Money is valuable again

Financial conditions beyond the fed funds rate

The FOMC is meeting this week, and unless something big changes on Wednesday, all attention will be on its decision to raise or not to raise rates. All well and good, but the level of the fed funds rate is only one aspect of financial conditions, and not even the most important aspect. Today: a more complete picture.

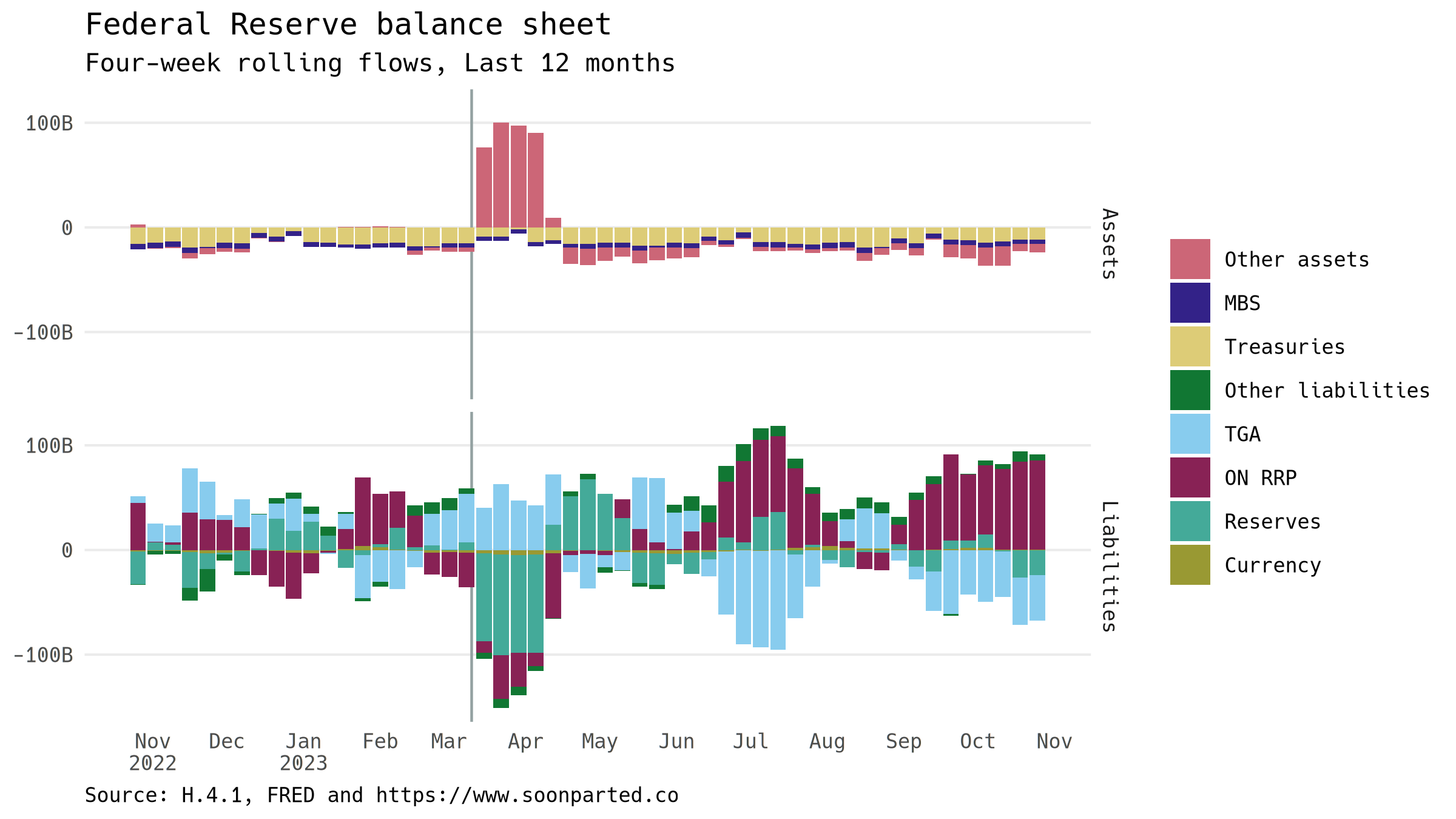

This graph shows four-week rolling changes in the Fed’s balance sheet entries. Assets are above, liabilities below. Bars pointing toward the outside of the graph indicate expansion; bars pointing toward the center indicate contraction. The asset side is mostly set by policy, which for a year and a half has been a policy of contraction (so-called quantitative tightening). A portion of maturing Treasury and agency securities are not being rolled over. The exception to this policy of expansion was the March’s SVB Panic. (Note SVB, which happened all at once, gets smudged into a four-week episode in this graph, a fair price I think for being able to see other trends more clearly.)

The liability side is also affected by the Fed’s policy stance, though the effect is more indirect. Since July, the overwhelming feature of the liability side has been the contraction of the overnight reverse repo (ON RRP) facility. As the graph shows, usage of the ON RRP facility has fallen steadily, largely in favor of Treasury deposits in the Treasury General Account (TGA).

What is ON RRP anyway? This repo deposit facility allows a set of financial institutions, mostly money market funds, to deposit funds at the Fed and receive interest at the ON RRP rate, which is typically 3bp below the fed funds effective rate, and exactly 5bp above the fed funds lower bound. ON RRP deposits are made using the tri-party repo system, so that depositors receive Treasury securities as collateral for their cash. The ON RRP facility predated the pandemic, having seen some experimental usage over the last decade, but its usage was dramatically expanded in 2021 and 2022. The Fed created trillions of dollars of funds through asset purchases, and ON RRP was the liability entry that was chosen to match the expansion:

The vertical lines in this graph mark the key turning points in the Fed’s balance sheet. Post-SVB, i.e. to the right of the last vertical line, the tide has turned for the ON RRP facility, with usage on track to fall below $1 trillion in the next couple of weeks. ON RRP usage is falling much faster than the Fed’s balance sheet is shrinking, which means the funds are moving, not being destroyed. By looking at money market funds’ assets, we can see what is happening. Money funds have been buying Treasury debt, $750 billion from July through September. At least half of the funds has come from the contraction in RRP, and the October data is likely to show more of the same:

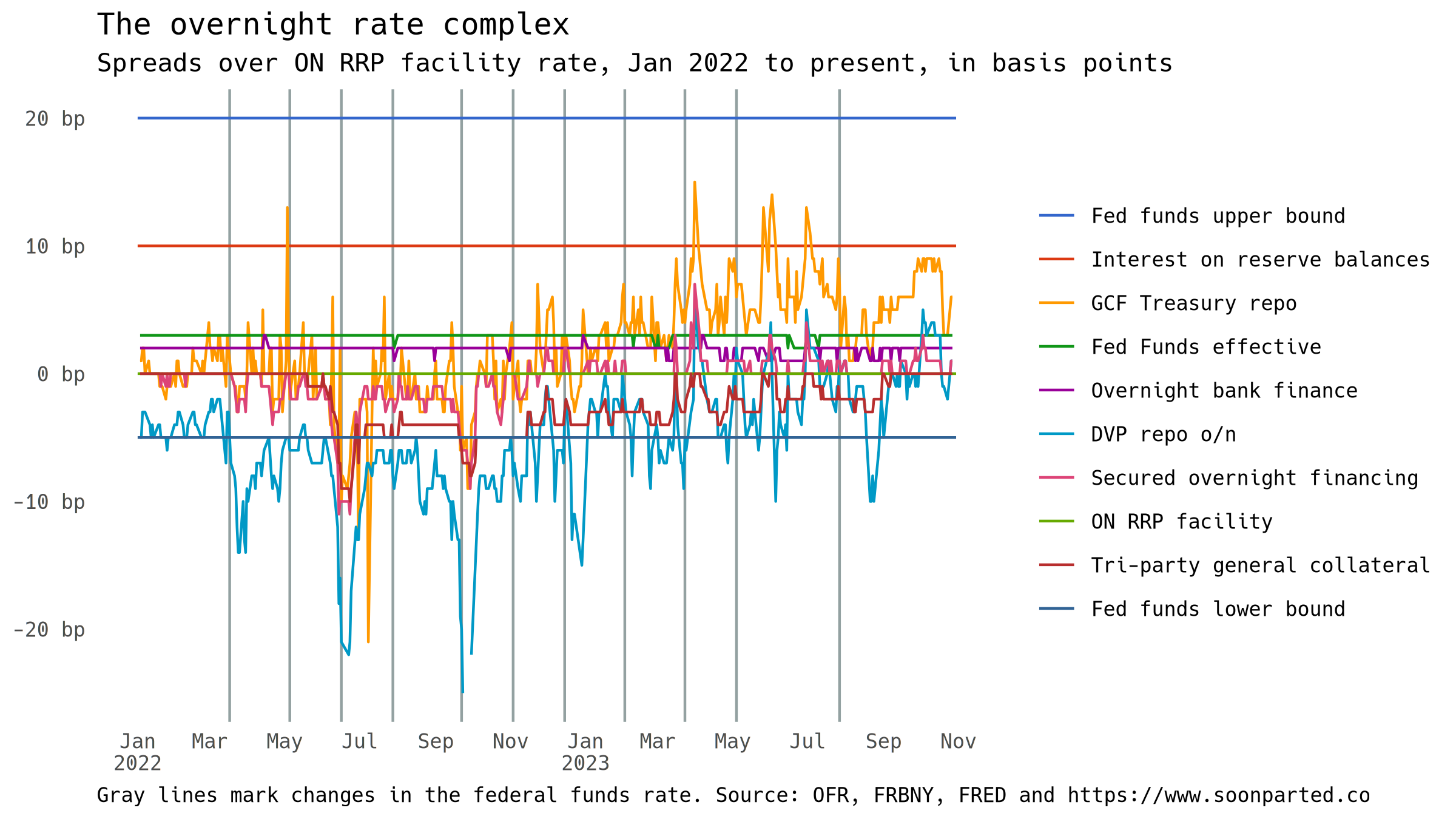

Everything above is in terms of balance sheet quantities, but the story is there in the prices, too. Let me end with one of my favorite graphs, the overnight rate complex. This graph shows the key US dollar overnight interest rates. Since financial institutions are both borrowers and lenders of money, it makes sense to think not about the levels of interest rates, but about the spreads between interest rates. The graph shows the spreads of overnight rates above the ON RRP facility rate.

For all of 2022, there was so much money washing around in the financial system that a significant fraction of repo lenders would accept rates below the Fed’s ON RRP rate. There are specific reasons for this, for example the DVP repo market is one place where bond shorts can obtain securities, accepting low rates on their cash as part of the carry for holding their securities. Still, for most of 2022 the entire overnight complex was below the fed funds rate: lots of lenders were accepting very low compensation for their cash.

That has changed, especially since September. No rates have printed below the fed funds lower bound since then, and the ON RRP rate, 5bp higher, is increasingly effective as a floor. That means that those who have cash are increasingly finding that they can get better compensation by doing something other than depositing at the Fed—hence the decline in ON RRP. In other words, money is valuable again.

What’s next? Now that money is valuable again, those who have it will hold on to it more tightly. It will almost certainly end in a scramble for cash. I won’t try to predict whether that scramble will come sooner or later, but when it comes, it will, nearly by definition, come suddenly and from an unexpected direction.