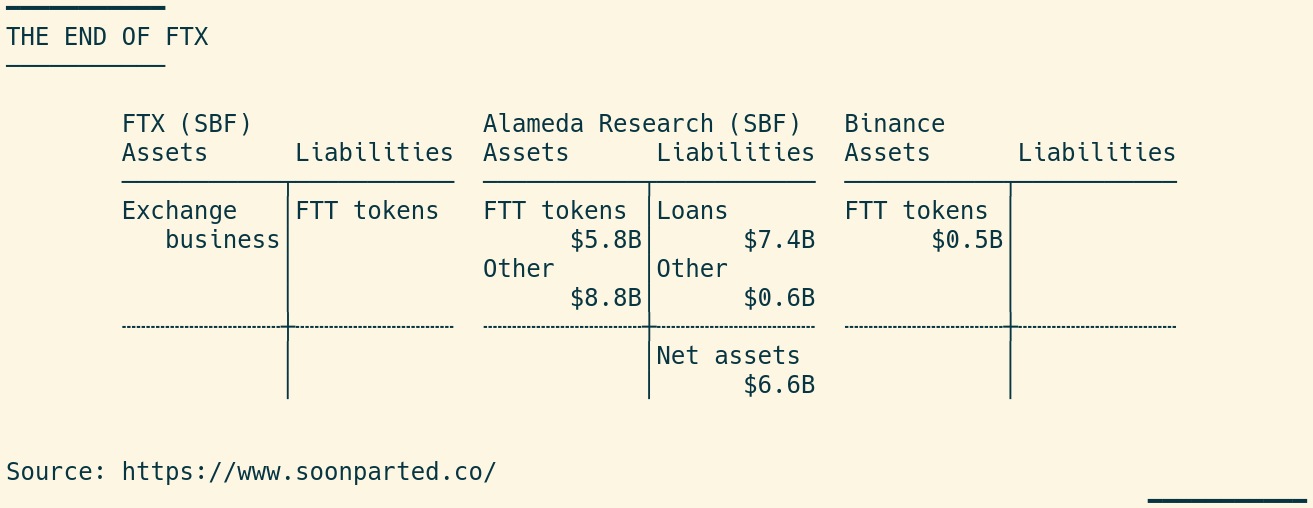

FTX’s collapse was precipitated by a leak of the balance sheet of crypto trading firm Alameda Research. Both FTX and Alameda are/were projects of Sam Bankman-Fried, styled until quite recently as a crypto-themed JP Morgan. SBF is, or rather was, the shaggy billionaire who swooped in to bail out his troubled rivals, so preserving the dream of decentralized finance—and making a fortune in the process.

CoinDesk’s Ian Allison reported on the leaked document, which revealed that Alameda was heavily invested in its sibling organization FTX. The information isn’t enough to write up a full balance sheet, but schematically it must be something like this:

What it says is this: FTX raised cash in part by issuing its own FTT crypto tokens. Alameda had bought a lot of those tokens using borrowed money. FTX’s rival Binance also held FTT tokens, about $500 million worth.

After CoinDesk’s story, Binance began very noisily selling; FTT tokens promptly shed 80% of their dollar price:

A graph with this general shape is obligatory in posts of this nature. The main lesson to draw from it is that “liquidity kills you quick”, or more precisely the sudden disappearance of liquidity does. The vertical part of the time series represents a not-insignificant destruction of paper wealth, especially of course for SBF.

Who’s next?

What’s more, for Alameda’s lenders, it was a destruction of collateral—their hope of getting repaid. Presumably they have been asking for their money back. Bankman-Fried, now unable to sell FTT tokens except at deep discount, would suddenly have found it much harder to pay them: liquidity event.

SBF tried to sell FTX to his archrival, Binance’s Changpeng Zhao (CZ), and for a few hours it seemed like that might work. But then, and after I had written the first draft of this post, that deal fell through. Evidently US regulators’ interest in FTX is sufficiently fervent that even a fire-sale price is too high. “We do not want to face FTX,” as Faina Epshteyn might have said.

Seems like a domino in the lead-up to SVB's collapse.

Thanks for writing a timely piece.

I think FTT should be included in the Asset side.

Although FTT is issued by FTX, it is not a financial asset which is also a debt of the issuer.

Gold is to nobody's liability what FTT is to FTX's asset(not liability)

As you can see B/S in https://www.ft.com/content/0c2a55b6-d34c-4685-8a8d-3c9628f1f185,

FTT is in asset side not in liability side.

Correct me if I'm wrong.

Thanks.