Day by day

The Fed in the Long Pandemic

Writing in the Financial Times about March’s bank failures, Adam Tooze surprised me with this observation: “We would not be here but for the pandemic.” Obviously true, but I was surprised to realize, thanks to Tooze, that it now needs to be stated explicitly. I had taken the COVID-19 pandemic to be part of the unstated context.

So, in what follows, I walk the path between the SVB Panic (“March Madness”) and the pandemic, using the Fed’s balance sheet as the map.

A map, or maybe a seismogram

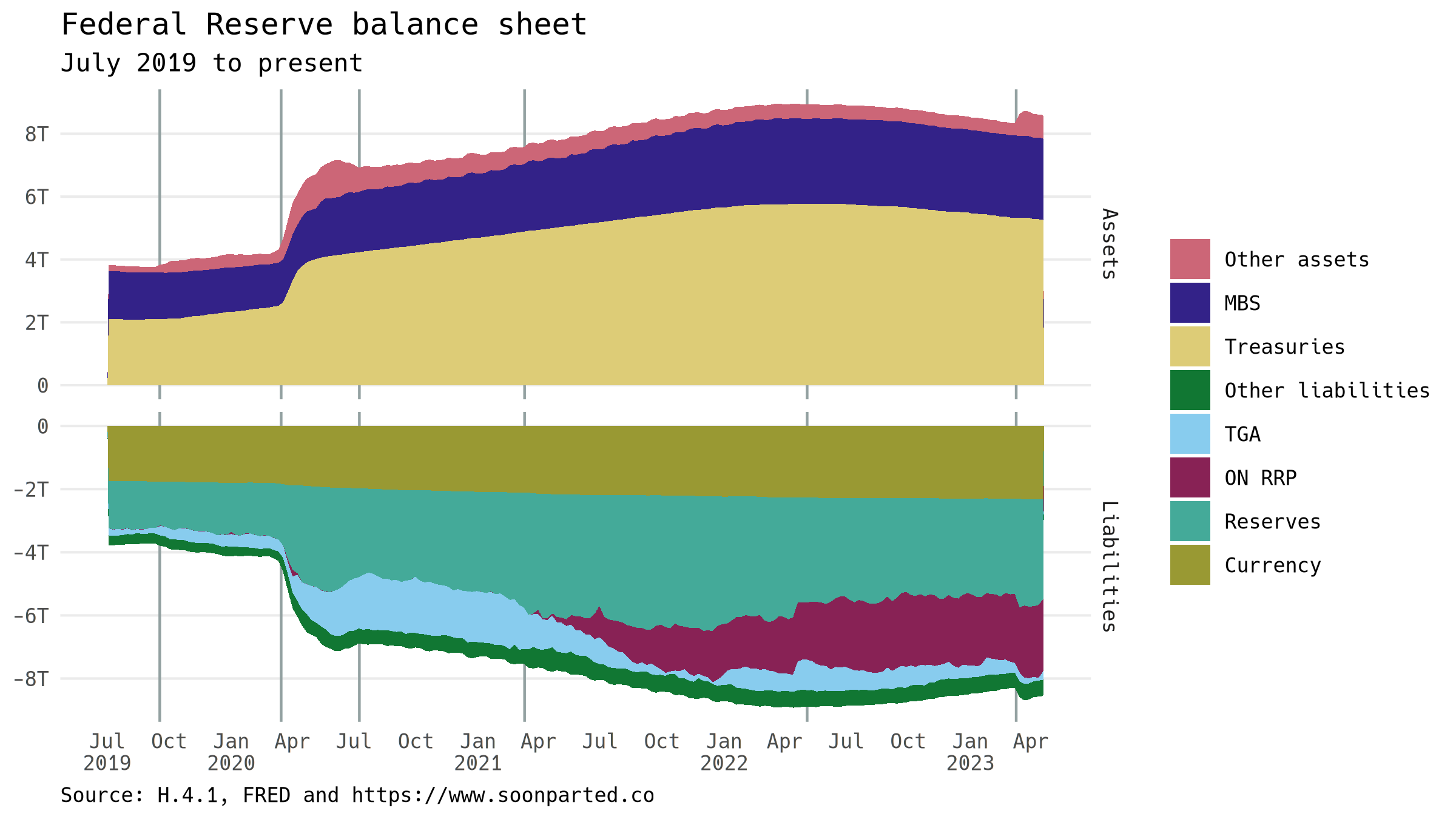

This is visualization of the balance sheet of the core institution of the entire global monetary system, the US Federal Reserve. Assets are shown in the top panel; liabilities below. The image is symmetrical, which is a visual expression of an accounting fact, the balance sheet identity “assets equal liabilities.” Time is represented on the horizontal axis, dollar amounts on the vertical axis:

For Fed-watchers, the Long Pandemic is the right scope: quantitative easing had begun after the repo crisis of September 2019, brought on by the balance-sheet contraction policy that had preceded it. As a result, the Fed’s balance sheet was already expanding when the COVID-19 pandemic went global in March of 2020. The accelerated QE took the form of purchases by the central bank of Treasury and mortgage-backed securities (MBS), ending in May 2022 after a total expansion of more than four trillion dollars. In the balance-sheet graph, colors1 represent balance sheet entries; QE is thus easy to spot in the upper panel.

The inflation of 2021 and 2022 can be seen as having three short-term causes. First, production systems everywhere were suddenly stopped and then re-started in the early weeks of the pandemic. With minimal buffer stocks to absorb the disruption of supply chains, shortages meant that sellers everywhere had the upper hand, and so prices rose. Second, with social spaces closed, consumption substituted from services to goods. Sellers of goods thus had the upper hand, and prices rose. Third, Russia invaded Ukraine, disrupting commodity flows in various ways. Sellers of commodities had the upper hand, and so prices rose.

The Fed’s mandate requires that it respond to high inflation, so despite its early insistence that price rises would be “transitory,” the central bank was nonetheless eventually compelled to tighten monetary policy. This began in earnest after May 2022: balance sheet contraction through securities sales, and increases in overnight interest rates.

Bond prices have been driven down, and rates have been driven up, to the point where commercial banks’ securities are worth less than face value. I have not yet seen a report on exactly what set off the run on SVB, but in one way or another, its creditors were worried that if the bank would not be able to generate enough cash by selling securities. The Fed used its balance sheet to stave off the panic, visible in the graph as a recent blip of expansion, after a year of contraction.

In one long sentence

The SVB Panic is a symptom of stress on bank balance sheets;

bank balance sheets are stressed by unrealized losses on security holdings;

security prices are down because the Fed has been selling assets and because short rates have been raised;

these tightening policies are the central bank’s response to inflation;

inflation is high because of the pandemic and because of Russia’s invasion of Ukraine; and crucially

both of these factors represented a sudden shift in macroeconomic conditions, in favor of sellers.

Each of these statements would, I think, be widely accepted, but it is getting harder to hold them all in mind at once.

Previously on Soon Parted

Using a colorblind-safe scheme, see the work of Paul Tol. Interestingly to me, these schemes are designed to hold up pretty well even in grayscale, so you can print in black-and-white and still read the charts.↩︎